How To Calculate Credit Card Utilization Ratio

adminse

Apr 07, 2025 · 9 min read

Table of Contents

How to Master Your Credit Score: Decoding Credit Card Utilization Ratio

Understanding your credit utilization ratio is crucial for building a strong credit profile. It significantly impacts your credit score, influencing your access to loans and interest rates.

Editor’s Note: This article on calculating credit card utilization ratio was published today, providing you with the most up-to-date information and strategies to manage your credit effectively.

Why Credit Card Utilization Ratio Matters

Your credit utilization ratio is a key factor in determining your creditworthiness. Lenders use it to assess your risk profile, gauging how responsibly you manage your credit. A high utilization ratio signals potential financial instability, leading to higher interest rates or even loan denials. Conversely, a low utilization ratio reflects responsible credit management, potentially improving your credit score and access to better financial opportunities. This ratio influences not only credit card approvals but also loan applications for mortgages, auto loans, and personal loans. Understanding and managing this ratio is crucial for long-term financial health.

Overview: What This Article Covers

This article provides a comprehensive guide to understanding and calculating your credit card utilization ratio. We will cover the definition, various methods of calculation, the ideal utilization rate, strategies for improvement, and frequently asked questions. You will gain actionable insights to optimize your credit profile and improve your financial well-being.

The Research and Effort Behind the Insights

This article is based on extensive research, incorporating information from leading credit bureaus, financial experts, and reputable financial websites. We've compiled data from multiple sources to provide accurate and trustworthy information, empowering you to make informed decisions about your credit management.

Key Takeaways:

- Definition of Credit Utilization Ratio: A clear explanation of what credit utilization means.

- Calculation Methods: Step-by-step instructions on calculating your ratio, addressing both individual cards and overall credit.

- Ideal Utilization Rate: Understanding the range that benefits your credit score.

- Strategies for Improvement: Actionable steps to lower your utilization ratio.

- Impact on Credit Score: How your utilization ratio directly affects your score.

- Addressing Common Misconceptions: Clearing up common misunderstandings about credit utilization.

Smooth Transition to the Core Discussion

Now that we understand the importance of credit utilization, let's delve into the specifics of calculating this vital ratio and explore strategies for maintaining a healthy credit profile.

Exploring the Key Aspects of Credit Card Utilization Ratio

Definition and Core Concepts

Your credit utilization ratio is the percentage of your available credit that you're currently using. It's calculated by dividing your total credit card debt by your total available credit. This ratio provides lenders with an indication of your debt-to-credit capacity. A low ratio demonstrates responsible credit management, while a high ratio suggests potential overspending and increased financial risk.

Calculating Your Credit Utilization Ratio: A Step-by-Step Guide

Method 1: Calculating for Individual Credit Cards

-

Find your credit limit: Check your credit card statement for your total available credit. This is the maximum amount you can borrow.

-

Find your current balance: Note the outstanding balance on your statement. This is the amount you owe.

-

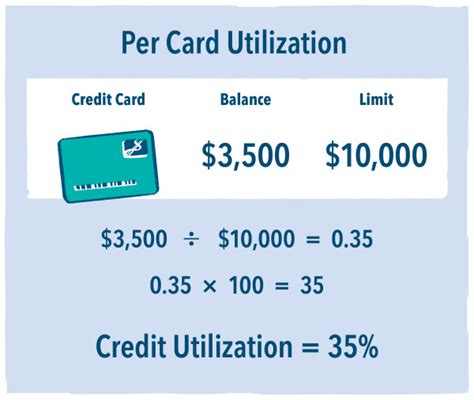

Calculate the utilization ratio: Divide your current balance by your credit limit and multiply by 100 to express it as a percentage.

Utilization Ratio (%) = (Current Balance / Credit Limit) x 100

For example, if your credit limit is $1000 and your current balance is $200, your utilization ratio is (200/1000) x 100 = 20%.

Method 2: Calculating Your Overall Credit Utilization Ratio

This method is more complex and requires collecting data from all your credit cards.

-

Total Available Credit: Add up the credit limits across all your credit cards.

-

Total Outstanding Balance: Sum up the outstanding balances on all your credit cards.

-

Overall Utilization Ratio: Divide your total outstanding balance by your total available credit and multiply by 100.

Overall Utilization Ratio (%) = (Total Outstanding Balance / Total Available Credit) x 100

The Ideal Credit Utilization Ratio

While there's no universally agreed-upon magic number, financial experts generally recommend keeping your credit utilization ratio below 30%. Aiming for a utilization ratio of 10% or less is even better, as this demonstrates excellent credit management to lenders. However, some experts suggest that even a ratio below 30% can help maintain or improve credit scores.

Strategies for Improving Your Credit Utilization Ratio

-

Pay Down Your Balances: The most direct way to lower your utilization ratio is to pay down your outstanding credit card balances. Focus on high-utilization cards first. Consider making extra payments beyond your minimum due.

-

Increase Your Credit Limits: Contact your credit card issuer and request a credit limit increase. This will lower your utilization ratio without changing your outstanding balance. However, only pursue this if you're confident you can manage increased credit responsibly.

-

Open a New Credit Card: Opening a new credit card with a high credit limit can also reduce your overall utilization ratio. Choose a card with a low interest rate and avoid using it excessively. Use this strategically and always prioritize paying down existing balances.

-

Regularly Monitor Your Credit Reports: Regularly check your credit reports from all three major credit bureaus (Equifax, Experian, and TransUnion) for errors. Address any discrepancies promptly.

-

Use Credit Cards Wisely: Avoid maxing out your credit cards. Use credit cards for purchases you can comfortably afford to pay off in full each month. Plan your spending and stick to your budget.

-

Pay on Time: Always pay your credit card bills on time, as late payments negatively impact your credit score.

Impact on Your Credit Score

Your credit utilization ratio is a significant factor in your FICO credit score, one of the most widely used credit scoring models. A high utilization ratio negatively affects your score, as it shows lenders that you are using a significant portion of your available credit, suggesting a higher risk of default.

Addressing Common Misconceptions

Misconception 1: Closing Unused Credit Cards Improves Your Credit Score

While it might seem logical to close unused credit cards to simplify your finances, this can actually harm your credit score. Closing a card reduces your available credit, potentially increasing your utilization ratio, even if you don't use the card. It also reduces the length of your credit history, which is another scoring factor.

Misconception 2: Paying Your Balance in Full Each Month Doesn't Affect Your Score

Paying your balance in full each month is excellent for avoiding interest charges. However, it doesn't negate the impact of your utilization ratio on your credit score. Even if you pay in full, the reported balance before your payment is still factored into the calculation.

Misconception 3: A High Credit Limit Always Improves Your Score

A high credit limit can help lower your utilization ratio, but excessively high credit limits, without responsible management, can also negatively impact your score. Lenders might perceive someone with numerous high-limit cards as a higher risk, regardless of the utilization ratio.

Exploring the Connection Between Payment History and Credit Utilization Ratio

Payment history and credit utilization ratio are both vital components of your credit score. A good payment history (paying bills on time) demonstrates financial responsibility, while a low utilization ratio indicates that you're managing your credit wisely. The combination of a good payment history and low utilization ratio signifies strong creditworthiness.

Key Factors to Consider

Roles and Real-World Examples: A person with a consistent history of on-time payments but a high utilization ratio might still be perceived as a higher risk compared to someone with a slightly less perfect payment history but a much lower utilization ratio.

Risks and Mitigations: The risk of a high utilization ratio is a lower credit score and higher interest rates on future loans. Mitigation strategies involve actively paying down balances and potentially requesting credit limit increases.

Impact and Implications: The impact of a high utilization ratio can be long-lasting, affecting your ability to secure loans at favorable terms or even impacting your ability to rent an apartment.

Conclusion: Reinforcing the Connection

The relationship between payment history and credit utilization is synergistic. Both are crucial for a strong credit score. Responsible credit card management encompasses both timely payments and maintaining a low utilization ratio.

Further Analysis: Examining Payment History in Greater Detail

Consistent on-time payments are the cornerstone of a good credit history. This demonstrates responsible borrowing and reduces the perception of risk for lenders. Conversely, late or missed payments have a significant negative impact on your credit score, outweighing the benefits of even a low utilization ratio.

FAQ Section: Answering Common Questions About Credit Utilization Ratio

Q: What is the best credit utilization ratio? A: The ideal credit utilization ratio is below 30%, with 10% or less being even better.

Q: How often is my credit utilization ratio updated? A: Credit utilization is reported to credit bureaus monthly, based on the balances reported by your credit card issuers.

Q: Can I improve my credit utilization ratio quickly? A: Yes, by making extra payments on your high-utilization cards, you can lower your ratio relatively quickly.

Q: Will a low utilization ratio guarantee a loan approval? A: No, while a low utilization ratio is a crucial factor, other factors, such as payment history, length of credit history, and types of credit used, also influence loan approvals.

Practical Tips: Maximizing the Benefits of Credit Card Utilization

- Set up automatic payments: Automate your payments to avoid late fees and ensure on-time payments.

- Monitor your spending: Track your expenses regularly to prevent exceeding your budget and accumulating high balances.

- Use budgeting tools: Employ budgeting apps or spreadsheets to manage your finances and monitor your credit utilization.

- Review credit reports regularly: Check your credit reports for errors and identify potential areas for improvement.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding and managing your credit utilization ratio is crucial for building and maintaining a strong credit profile. By actively paying down debt, requesting credit limit increases responsibly, and regularly monitoring your credit reports, you can significantly improve your creditworthiness and access better financial opportunities. Remember, responsible credit card usage is a key element in achieving long-term financial stability.

Latest Posts

Latest Posts

-

Advance Refunding Definition

Apr 30, 2025

-

Advance Premium Fund Definition

Apr 30, 2025

-

Advance Premium Definition

Apr 30, 2025

-

Advance Funded Pension Plan Definition

Apr 30, 2025

-

Advance Commitment Definition

Apr 30, 2025

Related Post

Thank you for visiting our website which covers about How To Calculate Credit Card Utilization Ratio . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.