How To Get Private Student Loans Out Of Default

adminse

Mar 28, 2025 · 8 min read

Table of Contents

Escaping the Grip: A Comprehensive Guide to Getting Private Student Loans Out of Default

What if the weight of defaulted student loans could be lifted, paving the way for financial stability? Rehabilitating private student loans is a challenging but achievable process, requiring strategic planning and a firm understanding of the available options.

Editor's Note: This article provides up-to-date information on navigating the complex process of rehabilitating defaulted private student loans. The information presented is for guidance only and should not be considered legal or financial advice. Readers are encouraged to seek professional counsel for their specific circumstances.

Why Getting Private Student Loans Out of Default Matters:

Defaulting on a private student loan has severe consequences, impacting credit scores, hindering future borrowing opportunities, and potentially leading to wage garnishment or legal action. Rehabilitation is crucial for restoring financial health and securing a brighter future. Understanding the process and available options empowers individuals to regain control of their finances and build a more stable financial life. This includes regaining access to credit and avoiding further financial damage.

Overview: What This Article Covers:

This article delves into the intricacies of private student loan default, offering a step-by-step guide to rehabilitation. It explores the various rehabilitation options, including loan consolidation, repayment plans, and settlement options. Readers will gain actionable insights into negotiating with lenders, understanding their rights, and building a sustainable repayment plan.

The Research and Effort Behind the Insights:

This comprehensive guide is the result of extensive research, drawing upon information from reputable sources like the Consumer Financial Protection Bureau (CFPB), the National Foundation for Credit Counseling (NFCC), and numerous legal and financial publications. The information presented aims to provide readers with accurate and reliable information to help them navigate this challenging process.

Key Takeaways:

- Understanding the Default Process: Knowing the stages of default and the legal implications.

- Contacting Lenders: The importance of proactive communication with loan servicers.

- Exploring Rehabilitation Options: Examining various repayment plans and settlement possibilities.

- Negotiating with Lenders: Strategies for achieving favorable repayment terms.

- Protecting Your Rights: Understanding consumer protection laws and avoiding predatory practices.

- Building a Budget and Repayment Plan: Developing a sustainable strategy for managing debt.

- Credit Repair Strategies: Steps to rebuild credit after default.

Smooth Transition to the Core Discussion:

Having established the significance of rehabilitating defaulted private student loans, let's explore the practical steps involved in this process.

Exploring the Key Aspects of Getting Private Student Loans Out of Default:

1. Understanding the Default Process:

Before embarking on the rehabilitation journey, it's vital to understand how a private student loan reaches default status. Typically, this occurs after a prolonged period of non-payment, usually 90 days or more. The specific timeframe can vary based on the lender's policies and the loan agreement. Once in default, lenders may initiate collection activities, including reporting the default to credit bureaus, potentially leading to a significant drop in credit scores. They may also pursue legal action, such as wage garnishment or pursuing legal judgments.

2. Contacting Your Lenders Immediately:

Proactive communication with your lender is paramount. Even if you're currently unable to make full payments, reaching out to explain your situation and explore potential solutions can prevent further damage. Many lenders are willing to work with borrowers who demonstrate a genuine desire to resolve their debt. This initial contact can open the door to potential repayment options or other solutions.

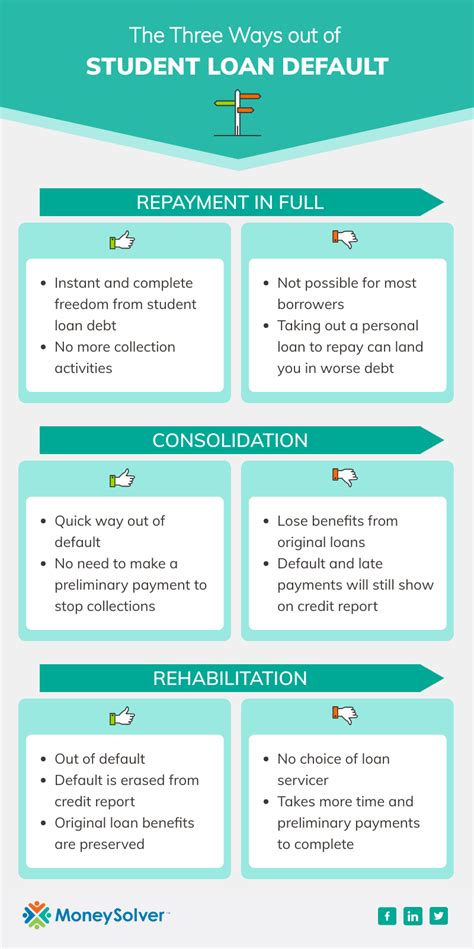

3. Exploring Rehabilitation Options:

Several options exist to rehabilitate defaulted private student loans. These vary considerably based on your individual circumstances, the lender's policies, and the type of loan.

-

Rehabilitation Programs: Some lenders offer formal rehabilitation programs. These usually involve making a series of on-time payments, often for a specific period (e.g., nine consecutive months). Successful completion of the program can reinstate the loan to good standing and remove the default from your credit report.

-

Loan Consolidation: Consolidating multiple private student loans into a single loan can simplify repayment. A lower monthly payment might be achievable, but it's crucial to carefully review the terms, as interest rates and the total repayment amount could potentially increase.

-

Repayment Plans: Negotiating a new repayment plan with the lender is a viable option. This might involve extending the repayment period or adjusting the monthly payment amount to suit your current financial situation. However, remember that extending the repayment period will often increase the total interest paid over the life of the loan.

-

Settlement: In some cases, a lender might agree to a loan settlement, where you pay a lump sum less than the total debt owed. This is typically a last resort and often requires significant negotiation. A settlement will negatively impact your credit score, but it can be preferable to long-term collection efforts.

4. Negotiating with Lenders:

Negotiation requires careful preparation. Gather all relevant documentation, including your loan agreement, income statements, and any other financial documents that support your case. Present a clear and concise explanation of your financial situation and propose a feasible repayment plan. Be prepared to compromise and be persistent. It may take multiple attempts to reach a mutually agreeable solution.

5. Protecting Your Rights:

Understand your rights as a borrower under the Fair Debt Collection Practices Act (FDCPA) and other relevant consumer protection laws. Be wary of predatory collection practices and document all communication with lenders and collection agencies. If you feel your rights are being violated, seek legal counsel.

6. Building a Budget and Creating a Realistic Repayment Plan:

Rehabilitation requires a comprehensive understanding of your financial situation. Create a detailed budget to identify areas where you can reduce spending and allocate funds towards your student loan payments. Developing a sustainable repayment plan, that aligns with your budget, is crucial for long-term success. Consider utilizing budgeting apps or seeking guidance from a financial advisor.

7. Credit Repair Strategies:

After successfully rehabilitating your loan, focus on repairing your credit. This involves consistently making on-time payments on all your debts, monitoring your credit reports for inaccuracies, and utilizing credit-building strategies, such as secured credit cards. Repairing your credit will take time and effort, but it's essential for securing future financial opportunities.

Exploring the Connection Between Credit Counseling and Getting Private Student Loans Out of Default:

Credit counseling agencies, such as those accredited by the NFCC, can play a significant role in navigating the complexities of defaulted private student loans. They provide expert guidance on budgeting, debt management, and negotiating with creditors. They can help borrowers develop a comprehensive debt management plan and act as intermediaries between borrowers and lenders. While credit counseling services are generally not free, they often provide valuable support and guidance during this challenging process.

Key Factors to Consider:

-

Roles and Real-World Examples: Credit counselors can help create personalized debt management plans, negotiate lower interest rates, or consolidate debts to make repayments more manageable. They can even offer support in navigating the emotional stress associated with debt.

-

Risks and Mitigations: While credit counseling offers significant benefits, it’s crucial to choose a reputable, NFCC-accredited agency. Avoid companies promising unrealistic results or charging exorbitant fees.

-

Impact and Implications: Utilizing credit counseling services can significantly improve the chances of successful loan rehabilitation, leading to improved credit scores, reduced stress, and better financial well-being.

Conclusion: Reinforcing the Connection:

The relationship between credit counseling and private student loan rehabilitation is symbiotic. Credit counselors provide invaluable support and expertise, empowering borrowers to navigate the intricacies of the process and achieve positive outcomes. Their guidance allows borrowers to regain control of their finances and build a pathway to a more secure financial future.

Further Analysis: Examining Credit Counseling Agencies in Greater Detail:

Choosing the right credit counseling agency is crucial. Look for agencies accredited by the NFCC, ensuring they adhere to ethical and professional standards. Thoroughly review their services, fees, and client testimonials before engaging their services. Understand their approach to debt management and make sure their strategy aligns with your personal goals and financial situation.

FAQ Section: Answering Common Questions About Getting Private Student Loans Out of Default:

Q: What happens if I ignore my defaulted private student loans?

A: Ignoring defaulted loans will likely result in further damage to your credit score, potential wage garnishment, legal action, and continued collection efforts.

Q: Can I negotiate a lower payment amount with my lender?

A: It's possible. The likelihood of success depends on your financial circumstances, the lender's policies, and your ability to negotiate effectively.

Q: Will rehabilitation remove the default from my credit report?

A: This depends on the lender and the specifics of the rehabilitation program. Successful completion may lead to the removal of the default, but it's not guaranteed.

Q: How long does the rehabilitation process take?

A: The duration varies based on the chosen rehabilitation method, the lender’s requirements, and the borrower's adherence to the agreed-upon repayment plan.

Q: What if I can't afford any payments?

A: Explore options such as bankruptcy or seeking assistance from non-profit organizations that offer financial aid and counseling.

Practical Tips: Maximizing the Benefits of Private Student Loan Rehabilitation:

-

Act Quickly: Contact your lender as soon as possible to initiate the rehabilitation process.

-

Document Everything: Keep meticulous records of all communication, payments, and agreements.

-

Be Honest and Transparent: Provide accurate information about your financial situation.

-

Seek Professional Help: Consider consulting with a credit counselor or financial advisor for guidance.

-

Stay Organized: Develop a system to track your payments and communication with your lender.

Final Conclusion: Wrapping Up with Lasting Insights:

Rehabilitating defaulted private student loans is a challenging but achievable goal. By understanding the process, exploring available options, and actively engaging with lenders, borrowers can regain control of their finances and build a path towards financial stability. Proactive communication, careful planning, and potentially seeking professional guidance are crucial elements in successfully navigating this process and securing a brighter financial future. Remember that the journey might be challenging, but regaining control of your financial health is possible with careful planning and dedication.

Latest Posts

Latest Posts

-

Intercompany Products Suits Exclusion Definition

Apr 24, 2025

-

Intercommodity Spread Definition

Apr 24, 2025

-

Interchange Rate Definition Calculation Factors Examples

Apr 24, 2025

-

Interchange Definition

Apr 24, 2025

-

What Is The Interbank Rate Definition How It Works And Example

Apr 24, 2025

Related Post

Thank you for visiting our website which covers about How To Get Private Student Loans Out Of Default . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.