How Long Will It Take You To Pay The Debt If You Pay A Minimum Amount

adminse

Apr 05, 2025 · 7 min read

Table of Contents

How Long Will It Take to Pay Off Debt Paying Only the Minimum? A Deep Dive into Debt Repayment

How long will your debt haunt you if you only pay the minimum amount each month? The answer, unfortunately, is often much longer—and far more expensive—than you might imagine.

Editor's Note: This article provides a comprehensive analysis of minimum payment debt repayment timelines and the associated costs. The information presented is for educational purposes and should not be considered financial advice. Consult with a financial advisor for personalized guidance.

Why Minimum Payments Matter: A Costly Illusion of Progress

Many people find themselves trapped in a cycle of minimum debt payments, believing it's a manageable approach. However, this perception is often misleading. While minimum payments fulfill the immediate obligation and avoid late fees, they significantly prolong the repayment process and dramatically increase the total interest paid. Understanding the mechanics of compound interest and the long-term implications is crucial for effective debt management. This article will explore the factors influencing repayment time, using real-world examples and practical strategies to help you navigate this common financial challenge.

Overview: What This Article Covers

This comprehensive guide will dissect the complexities of minimum debt payments, covering:

- The Mechanics of Minimum Payments: Understanding how minimum payments are calculated and their impact on your debt.

- Calculating Repayment Time: Exploring various methods for estimating how long it takes to pay off debt with minimum payments.

- The Crushing Weight of Interest: Analyzing the substantial amount of interest accrued over extended repayment periods.

- Factors Affecting Repayment Time: Identifying variables like interest rates, initial debt amount, and payment consistency.

- The High Cost of Inaction: Highlighting the financial consequences of relying solely on minimum payments.

- Strategic Alternatives to Minimum Payments: Exploring more effective debt repayment strategies, such as debt snowball and debt avalanche methods.

- Real-World Scenarios and Case Studies: Illustrating the implications of minimum payments through practical examples.

- Frequently Asked Questions (FAQs): Addressing common queries about minimum payments and debt repayment.

- Practical Tips for Accelerated Debt Repayment: Offering actionable advice for faster debt elimination.

The Research and Effort Behind the Insights

This article incorporates data from reputable financial institutions, peer-reviewed studies on consumer debt, and analysis of commonly used debt calculation tools. The information presented aims to provide a realistic and evidence-based understanding of the challenges associated with minimum debt payments.

Definition and Core Concepts: Understanding Minimum Payments

Minimum payments are the smallest amount a borrower can pay on a debt each month without incurring late fees. These are typically calculated as a percentage of the outstanding balance or a fixed amount, whichever is greater. Credit card companies, loan providers, and other lenders specify the minimum payment requirements in their agreements. Crucially, these minimum payments primarily cover the interest accrued, leaving only a small portion to reduce the principal balance.

Applications Across Industries: The Prevalence of Minimum Payments

Minimum payment structures are prevalent across various debt types:

- Credit Cards: Credit card companies often set minimum payments at a low percentage (e.g., 2-3%) of the outstanding balance.

- Loans: Personal loans, auto loans, and mortgages usually have fixed minimum monthly payments outlined in the loan agreement.

- Student Loans: Federal and private student loans have varying minimum payment schedules, often based on the loan's repayment plan.

Challenges and Solutions: The Pitfalls of Minimum Payments

The primary challenge of relying solely on minimum payments is the significantly extended repayment period and the substantial accumulation of interest. This can trap individuals in a cycle of debt, hindering their financial progress.

Impact on Innovation: The Need for Better Financial Literacy

The widespread reliance on minimum payments underscores the need for improved financial literacy. Many individuals are unaware of the long-term costs associated with this approach, leading to poor financial decisions.

Smooth Transition to the Core Discussion: The Math of Minimum Payments

Understanding the math behind minimum payments is crucial for appreciating their long-term impact. Let's delve into how these calculations work and their consequences.

Exploring the Key Aspects of Minimum Payment Repayment

1. Calculating Repayment Time:

There's no single formula for calculating the exact repayment time with minimum payments. The time varies depending on factors such as:

- Interest Rate: Higher interest rates prolong repayment significantly.

- Initial Debt Amount: Larger debts naturally take longer to pay off.

- Minimum Payment Percentage: A lower minimum payment percentage extends repayment dramatically.

- Additional Charges: Fees and penalties can further extend the repayment period.

Several online calculators and debt repayment tools can help estimate the repayment timeframe based on these variables. However, it's crucial to input accurate information for an accurate prediction.

2. The Crushing Weight of Interest:

The primary drawback of minimum payments is the excessive interest paid over the long repayment period. Compound interest, where interest is calculated on both the principal and accumulated interest, accelerates this effect. The longer it takes to pay off the debt, the more interest you pay, essentially paying more for the initial debt amount.

3. Factors Affecting Repayment Time:

The variables mentioned earlier interact in complex ways to determine repayment time. For instance, even a small increase in the interest rate can significantly impact the repayment period. Similarly, consistent on-time payments, even if minimum, are vital to avoid late fees and further delays.

Exploring the Connection Between Interest Rates and Repayment Time

The interest rate is the most influential factor in determining how long it will take to repay debt using minimum payments. A higher interest rate means a larger portion of your payment goes towards interest, leaving less to reduce the principal. This creates a vicious cycle where your debt balance shrinks slowly, and the overall repayment time is significantly prolonged. A 1% increase in the interest rate can translate into years of added repayment time and thousands of dollars in extra interest.

Key Factors to Consider:

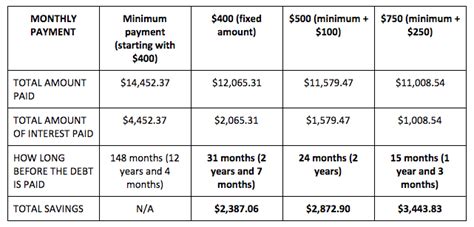

- Roles and Real-World Examples: Consider a credit card with a $5,000 balance and a 18% APR. The minimum payment might be $100. Using an online calculator, you'll find it takes years to pay this off, accruing thousands in interest.

- Risks and Mitigations: The primary risk is overspending and accumulating more debt during the extended repayment period. Mitigation strategies include budgeting, reducing spending, and exploring debt consolidation options.

- Impact and Implications: The long repayment time and high interest payments negatively impact credit scores, restrict financial flexibility, and limit opportunities for savings and investments.

Conclusion: Reinforcing the Connection

The relationship between interest rates and repayment time underscores the urgency of adopting proactive debt management strategies. High interest rates create a significant financial burden that can be mitigated by accelerating debt repayment.

Further Analysis: Examining the Impact of Missed Payments

Missed payments have a devastating effect on the repayment timeline. Beyond late fees, missed payments negatively impact credit scores, potentially leading to higher interest rates on future loans and reduced access to credit. This further delays debt repayment and amplifies the financial burden.

FAQ Section: Answering Common Questions About Minimum Payments

-

Q: Is it always bad to pay only the minimum payment? A: While convenient in the short term, solely relying on minimum payments significantly prolongs debt repayment and increases the total interest paid. It's generally advisable to pay more than the minimum whenever possible.

-

Q: How can I calculate my approximate repayment time? A: Several online debt calculators can provide estimates based on your debt amount, interest rate, and minimum payment.

-

Q: What if I can't afford to pay more than the minimum? A: Explore options such as debt consolidation, balance transfers to lower interest cards, or seeking financial counseling to develop a manageable repayment plan.

Practical Tips: Maximizing the Benefits (Minimizing the Drawbacks) of Minimum Payments

- Always pay on time: Avoiding late fees is crucial to prevent further delays and added costs.

- Pay more than the minimum whenever possible: Even small extra payments accelerate debt reduction.

- Track your progress: Regularly monitor your debt balance and repayment progress.

- Consider debt consolidation or balance transfers: These options can help lower interest rates and streamline repayment.

- Create a budget: A realistic budget helps manage spending and allocate funds toward debt repayment.

Final Conclusion: Wrapping Up with Lasting Insights

Paying only the minimum amount on your debt is a costly strategy that prolongs repayment and significantly increases the total interest paid. While it might seem manageable initially, the long-term financial implications are substantial. Proactive debt management, informed financial decisions, and exploration of alternative repayment strategies are vital for achieving financial freedom and avoiding the trap of prolonged debt repayment. Prioritize paying more than the minimum, explore options like debt consolidation or balance transfers, and build a budget to gain control of your financial future.

Latest Posts

Latest Posts

-

What Are Asset Management Skills

Apr 06, 2025

-

What Are Financial Management Skills

Apr 06, 2025

-

Money Management International

Apr 06, 2025

-

How Does Money Management International Work

Apr 06, 2025

-

What Are The 5 Principles Of Money

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about How Long Will It Take You To Pay The Debt If You Pay A Minimum Amount . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.