Limited Pay Life Insurance Meaning

adminse

Mar 28, 2025 · 9 min read

Table of Contents

Decoding Limited-Pay Life Insurance: A Comprehensive Guide

What if securing your family's financial future didn't require lifelong premium payments? Limited-pay life insurance offers a strategic approach to permanent life insurance coverage, providing lifelong protection with a finite payment schedule.

Editor’s Note: This article on limited-pay life insurance was published today, providing readers with the most up-to-date information and insights into this crucial financial planning tool.

Why Limited-Pay Life Insurance Matters:

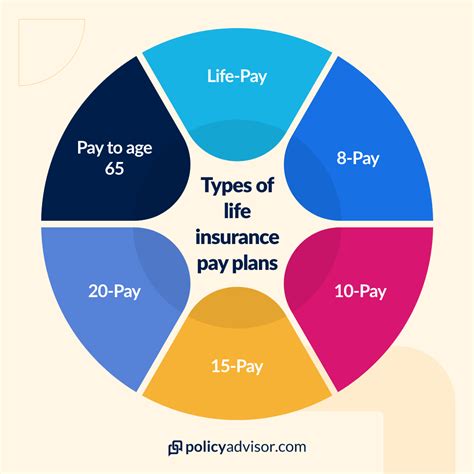

Limited-pay life insurance, a type of permanent life insurance, stands out for its unique structure. Unlike whole life insurance, which requires premium payments throughout the insured's life, limited-pay policies require payments for a specified period – typically 10, 20, or 30 years, or until a certain age, such as 65. Once this payment period concludes, coverage continues for the insured's entire life, even without further premium contributions. This feature makes it an attractive option for those seeking long-term financial security while managing their budgetary constraints. Its significance lies in its flexibility, offering a balance between lifelong protection and manageable premium schedules. This type of policy can be especially appealing to high-income earners who expect their income to decrease in retirement, or those seeking to leave a substantial legacy for their heirs.

Overview: What This Article Covers:

This article dives deep into the intricacies of limited-pay life insurance. We will explore its definition, key features, advantages and disadvantages, explore its variations, compare it to other life insurance options, and provide practical advice for determining if it's the right choice for your individual circumstances. Readers will gain a comprehensive understanding of this complex financial product, enabling informed decision-making.

The Research and Effort Behind the Insights:

This in-depth analysis draws from extensive research, including examination of industry reports, financial planning literature, and analysis of policy documents from leading insurance providers. The information presented is designed to be accurate, unbiased, and helpful to readers seeking to make sound financial choices.

Key Takeaways:

- Definition and Core Concepts: A clear understanding of what constitutes limited-pay life insurance and its fundamental principles.

- Variations and Types: Exploration of different types of limited-pay policies and their specific characteristics.

- Advantages and Disadvantages: A balanced assessment of the benefits and drawbacks to help readers weigh the pros and cons.

- Comparison with Other Policies: A comparative analysis against other life insurance options, highlighting their key differences.

- Practical Applications: Real-world scenarios illustrating the use of limited-pay life insurance in financial planning.

- Selection Criteria: Factors to consider when choosing a limited-pay life insurance policy.

Smooth Transition to the Core Discussion:

Having established the relevance and importance of understanding limited-pay life insurance, let's delve into the specifics, examining its core features and nuances.

Exploring the Key Aspects of Limited-Pay Life Insurance:

1. Definition and Core Concepts:

Limited-pay life insurance is a type of permanent life insurance offering lifelong coverage, but with premiums paid only for a predetermined period. This period can range from 10 to 30 years, or until the insured reaches a specific age. The key feature differentiating it from whole life insurance is the finite payment schedule. After the limited payment period, the policy remains in force, offering continued death benefit protection without further premiums. This is achieved through the accumulation of cash value within the policy, which is invested and grows over time to help fund future death benefits.

2. Variations and Types:

While the core principle remains consistent, limited-pay life insurance can manifest in various forms. Some common variations include:

- Limited-Pay Whole Life: This is the most common type, offering lifelong coverage with a fixed premium payment period.

- Limited-Pay Universal Life: This offers flexibility in premium payments within the limited-pay period, although the total premiums paid remain within the defined timeframe. Cash value growth can vary depending on the underlying investment options.

- Modified Limited-Pay: This starts with lower premiums for an initial period, which then increase to a higher, fixed level for the remaining payment term.

3. Advantages of Limited-Pay Life Insurance:

- Predictable Premiums: Payments are fixed and known in advance, making budgeting easier.

- Lifelong Coverage: Provides peace of mind knowing that death benefit protection lasts a lifetime.

- Cash Value Accumulation: Builds cash value that grows tax-deferred and can be accessed through loans or withdrawals (though this impacts the death benefit).

- Financial Planning: Can serve as an estate planning tool, providing a death benefit to heirs.

- Potential for Higher Death Benefit: Compared to term life insurance with the same premium outlay over a limited period, the limited-pay policy can result in a larger death benefit.

4. Disadvantages of Limited-Pay Life Insurance:

- Higher Initial Premiums: Premiums are generally higher than term life insurance because of the lifelong coverage and cash value accumulation.

- Less Flexibility: Once the payment period is over, it’s harder to adjust the coverage amount.

- Cash Value Fluctuations (for some types): The cash value growth in universal life variations can be affected by market conditions.

- Complexity: The policies can be more complex than term life insurance, requiring a thorough understanding before purchasing.

- Potential for Loan Usage Impacts: Using cash value for loans can reduce the death benefit.

5. Comparison with Other Policies:

Limited-pay life insurance stands in contrast to other types of life insurance:

- Term Life Insurance: Offers coverage for a specific period, typically 10, 20, or 30 years, at a lower premium. It does not build cash value.

- Whole Life Insurance: Offers lifelong coverage with premiums paid throughout life, also building cash value.

- Universal Life Insurance: Provides lifelong coverage with flexible premium payments and adjustable death benefit. Cash value can vary with market fluctuations.

6. Practical Applications of Limited-Pay Life Insurance:

Limited-pay life insurance is suitable for individuals with:

- Specific Financial Goals: Planning for estate taxes, providing for heirs, or creating a legacy.

- Desire for Lifelong Coverage: Seeking guaranteed coverage throughout their life.

- Capacity for Higher Premiums: Able to afford the initially higher premium cost.

- Long-Term Financial Planning: Looking for a long-term financial security solution.

7. Selection Criteria for Choosing a Policy:

When selecting a limited-pay life insurance policy, consider the following:

- Length of the Payment Period: Choose a duration aligned with your financial capabilities and goals.

- Death Benefit Amount: Select an amount sufficient to meet your family's needs.

- Insurance Provider Reputation: Research the financial stability and reputation of the insurance company.

- Policy Features and Riders: Understand the specific features, riders, and potential benefits.

- Cost Comparison: Compare quotes from multiple insurers to find the best value.

Exploring the Connection Between Cash Value Growth and Limited-Pay Life Insurance:

Cash value growth is intrinsically linked to limited-pay life insurance. The higher premiums paid over a shorter period allow for significant cash value accumulation. This cash value grows tax-deferred, meaning you won’t pay taxes on the gains until you withdraw them. However, the cash value growth rate varies depending on the policy type (whole life generally has a more predictable growth rate than universal life) and the insurer's investment performance (for universal life policies).

Key Factors to Consider:

- Roles and Real-World Examples: Cash value can be used for supplementary retirement income, college funding, or other financial needs. Imagine a business owner using the cash value as collateral for a loan to expand their operations.

- Risks and Mitigations: The cash value’s growth is not guaranteed, especially in variable universal life policies. Proper understanding of the policy’s terms and potential investment risk is crucial.

- Impact and Implications: Proper cash value management can significantly enhance the overall value of the policy. However, withdrawing or borrowing against cash value will reduce the death benefit.

Conclusion: Reinforcing the Connection:

The relationship between cash value and limited-pay life insurance is symbiotic. The limited payment structure facilitates cash value growth, enhancing the policy's overall value and offering financial flexibility. Understanding this connection enables informed decisions regarding policy selection and cash value management.

Further Analysis: Examining Cash Value Accumulation in Greater Detail:

Cash value accumulation is not just a passive feature; it’s a dynamic component of limited-pay life insurance. The rate of cash value growth is influenced by several factors, including the policy's type, the insurer’s investment strategy, and the policy’s fees. Understanding these nuances is vital for maximizing the benefits of cash value growth.

FAQ Section: Answering Common Questions About Limited-Pay Life Insurance:

-

What is limited-pay life insurance? Limited-pay life insurance is a type of permanent life insurance that provides lifelong coverage but with premiums paid for a limited period only.

-

How does limited-pay life insurance differ from whole life insurance? Limited-pay life insurance has a defined premium payment period, while whole life requires premiums for the entire life of the insured.

-

What are the benefits of choosing a limited-pay policy? Benefits include predictable premiums, lifelong coverage, cash value accumulation, and estate planning potential.

-

What are the drawbacks of limited-pay life insurance? Drawbacks include higher initial premiums compared to term life, less flexibility, and potential complexity.

-

How is the cash value calculated? Cash value growth is influenced by factors like the type of policy, interest rates, and fees. It is generally a complex calculation detailed in the policy document.

-

Can I borrow against my cash value? Yes, many limited-pay policies allow borrowing against the accumulated cash value, but this will impact the death benefit.

Practical Tips: Maximizing the Benefits of Limited-Pay Life Insurance:

- Compare policies: Obtain quotes from multiple insurance providers before making a decision.

- Understand policy features: Carefully review the policy document to understand all terms, fees, and benefits.

- Consult a financial advisor: Seek professional advice to determine if a limited-pay policy is appropriate for your needs.

- Plan for premium payments: Ensure you can comfortably afford the premiums during the payment period.

- Monitor cash value growth: Track your policy's cash value growth to ensure it aligns with your expectations.

Final Conclusion: Wrapping Up with Lasting Insights:

Limited-pay life insurance offers a compelling solution for individuals seeking lifelong coverage with a manageable premium payment schedule. By understanding its intricacies, benefits, and potential drawbacks, individuals can make informed decisions about this valuable financial tool. Careful planning and consideration of personal financial circumstances are key to harnessing the advantages of this type of insurance. It’s a powerful tool for financial security and legacy planning, but should be chosen strategically based on one's specific needs and risk tolerance.

Latest Posts

Latest Posts

-

Inside Days Definition Trading Strategy Examples Vs Outside

Apr 24, 2025

-

Input Output Analysis Definition Main Features And Types

Apr 24, 2025

-

Inorganic Growth Definition How It Arises Methods And Example

Apr 24, 2025

-

Inland Revenue Definition

Apr 24, 2025

-

Inland Bill Of Lading Definition

Apr 24, 2025

Related Post

Thank you for visiting our website which covers about Limited Pay Life Insurance Meaning . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.