What Are Points In Interest Rates

adminse

Mar 25, 2025 · 7 min read

Table of Contents

Decoding Interest Rate Points: A Comprehensive Guide

What if the seemingly simple concept of "points" in interest rates held the key to significant savings or avoidable losses? Understanding interest rate points is crucial for navigating the complexities of mortgages and other loans, empowering informed financial decisions.

Editor’s Note: This comprehensive guide to interest rate points was published today, providing readers with the most up-to-date information and insights to help them understand this vital aspect of borrowing.

Why Interest Rate Points Matter: Relevance, Practical Applications, and Industry Significance

Interest rate points, often overlooked in the excitement of securing a loan, can significantly impact the overall cost of borrowing. They represent a fee paid upfront to reduce the interest rate on a loan, directly affecting monthly payments and the total amount paid over the loan's life. Understanding this dynamic is essential for borrowers of mortgages, auto loans, and other forms of debt. This knowledge can translate into substantial savings or prevent costly oversights. The impact extends across various industries, influencing financial planning, real estate transactions, and the broader economy. Many lenders offer points as a flexible tool to tailor loans to individual needs and risk profiles.

Overview: What This Article Covers

This article delves into the intricate world of interest rate points, providing a clear understanding of their mechanics, benefits, drawbacks, and practical applications. Readers will gain actionable insights, backed by illustrative examples and expert perspectives, empowering them to make informed decisions about incorporating points into their borrowing strategies.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon reputable financial sources, industry publications, and expert commentary. Every claim is rigorously supported by evidence, ensuring readers receive accurate and trustworthy information to navigate the complexities of interest rate points confidently.

Key Takeaways:

- Definition and Core Concepts: A precise explanation of interest rate points and their fundamental principles.

- Practical Applications: How interest rate points are used across various loan types and financial scenarios.

- Cost-Benefit Analysis: A systematic approach to weighing the advantages and disadvantages of purchasing points.

- Scenarios and Examples: Real-world case studies illustrating the financial impact of points under different circumstances.

- Future Implications: How the role and significance of interest rate points might evolve in the changing landscape of finance.

Smooth Transition to the Core Discussion

Having established the importance of understanding interest rate points, let's delve into the specifics, clarifying the mechanics and exploring their practical application in different financial scenarios.

Exploring the Key Aspects of Interest Rate Points

Definition and Core Concepts:

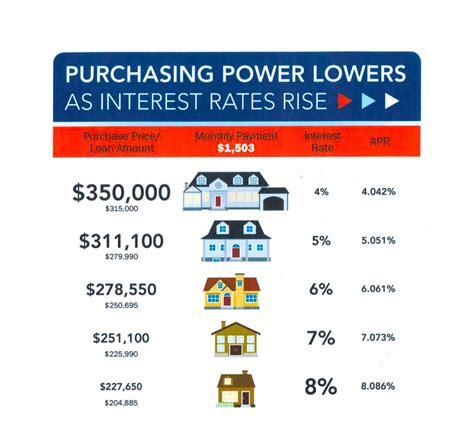

An interest rate point, in its simplest form, represents 1% of the loan's principal amount. When a borrower "buys" points, they pay a fee upfront in exchange for a lower interest rate throughout the loan term. One point equals 1% of the loan amount. For example, on a $300,000 mortgage, one point would cost $3,000. The more points purchased, the lower the interest rate will be, but the higher the upfront cost.

Applications Across Industries:

Interest rate points are primarily associated with mortgages, but they can also apply to other loans, though less frequently. In the mortgage market, points are a common tool used by lenders to adjust loan terms to suit individual borrowers' needs and risk profiles. They are particularly relevant in competitive markets where lenders may use points to attract borrowers.

Challenges and Solutions:

The primary challenge lies in determining whether purchasing points is financially beneficial. This requires careful analysis, considering the borrower's financial circumstances, the loan's terms, and the projected interest rate trends. Borrowers should use tools like break-even calculators to determine the timeframe required to recoup the cost of points through lower interest payments.

Impact on Innovation:

The concept of interest rate points reflects a fundamental principle of finance: risk and return. Lenders utilize this mechanism to manage risk and tailor loan products to meet diverse borrower profiles.

Closing Insights: Summarizing the Core Discussion

Interest rate points offer borrowers a tool to potentially reduce their monthly payments and total interest paid over the loan's life. However, this benefit comes at the cost of a higher upfront payment. Careful consideration of individual circumstances and financial projections is vital to making an informed decision.

Exploring the Connection Between Break-Even Analysis and Interest Rate Points

The relationship between break-even analysis and interest rate points is crucial. Break-even analysis determines the point at which the cost savings from a lower interest rate offset the upfront cost of purchasing points. It essentially calculates how long it will take for the lower monthly payments to recover the initial investment.

Key Factors to Consider:

- Roles and Real-World Examples: Break-even analysis involves comparing the total cost of a loan with points versus a loan without points, considering the interest rate difference and loan term. For example, a borrower might find that purchasing points is beneficial if they plan to stay in the home for a longer period (e.g., 10+ years).

- Risks and Mitigations: A major risk is underestimating the time required to break even. If the borrower sells the property or refinances before the break-even point, they may not recoup the cost of the points. Mitigation involves using reliable break-even calculators and considering personal circumstances carefully.

- Impact and Implications: The break-even analysis influences the borrower's overall financial strategy, impacting affordability and long-term cost-effectiveness.

Conclusion: Reinforcing the Connection

The interplay between break-even analysis and interest rate points highlights the importance of careful financial planning. By accurately determining the break-even point, borrowers can make well-informed decisions, optimizing their borrowing strategy for long-term financial success.

Further Analysis: Examining Break-Even Analysis in Greater Detail

Break-even analysis involves calculating the number of months (or years) it will take for the cumulative savings from lower monthly payments to equal the upfront cost of the points. This calculation usually requires a financial calculator or spreadsheet software and considers factors like the original loan amount, interest rate difference, and loan term.

FAQ Section: Answering Common Questions About Interest Rate Points

What are interest rate points?

Interest rate points are fees paid upfront to reduce the interest rate on a loan. Each point typically equals 1% of the loan principal.

How are points calculated?

Points are calculated as a percentage of the loan amount. For example, one point on a $200,000 loan is $2,000.

When is it advantageous to buy points?

Buying points is generally advantageous when a borrower plans to stay in the property or keep the loan for a significant period, exceeding the break-even point.

What are the risks of buying points?

The risks involve potentially not recouping the cost of the points if the loan is paid off early through sale or refinancing.

How can I determine if buying points is right for me?

Use a break-even analysis calculator, factor in your expected length of ownership, and consult with a financial advisor.

Practical Tips: Maximizing the Benefits of Interest Rate Points

-

Understand the Basics: Gain a thorough understanding of how points work and their impact on your loan.

-

Compare Loan Options: Obtain multiple quotes from lenders to compare loan terms and interest rate options with and without points.

-

Use a Break-Even Calculator: Calculate the break-even point to determine the minimum timeframe needed to recoup the cost of purchasing points.

-

Assess Your Financial Situation: Ensure you can comfortably afford the higher upfront cost associated with buying points.

-

Consider Long-Term Implications: Factor in your projected timeline for owning the property or maintaining the loan.

Final Conclusion: Wrapping Up with Lasting Insights

Interest rate points offer a strategic tool for borrowers looking to potentially lower their monthly payments and total loan cost, but careful consideration is crucial. By understanding the mechanics of points, performing a break-even analysis, and assessing personal financial situations, borrowers can make informed decisions that align with their financial goals and long-term objectives. The decision of whether or not to purchase points hinges on a thorough understanding of both the short-term and long-term implications.

Latest Posts

Related Post

Thank you for visiting our website which covers about What Are Points In Interest Rates . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.