How To Dispute A Late Payment On Transunion

adminse

Apr 03, 2025 · 7 min read

Table of Contents

How to Dispute a Late Payment on TransUnion: A Comprehensive Guide

What if a single late payment unfairly tanks your credit score? Disputing inaccurate information on your TransUnion report is a crucial step in protecting your financial health.

Editor’s Note: This comprehensive guide on disputing late payments on your TransUnion credit report was published today. The information provided is current and based on established procedures. Always verify information directly with TransUnion for the most up-to-date details.

Why Disputing Late Payments on TransUnion Matters:

A late payment reported to TransUnion can significantly impact your credit score, potentially affecting your ability to secure loans, rent an apartment, or even get a job. Even a single inaccurate late payment can have lasting consequences. Therefore, understanding how to effectively dispute such entries is paramount to protecting your creditworthiness. This involves meticulously examining your report, gathering supporting evidence, and navigating the dispute process efficiently. The potential benefits – restoring your credit score and preventing future financial setbacks – make the effort worthwhile.

Overview: What This Article Covers:

This article offers a step-by-step guide to disputing a late payment on your TransUnion credit report. It covers understanding the process, gathering necessary documentation, submitting your dispute, understanding potential outcomes, and steps to take if your dispute is unsuccessful. We'll also address common questions and provide practical tips to improve your chances of a successful resolution.

The Research and Effort Behind the Insights:

This guide is based on thorough research of TransUnion's official dispute process, consumer protection laws, and best practices for credit repair. We've consulted numerous reputable sources, including government websites, consumer advocacy organizations, and expert opinions to ensure the accuracy and reliability of the information presented.

Key Takeaways:

- Understanding the Dispute Process: Learn the steps involved in submitting a formal dispute to TransUnion.

- Gathering Supporting Evidence: Discover the types of documentation needed to support your claim.

- Submitting Your Dispute: Understand the different methods for submitting a dispute and the importance of accuracy.

- Potential Outcomes and Next Steps: Learn what happens after you submit your dispute and how to proceed if it’s unsuccessful.

- Prevention Strategies: Learn how to avoid late payments in the future.

Smooth Transition to the Core Discussion:

Now that we understand the importance of disputing inaccurate late payments, let’s delve into the specifics of how to navigate the TransUnion dispute process effectively.

Exploring the Key Aspects of Disputing a Late Payment on TransUnion:

1. Verify the Accuracy of the Late Payment:

Before initiating a dispute, meticulously review your TransUnion credit report. Confirm that the reported late payment is indeed accurate in terms of the creditor, the date, and the amount. Even a minor discrepancy can be grounds for a dispute. Check the following:

- Creditor Name: Is the creditor correctly identified? A misspelling or incorrect name can indicate an error.

- Date of Late Payment: Is the date accurate? If you believe the date is wrong, gather proof such as bank statements or payment confirmations.

- Amount Owed: Does the amount match your records? Discrepancies could signify an accounting error.

- Account Number: Verify the account number is correct.

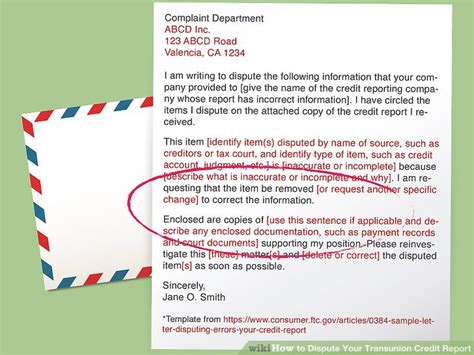

2. Gather Supporting Documentation:

Strong documentation is crucial for a successful dispute. Gather evidence that proves the late payment is inaccurate or should be removed. This may include:

- Proof of Payment: This could be a bank statement showing the payment was made on time, a canceled check, a money order receipt, or an online payment confirmation.

- Payment Agreements: If you had a payment arrangement with the creditor, provide documentation outlining the terms.

- Correspondence with the Creditor: Any emails, letters, or other communications that demonstrate your attempts to resolve the issue with the creditor should be included.

- Dispute Letter Template: TransUnion’s website may provide a template to guide you in writing a clear and concise letter.

3. Submitting Your Dispute to TransUnion:

TransUnion offers several ways to submit a dispute:

- Online: The easiest method is usually through TransUnion's website. Their online portal generally guides you through the process and allows you to upload supporting documents.

- Mail: You can mail your dispute letter and supporting documentation to the TransUnion address specified on their website. Ensure you use certified mail with return receipt requested for proof of delivery.

- Phone: While less common, you might be able to initiate a dispute over the phone. However, it's best to follow up with a written dispute letter and supporting documentation.

4. The Investigation Process:

Once TransUnion receives your dispute, they'll investigate the matter. This usually involves contacting the creditor to verify the accuracy of the reported information. The investigation process can take 30-45 days or longer.

5. Potential Outcomes:

- Verification: TransUnion might verify the accuracy of the late payment and leave the information on your report.

- Removal: If TransUnion finds the information inaccurate or incomplete, they may remove the late payment.

- Correction: The late payment might be corrected (e.g., the date is changed).

6. Next Steps If Your Dispute is Unsuccessful:

If TransUnion doesn't remove the late payment, you can:

- Resubmit your dispute: Provide additional evidence or clarify points in your initial dispute.

- Contact the creditor directly: Attempt to resolve the issue directly with the creditor. A corrected report from the creditor can strengthen your case for a second dispute.

- File a complaint with the Consumer Financial Protection Bureau (CFPB): The CFPB is a federal agency that protects consumers' financial interests.

Exploring the Connection Between Credit Repair Companies and Disputing Late Payments:

While you can certainly handle the dispute yourself, credit repair companies offer assistance in navigating the complex process. They typically charge a fee, but they can simplify the process and potentially improve your chances of success. However, thoroughly research any credit repair company before engaging their services. Be wary of companies making unrealistic claims or employing high-pressure sales tactics.

Key Factors to Consider When Using Credit Repair Companies:

- Transparency and Fees: Understand exactly what services they offer and the associated costs.

- Experience and Reputation: Check online reviews and ratings to assess their track record.

- Contracts and Guarantees: Read the contract carefully and understand any guarantees or limitations.

- FTC Compliance: Ensure the company adheres to the Fair Credit Reporting Act (FCRA) regulations.

Further Analysis: Examining the Fair Credit Reporting Act (FCRA) in Greater Detail:

The FCRA is a federal law that protects consumers' rights related to their credit reports. It dictates how credit reporting agencies, including TransUnion, must handle disputes and ensures fairness and accuracy. Understanding the FCRA is essential when disputing inaccurate information. The FCRA gives you the right to:

- Obtain a free credit report annually: This allows you to monitor your credit report for errors.

- Dispute inaccurate information: You have the right to challenge any information you believe is incorrect.

- Receive notice of adverse actions: If your application for credit, insurance, or employment is denied due to your credit report, you're entitled to notification.

FAQ Section: Answering Common Questions About Disputing Late Payments on TransUnion:

Q: How long does the dispute process take?

A: The investigation typically takes 30-45 days, but it can sometimes take longer.

Q: What if I don’t have proof of payment?

A: This significantly reduces your chances of a successful dispute. However, you can still try by providing any other supporting documentation that might help your case.

Q: Can I dispute multiple late payments at once?

A: Yes, you can submit a single dispute for multiple late payments, as long as you provide supporting documentation for each.

Q: What if my dispute is denied?

A: You can try to resubmit your dispute with additional evidence, contact the creditor directly, or file a complaint with the CFPB.

Practical Tips: Maximizing the Benefits of the Dispute Process:

- Be Organized: Keep all documentation in order to avoid confusion.

- Be Persistent: Don't give up if your initial dispute is unsuccessful.

- Be Accurate: Ensure all information in your dispute letter is correct.

- Follow Up: After submitting your dispute, follow up with TransUnion to check on the status of your case.

Final Conclusion: Wrapping Up with Lasting Insights:

Disputing inaccurate late payments on your TransUnion credit report is a critical step in protecting your financial well-being. By understanding the process, gathering necessary documentation, and following the steps outlined above, you can significantly improve your chances of successfully resolving errors and maintaining a healthy credit score. Remember to stay proactive in monitoring your credit reports and taking steps to prevent future late payments. Your credit score is a valuable asset, and safeguarding it requires vigilance and proactive action.

Latest Posts

Latest Posts

-

What Is The Penalty For Late Electricity Bill Payment

Apr 04, 2025

-

What Is The Grace Period For Electric Bill

Apr 04, 2025

-

Apa Itu Liquidity Pool

Apr 04, 2025

-

What Is Liquidity Pool

Apr 04, 2025

-

Liquidity Pool Crypto Adalah

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about How To Dispute A Late Payment On Transunion . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.