How To Request A Lower Minimum Payment On Credit Card

adminse

Apr 04, 2025 · 8 min read

Table of Contents

How to Request a Lower Minimum Payment on Your Credit Card: A Comprehensive Guide

What if navigating your credit card payments felt less burdensome? Successfully negotiating a lower minimum payment is achievable with the right strategy and approach.

Editor’s Note: This article on requesting a lower minimum payment on your credit card was published today, providing you with the most up-to-date information and strategies to manage your credit card debt effectively.

Why Lowering Your Minimum Payment Matters:

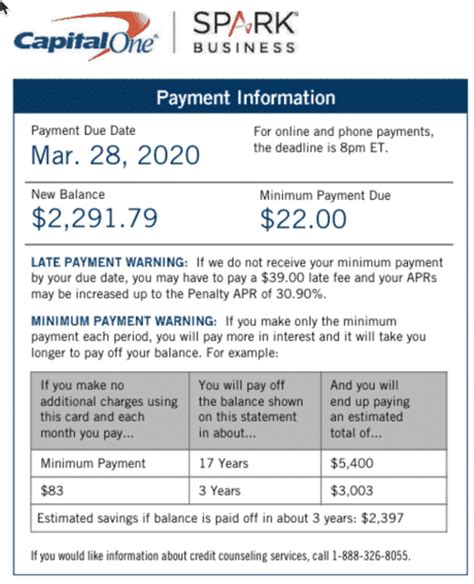

The minimum payment on your credit card statement might seem like a small, manageable amount, but consistently only paying the minimum can significantly hinder your financial progress. It often leads to accumulating more interest than principal, prolonging the repayment period and ultimately costing you far more in the long run. A lower minimum payment, while not solving the underlying debt problem, can provide temporary breathing room to manage your finances better and potentially accelerate debt reduction through increased payments whenever possible. It’s crucial to remember that a lower minimum payment doesn't reduce your total debt; it only changes how much you pay each month.

Overview: What This Article Covers:

This article comprehensively explores the strategies and tactics for successfully requesting a lower minimum payment from your credit card issuer. We will delve into understanding your credit card agreement, crafting a persuasive request, navigating potential challenges, and exploring alternative solutions to manage your debt more effectively. You'll gain actionable insights, supported by practical examples and expert advice.

The Research and Effort Behind the Insights:

This article is based on extensive research, drawing upon consumer finance regulations, credit card company policies, and best practices for debt management. We've analyzed numerous consumer experiences and consulted relevant financial resources to provide you with accurate and reliable information. The information presented aims to empower you to make informed decisions regarding your credit card debt.

Key Takeaways:

- Understanding Your Credit Agreement: Familiarize yourself with your credit card's terms and conditions.

- Crafting a Persuasive Request: Learn how to communicate your financial situation effectively.

- Navigating Potential Challenges: Understand potential objections from your issuer and prepare counterarguments.

- Exploring Alternative Solutions: Consider debt consolidation, balance transfers, or credit counseling.

- Maintaining Good Credit: Understand the impact of negotiating a lower minimum payment on your credit score.

Smooth Transition to the Core Discussion:

Now that we understand why lowering your minimum payment can be beneficial (within the context of a broader debt management strategy), let's delve into the practical steps involved in requesting this change.

Exploring the Key Aspects of Requesting a Lower Minimum Payment:

1. Understanding Your Credit Card Agreement:

Before you initiate a request, thoroughly review your credit card agreement. It outlines the terms and conditions, including the minimum payment calculation method. While there's no guarantee of success, understanding your rights and the issuer's policies will strengthen your position. Look for clauses that address hardship or temporary payment reductions.

2. Assessing Your Financial Situation:

Before contacting your credit card issuer, honestly assess your financial situation. Identify the specific reasons for needing a lower minimum payment. This might include unexpected job loss, medical expenses, or a significant decrease in income. Gather supporting documentation, such as pay stubs, medical bills, or proof of reduced income, to strengthen your request. Be prepared to explain your situation clearly and concisely.

3. Crafting a Persuasive Request:

A well-written request significantly increases your chances of success. Your communication should be polite, professional, and concise. Avoid accusatory or demanding language.

Here's a sample letter you can adapt:

Subject: Request for Temporary Minimum Payment Reduction – Account [Your Account Number]

Dear [Credit Card Company Name],

I am writing to request a temporary reduction in the minimum payment on my credit card account, [Your Account Number]. Due to [Clearly explain your financial hardship – be specific and honest, e.g., unexpected job loss, medical emergency, etc.], I am currently facing financial difficulties that make it challenging to meet the current minimum payment of [Current Minimum Payment Amount].

I have been a loyal customer for [Number] years and have always made timely payments until this unforeseen circumstance. I am requesting a temporary reduction to [Proposed Lower Minimum Payment Amount] for [Number] months. I understand that this is a temporary measure, and I am committed to resuming my regular payments as soon as my financial situation improves. I have attached supporting documentation [mention any supporting documents like pay stubs, etc.].

I would appreciate the opportunity to discuss this matter further and find a mutually agreeable solution. You can reach me at [Your Phone Number] or [Your Email Address].

Thank you for your time and consideration.

Sincerely,

[Your Name]

4. Choosing Your Communication Method:

You can choose to communicate via phone, mail, or online. A phone call often allows for more immediate feedback and negotiation, but a written letter provides a documented record of your request. Online portals usually have a messaging system for contacting customer service. Choose the method that you feel most comfortable with.

5. Navigating Potential Challenges:

Credit card companies might be hesitant to reduce minimum payments. They might request additional information, question the validity of your claim, or offer alternative solutions. Be prepared for these possibilities and have counterarguments ready. For example, if they ask for additional documentation, provide it promptly. If they suggest alternative solutions that you find unsuitable, explain why and reiterate your request for a lower minimum payment.

6. Exploring Alternative Solutions:

If your request for a lower minimum payment is denied, explore alternative debt management strategies. These include:

- Debt Consolidation: Combining multiple debts into a single loan with a potentially lower interest rate.

- Balance Transfers: Transferring your balance to a new credit card with a 0% introductory APR. Be aware of balance transfer fees and the APR after the introductory period ends.

- Credit Counseling: Seeking guidance from a non-profit credit counseling agency to create a debt management plan.

Exploring the Connection Between Effective Communication and Successful Negotiation:

Effective communication is pivotal to successfully negotiating a lower minimum payment. Clear, concise, and honest communication demonstrates your commitment to resolving the situation. Providing supporting documentation adds credibility to your claim. A respectful and professional tone fosters a positive dialogue with the credit card issuer, increasing your chances of a favorable outcome.

Key Factors to Consider:

- Roles and Real-World Examples: A single mother facing unexpected medical bills successfully negotiated a reduced minimum payment by providing medical records and proof of reduced income.

- Risks and Mitigations: Failing to meet even the reduced minimum payment can negatively impact your credit score. To mitigate this, diligently track your payments and communicate any unforeseen changes in your financial situation promptly.

- Impact and Implications: Negotiating a lower minimum payment can provide temporary relief but doesn't eliminate the debt. A long-term debt management strategy is necessary to avoid further accumulation of interest and fees.

Conclusion: Reinforcing the Connection:

The interplay between clear communication, a well-documented financial hardship, and a proactive approach are key to successfully negotiating a lower minimum payment. While this isn't a long-term solution to debt, it can offer crucial breathing room to create a sustainable debt repayment plan.

Further Analysis: Examining Financial Hardship in Greater Detail:

Financial hardship can manifest in various ways, from unexpected job loss and medical emergencies to natural disasters and unforeseen family expenses. Each situation requires a unique approach when communicating with credit card issuers. The key is to be honest, transparent, and prepared to provide supporting documentation that validates your claim.

FAQ Section: Answering Common Questions About Requesting a Lower Minimum Payment:

Q: What if my request is denied?

A: If your request is denied, explore alternative debt management solutions like debt consolidation or balance transfers. You can also contact a non-profit credit counseling agency for assistance.

Q: Will lowering my minimum payment affect my credit score?

A: While consistently making even reduced minimum payments is better than missing payments entirely, it's important to remember that a lower minimum payment does not directly improve your credit score. Consistent on-time payments, even if smaller than the original minimum, can help maintain your credit score. However, late payments, regardless of the payment amount, will negatively affect your credit score.

Q: How long can I keep a lower minimum payment?

A: The duration of a reduced minimum payment is usually temporary and negotiated with the credit card issuer. They might set a time frame or require you to demonstrate improved financial stability before returning to the regular minimum payment.

Q: Can I request a lower minimum payment multiple times?

A: Repeatedly requesting lower minimum payments may negatively impact your relationship with the credit card issuer. It's generally advisable to avoid frequent requests unless your financial circumstances drastically change.

Practical Tips: Maximizing the Benefits of a Lower Minimum Payment:

-

Budget Carefully: Create a detailed budget to track your income and expenses and identify areas where you can reduce spending.

-

Prioritize Payments: Focus on paying off high-interest debts first to minimize the overall interest burden.

-

Seek Professional Help: If you're struggling to manage your debt, consider seeking guidance from a financial advisor or a non-profit credit counseling agency.

Final Conclusion: Wrapping Up with Lasting Insights:

Requesting a lower minimum payment on your credit card can be a valuable tool for navigating temporary financial hardship. However, it's crucial to approach this strategically, crafting a compelling request supported by documentation and understanding the potential implications for your credit score. Remember that a lower minimum payment is a short-term solution, and a long-term debt management plan is essential for sustainable financial health. Proactive planning and responsible debt management are key to achieving long-term financial success.

Latest Posts

Latest Posts

-

Whats The Minimum Payment For Ssi

Apr 05, 2025

-

What Is The Minimum Ssdi Disability Payment

Apr 05, 2025

-

What Is The Minimum Social Security Disability Payment Per Month

Apr 05, 2025

-

What Is The Minimum Payment For Disability

Apr 05, 2025

-

What Is The Minimum Ssdi Monthly Payment

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How To Request A Lower Minimum Payment On Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.