How To Figure Out Minimum Payment On Line Of Credit

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Decoding Your Line of Credit Minimum Payment: A Comprehensive Guide

What if understanding your line of credit minimum payment unlocks significant long-term savings and financial stability? Mastering this seemingly simple calculation is crucial for responsible credit management and achieving your financial goals.

Editor’s Note: This article on calculating minimum payments for lines of credit was published today and provides up-to-date information and strategies for managing your credit responsibly.

Why Understanding Your Line of Credit Minimum Payment Matters:

Understanding your line of credit minimum payment is not just about avoiding late fees; it's a cornerstone of effective personal finance. Failing to grasp this fundamental aspect of credit management can lead to accumulating high interest charges, damaging your credit score, and ultimately hindering your financial progress. Knowing your minimum payment allows you to budget effectively, prioritize debt repayment, and make informed decisions about your spending. This knowledge empowers you to navigate the complexities of credit responsibly and build a solid financial foundation.

Overview: What This Article Covers:

This article provides a comprehensive guide to understanding and calculating minimum payments on lines of credit. We'll explore different calculation methods used by lenders, the factors influencing minimum payments, the implications of only paying the minimum, strategies for minimizing interest charges, and resources to help you manage your credit effectively. Readers will gain practical insights and actionable strategies to manage their line of credit responsibly.

The Research and Effort Behind the Insights:

This article is the result of extensive research, incorporating information from reputable financial institutions, consumer protection agencies, and legal resources related to credit agreements. The information presented is based on commonly used practices and regulations, but individual lender policies may vary. It's always advisable to refer to your specific credit agreement for the most accurate details regarding your minimum payment calculation.

Key Takeaways:

- Definition and Calculation Methods: Understanding how minimum payments are typically calculated, including the influence of interest rates and outstanding balances.

- Factors Affecting Minimum Payments: Identifying the variables that lenders consider when determining your minimum payment.

- Consequences of Only Paying the Minimum: Analyzing the long-term financial implications of consistently paying only the minimum payment.

- Strategies for Accelerated Repayment: Exploring strategies to pay down your line of credit faster and reduce interest charges.

- Resources and Support: Identifying resources available to help you manage your debt and credit effectively.

Smooth Transition to the Core Discussion:

Now that we understand the importance of understanding your minimum payment, let’s delve into the specifics of how these payments are calculated and the factors involved.

Exploring the Key Aspects of Line of Credit Minimum Payment Calculations:

1. Definition and Core Concepts:

A line of credit is a revolving credit account that allows you to borrow money up to a pre-approved limit. Unlike a loan with a fixed repayment schedule, you can borrow and repay funds repeatedly as needed. The minimum payment is the smallest amount you're required to pay each billing cycle to avoid late fees and remain in good standing with your lender. Failure to make at least the minimum payment can result in penalties and negatively impact your credit score.

2. Calculation Methods:

There isn't one universal formula for calculating minimum payments on lines of credit. Lenders employ various methods, but common approaches include:

-

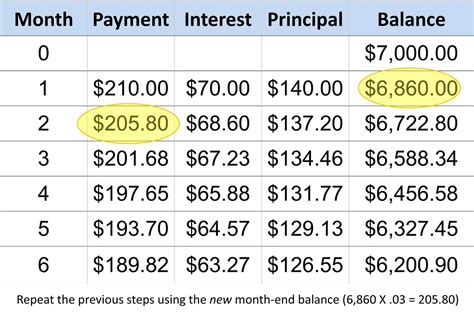

Percentage of Balance: Many lenders calculate the minimum payment as a percentage of your outstanding balance (e.g., 1% or 2%). This means the minimum payment will fluctuate each month depending on your balance. A higher balance will result in a higher minimum payment.

-

Fixed Minimum Payment: Some lenders set a fixed minimum payment regardless of the outstanding balance. This amount might be a small dollar amount (e.g., $25) or a slightly higher figure. While this offers predictability, it can take significantly longer to repay the balance.

-

Combination Approach: Some lenders use a combination of these approaches, perhaps setting a minimum percentage of the balance, but also ensuring the payment is at least a certain minimum dollar amount.

3. Factors Affecting Minimum Payments:

Several factors influence the minimum payment calculation:

-

Outstanding Balance: The higher your outstanding balance, the higher your minimum payment (generally, when a percentage-based method is used).

-

Interest Rate (APR): While not directly used in all minimum payment calculations, the annual percentage rate (APR) significantly impacts the overall cost of borrowing. A higher APR means you'll pay more in interest over time, even if your minimum payments are consistently made.

-

Lender's Policies: Each lender has its own policies and calculation methods. Review your credit agreement carefully to understand your lender's specific approach.

-

Payment History: While not directly involved in the calculation itself, a history of late or missed payments might prompt a lender to increase the minimum payment or impose stricter terms.

4. Impact on Innovation:

The evolution of online banking and digital financial services has made accessing and understanding line of credit information easier than ever before. Online portals and mobile apps provide real-time access to account balances, transaction histories, and minimum payment details. This increased transparency empowers consumers to make more informed decisions about their credit management.

Closing Insights: Summarizing the Core Discussion:

Understanding your line of credit minimum payment is essential for responsible credit management. While calculation methods vary, understanding the factors involved – balance, interest rate, and lender policies – allows for informed decision-making. Failing to meet minimum payments can lead to severe financial consequences.

Exploring the Connection Between Interest Rates and Line of Credit Minimum Payments:

The relationship between interest rates and minimum payments is indirect but profoundly impactful. The interest rate (APR) doesn't directly determine the minimum payment amount in many cases, but it significantly influences the overall cost of borrowing and the time it takes to repay the balance. A higher APR means a larger portion of your payment goes towards interest, leaving less to reduce the principal balance. This can lead to a longer repayment period and significantly higher total interest paid over the life of the credit line.

Key Factors to Consider:

Roles and Real-World Examples: Imagine two individuals with the same outstanding balance but different APRs. The individual with the higher APR will likely pay more in interest each month, even if their minimum payment is the same. This difference compounds over time, leading to substantially different total repayment costs.

Risks and Mitigations: The risk of focusing solely on minimum payments is the extended repayment period and the accumulation of significant interest charges. Mitigation strategies include paying more than the minimum whenever possible, exploring debt consolidation options, and proactively negotiating a lower APR with your lender.

Impact and Implications: The long-term implications of consistently paying only the minimum can be severe, potentially leading to increased debt burden, damaged credit score, and difficulty accessing future credit.

Conclusion: Reinforcing the Connection:

The connection between interest rates and minimum payments underscores the importance of understanding the overall cost of borrowing. By minimizing interest charges through strategic repayment and responsible credit management, individuals can achieve better financial outcomes.

Further Analysis: Examining APRs in Greater Detail:

The annual percentage rate (APR) represents the annual cost of borrowing, including interest and other fees. Understanding your APR is crucial because it directly impacts the total amount you pay over the life of your credit line. A higher APR means you'll pay more interest, even if you consistently meet minimum payments. Factors like your credit score, the type of credit line, and the lender's policies all influence the APR offered.

FAQ Section: Answering Common Questions About Line of Credit Minimum Payments:

What if I can't afford the minimum payment? Contact your lender immediately to discuss potential solutions, such as a hardship program or a repayment plan. Ignoring the problem will only worsen the situation.

Where can I find my minimum payment information? Check your monthly statement, online account portal, or contact your lender directly.

Will paying more than the minimum affect my credit score? No, paying more than the minimum payment will not negatively impact your credit score. In fact, it can improve your credit utilization ratio (the percentage of your available credit you're using), which is a positive factor in credit scoring models.

What happens if I miss a minimum payment? Late fees will be assessed, and your credit score will likely be negatively impacted. Repeated missed payments can lead to account closure and further damage to your credit.

Practical Tips: Maximizing the Benefits of Understanding Your Minimum Payment:

-

Check your statement carefully: Review your monthly statement thoroughly to understand your outstanding balance, minimum payment amount, and APR.

-

Budget effectively: Incorporate your minimum payment into your monthly budget to ensure you can consistently make payments on time.

-

Pay more than the minimum: Whenever possible, pay more than the minimum payment to reduce your balance faster and save on interest charges.

-

Explore debt consolidation: Consider consolidating high-interest debts into a lower-interest loan or credit line to reduce your overall borrowing costs.

-

Monitor your credit report: Regularly check your credit report for accuracy and to monitor your credit utilization ratio.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding your line of credit minimum payment is a critical component of responsible financial management. By understanding how these payments are calculated, the factors that influence them, and the consequences of consistently paying only the minimum, you can take proactive steps to manage your debt effectively and achieve long-term financial stability. Remember, consistent on-time payments, coupled with strategic repayment strategies, can significantly reduce your debt burden and improve your overall financial well-being.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On American Express Gold Card

Apr 06, 2025

-

Why Do Capital One Payments Take So Long

Apr 06, 2025

-

How Long Does Capital One Take To Process A Payment

Apr 06, 2025

-

How Long Do Capital One Payments Take

Apr 06, 2025

-

How Long Do Capital One Payments Take To Post

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about How To Figure Out Minimum Payment On Line Of Credit . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.