How Does Interest Work On Monthly Payments

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Unlocking the Mystery: How Interest Works on Monthly Payments

What if understanding how interest accrues on monthly payments unlocked a path to better financial decisions? Mastering this concept is key to responsible borrowing and achieving financial freedom.

Editor’s Note: This article on how interest works on monthly payments was published today, providing you with the latest insights into this crucial financial topic. We've broken down complex concepts into easy-to-understand explanations, empowering you to make informed decisions about your finances.

Why Understanding Interest on Monthly Payments Matters

Interest, the price paid for borrowing money, is a fundamental element of personal finance. Whether you're taking out a loan, using a credit card, or making installment payments, understanding how interest is calculated on your monthly payments is crucial. Ignoring this can lead to overspending, increased debt burdens, and missed opportunities for financial growth. The knowledge gained here will empower you to negotiate better loan terms, budget effectively, and ultimately, achieve your financial goals more efficiently. This understanding impacts everything from mortgages and auto loans to student loans and credit card debt.

Overview: What This Article Covers

This article provides a comprehensive overview of how interest accrues on monthly payments. We'll explore different interest calculation methods, dissect the components of a monthly payment, and delve into practical examples to illustrate these concepts clearly. Furthermore, we'll examine the impact of various factors, such as interest rates and loan terms, on the total interest paid. Finally, we’ll equip you with strategies to minimize interest payments and manage your debt effectively.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon established financial principles and incorporating real-world examples. The information presented is based on widely accepted financial calculations and aims to provide accurate and accessible information for all readers. We use clear language and avoid complex financial jargon to make the subject matter easy to grasp.

Key Takeaways:

- Definition of Interest: A comprehensive explanation of interest, its purpose, and how it functions within loan agreements.

- Interest Calculation Methods: A detailed analysis of different methods used to calculate interest on monthly payments, including simple interest and compound interest.

- Components of a Monthly Payment: A breakdown of the elements comprising a monthly payment, showing how much goes towards principal and how much towards interest.

- Amortization Schedules: An explanation of amortization schedules and how they provide a clear picture of interest and principal payments over the life of a loan.

- Factors Affecting Interest: An examination of how interest rates, loan terms, and payment frequency impact the total interest paid.

- Strategies for Minimizing Interest: Practical tips and strategies to reduce the total interest paid over the life of a loan.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding interest, let’s delve into the specifics of how it's calculated and applied to monthly payments.

Exploring the Key Aspects of Interest on Monthly Payments

1. Definition and Core Concepts:

Interest is the cost of borrowing money. Lenders charge interest as compensation for the risk they take in lending funds. The amount of interest charged depends on several factors, including the principal amount borrowed, the interest rate, and the loan term. Interest is usually expressed as an annual percentage rate (APR), but it's crucial to understand how this annual rate translates into monthly payments.

2. Interest Calculation Methods:

There are primarily two methods of calculating interest:

-

Simple Interest: This is the most straightforward method. It calculates interest only on the principal amount borrowed. The formula is: Interest = Principal x Rate x Time. Time is usually expressed in years, but for monthly payments, it would be expressed as a fraction of a year (e.g., 1/12 for one month). Simple interest is rarely used for loans with longer terms.

-

Compound Interest: This is the most common method used for loans and mortgages. It calculates interest not only on the principal but also on accumulated interest. This means that interest is added to the principal, and the next month's interest is calculated on the higher amount (principal + accumulated interest). This snowball effect leads to significantly higher interest payments over the life of a loan.

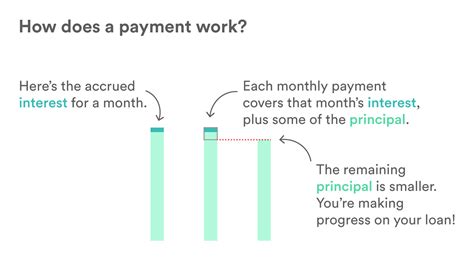

3. Components of a Monthly Payment:

Each monthly payment on a loan is divided into two parts:

-

Principal: The portion of the payment that goes towards reducing the original loan amount.

-

Interest: The portion of the payment that goes towards paying the lender for the cost of borrowing the money.

In the early stages of a loan, a larger portion of the payment goes towards interest, while as the loan nears its end, a larger portion goes towards the principal.

4. Amortization Schedules:

An amortization schedule is a detailed table that shows the breakdown of each monthly payment into principal and interest components over the life of a loan. It provides a clear picture of how your payments are allocated and how your loan balance decreases over time. You can easily find amortization calculators online to create one for your specific loan.

5. Factors Affecting Interest:

Several factors influence the total interest paid on a loan:

-

Interest Rate: A higher interest rate leads to higher monthly payments and significantly more interest paid over the loan's life.

-

Loan Term: A longer loan term means lower monthly payments, but it also results in paying more interest overall because interest accrues for a longer period.

-

Payment Frequency: Making more frequent payments (e.g., bi-weekly instead of monthly) can reduce the total interest paid because the principal balance decreases faster.

6. Impact on Innovation:

The way interest is calculated influences technological innovation in the finance sector. The need for accurate and efficient interest calculations has driven the development of sophisticated software and algorithms used in loan origination and management systems.

Exploring the Connection Between Amortization Schedules and Monthly Payments

Amortization schedules are directly related to how interest works on monthly payments. They provide a detailed breakdown of how each payment is allocated between principal and interest. By examining an amortization schedule, you can clearly see how the proportion of interest and principal changes over time.

Key Factors to Consider:

-

Roles and Real-World Examples: A mortgage is a prime example where amortization schedules are crucial. Borrowers can use these schedules to track their progress, plan for early payoff strategies, and understand the long-term financial implications of their loan.

-

Risks and Mitigations: Failure to understand amortization schedules can lead to unexpected expenses and difficulties in managing debt. Careful budgeting and financial planning, along with a thorough understanding of the loan terms, can mitigate these risks.

-

Impact and Implications: Amortization schedules have significant implications for long-term financial planning. By understanding them, individuals can make informed decisions about loan options and develop strategies to minimize debt.

Conclusion: Reinforcing the Connection

The close relationship between amortization schedules and monthly payments highlights the importance of understanding how interest is calculated. Amortization schedules provide the transparency needed to make responsible borrowing decisions.

Further Analysis: Examining Compound Interest in Greater Detail

Compound interest is the engine driving long-term debt growth. The earlier mentioned snowball effect, where interest accrues on accumulated interest, can dramatically increase the overall cost of borrowing. This is why it's essential to understand how compound interest works and to explore strategies to minimize its impact.

FAQ Section: Answering Common Questions About Interest on Monthly Payments

Q: What is the difference between APR and interest rate?

A: APR (Annual Percentage Rate) is the annual interest rate, including fees and other charges. The interest rate is the percentage charged on the principal amount. The APR is often higher than the quoted interest rate.

Q: How can I calculate my monthly payment?

A: You can use online loan calculators or financial formulas to calculate your monthly payment. These tools require the loan amount, interest rate, and loan term as inputs.

Q: How can I pay off my loan faster?

A: Making extra payments, even small ones, can significantly reduce the total interest paid and shorten the loan term. Refinancing to a lower interest rate can also save money.

Practical Tips: Maximizing the Benefits of Understanding Interest

-

Understand the Basics: Grasp the difference between simple and compound interest, and understand how each affects your monthly payments.

-

Compare Loan Offers: Don’t just look at the monthly payment. Analyze the total interest paid over the loan’s life.

-

Use Amortization Schedules: Monitor your progress, and plan your payments strategically.

-

Explore Refinancing Options: If interest rates fall, consider refinancing to a lower rate to save on interest.

-

Budget Wisely: Plan your budget to prioritize debt reduction and avoid accumulating more debt.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding how interest works on monthly payments is fundamental to responsible financial management. By mastering these concepts, you gain control over your finances, minimize unnecessary expenses, and make informed decisions to reach your financial goals efficiently. The knowledge presented here empowers you to navigate the complexities of borrowing and build a strong financial future.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On A 3000 Credit Card Chase

Apr 05, 2025

-

What Is The Minimum Payment On Chase Credit Card

Apr 05, 2025

-

Tjxrewards Com Credit Card Payments

Apr 05, 2025

-

Tjx Style Card Benefits

Apr 05, 2025

-

Tjx Rewards Annual Fee

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Does Interest Work On Monthly Payments . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.