How Does A Credit Card Grace Period Work

adminse

Apr 02, 2025 · 8 min read

Table of Contents

Decoding the Grace Period: How Credit Card Interest Works (and How to Avoid It)

What if understanding your credit card grace period could save you thousands of dollars over your lifetime? Mastering this crucial aspect of credit card management is the key to responsible borrowing and maximizing your financial health.

Editor’s Note: This article on credit card grace periods was published today, providing you with the most up-to-date information to help you manage your credit card accounts effectively.

Why Understanding Your Credit Card Grace Period Matters:

Credit cards offer convenience and financial flexibility, but understanding how they work, particularly the grace period, is critical to avoiding significant interest charges. A grace period is essentially a short window where you can pay your balance in full without incurring any interest. Knowing how this period functions, and the factors that can affect it, can mean the difference between paying only the amount you spent and paying considerably more in interest. This knowledge is relevant for everyone from students managing their first credit card to seasoned professionals looking to optimize their finances.

Overview: What This Article Covers:

This article delves deep into the intricacies of credit card grace periods. We will explore its definition, how it's calculated, factors that can impact it, strategies to maintain it, and what happens when you miss out. We'll also address common misconceptions and offer actionable tips for responsible credit card usage.

The Research and Effort Behind the Insights:

This comprehensive guide draws on extensive research, incorporating information from leading financial institutions, consumer protection agencies, and established financial literature. Every claim is supported by factual data and relevant examples to ensure accuracy and clarity.

Key Takeaways:

- Definition of Grace Period: A clear explanation of what constitutes a credit card grace period.

- Calculating Your Grace Period: A step-by-step guide to understanding how your grace period is determined.

- Factors Affecting Grace Period: An in-depth analysis of elements that can shorten or eliminate your grace period.

- Maintaining Your Grace Period: Practical strategies to ensure you consistently benefit from the grace period.

- Consequences of Missing the Grace Period: The financial implications of not paying your balance in full before the grace period ends.

- Common Misconceptions: Addressing frequently held but incorrect beliefs about grace periods.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding your grace period, let's explore its core aspects in detail.

Exploring the Key Aspects of Credit Card Grace Periods:

1. Definition and Core Concepts:

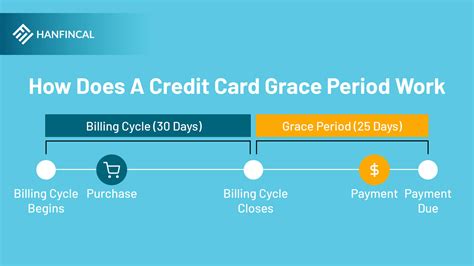

A grace period on a credit card is the time you have between the end of your billing cycle and the due date of your payment, during which you can pay your statement balance in full without incurring interest charges. It's essentially a free period offered by credit card companies, allowing you to use their credit without immediately paying interest. This benefit is contingent on paying your balance in full by the due date.

2. How the Grace Period is Calculated:

The calculation isn't universally standardized; it varies slightly between credit card issuers. However, the general principle remains the same:

- Billing Cycle: Your billing cycle starts on a specific date and ends on a specific date each month. This period tracks your purchases and other transactions.

- Statement Date: After your billing cycle ends, the credit card company generates a statement summarizing your transactions and the balance due.

- Due Date: The due date is typically 21-25 days after the statement date. This is the deadline for paying your balance to qualify for the grace period.

Example: If your billing cycle ends on the 15th of each month, and your statement is generated on the 17th, your due date might fall on the 11th of the following month (approximately 25 days later). The grace period is the time between the 17th and the 11th.

3. Factors that Can Affect Your Grace Period:

Several factors can significantly impact or even eliminate your grace period:

- Late Payments: A late payment on your previous statement almost always cancels the grace period on your next statement. Even if you pay your current balance in full after the due date, you'll be charged interest on the previous balance.

- Cash Advances: Cash advances are typically not subject to a grace period. Interest charges accrue immediately on cash advances.

- Balance Transfers: Interest on balance transfers generally starts accruing immediately. The grace period is usually not applicable to transferred balances.

- Promotional Offers: Some promotional offers, like 0% APR periods, may have specific rules regarding grace periods. Carefully review the terms and conditions of these offers.

- Specific Card Agreements: Always refer to your credit card agreement for the precise terms and conditions related to your grace period. These agreements may contain details not explicitly stated elsewhere.

4. Maintaining Your Grace Period:

The key to consistently enjoying the benefits of your grace period is simple:

- Pay Your Balance in Full: Always aim to pay your statement balance in full by the due date.

- Set Reminders: Use online banking, calendar alerts, or budgeting apps to set reminders for your payment due date.

- Automate Payments: Consider setting up automatic payments to ensure timely payments, minimizing the risk of missing deadlines.

- Monitor Your Account: Regularly review your credit card statement for accuracy and promptly address any discrepancies.

- Understand Your Billing Cycle: Become familiar with your specific billing cycle and due date to avoid surprises.

5. Consequences of Missing Your Grace Period:

Missing your grace period will have significant financial implications:

- Interest Charges: You'll be charged interest on your entire outstanding balance from the day the grace period expires.

- Higher Debt: The interest adds to your principal balance, increasing the overall amount you owe.

- Damage to Credit Score: Repeated late payments can negatively impact your credit score, making it more difficult to secure loans and other financial products in the future.

- Increased Minimum Payment: Your minimum payment amount may increase as a result of the accrued interest, making it harder to pay off your balance.

6. Common Misconceptions about Grace Periods:

- Myth: Paying a portion of your balance before the due date grants you a grace period. Reality: You must pay your statement balance in full to qualify for the grace period. Partial payments will not waive interest charges.

- Myth: The grace period applies to all credit card transactions. Reality: Cash advances and balance transfers typically don't have a grace period; interest accrues immediately.

- Myth: A grace period is guaranteed on all credit cards. Reality: Credit card companies can modify or eliminate the grace period under certain conditions (such as late payments).

Exploring the Connection Between Payment Habits and Grace Periods:

The relationship between responsible payment habits and the effective use of grace periods is undeniably crucial. Consistent, on-time payments are essential for maintaining the grace period. Poor payment habits—missing payments, paying late, or only making minimum payments—directly compromise the grace period and lead to increased interest charges.

Key Factors to Consider:

- Roles and Real-World Examples: A consumer who consistently pays their balance in full before the due date benefits significantly by avoiding interest charges. Conversely, someone who frequently makes late payments or only pays the minimum will incur substantial interest costs, losing the advantage of the grace period.

- Risks and Mitigations: The risk of losing the grace period is substantial. Mitigating this risk involves setting payment reminders, automating payments, and actively monitoring your account.

- Impact and Implications: The long-term impact of consistently using the grace period is substantial financial savings. Conversely, failing to leverage this benefit results in higher debt, negatively affecting overall financial health.

Conclusion: Reinforcing the Connection:

The connection between consistent on-time payments and the successful utilization of the grace period is paramount. By prioritizing responsible payment habits, consumers can maximize the financial benefits offered by credit cards, ultimately building a stronger financial future.

Further Analysis: Examining Payment Methods in Greater Detail:

Different payment methods can impact the timing and effectiveness of your payments. Electronic payments, such as online transfers or automatic payments, generally offer confirmation of receipt and ensure timely processing. Mail-in payments, on the other hand, rely on postal services and can be subject to delays, potentially jeopardizing your grace period.

FAQ Section: Answering Common Questions About Credit Card Grace Periods:

What is a credit card grace period? A grace period is the time you have after your billing cycle ends to pay your balance in full without incurring interest.

How long is a grace period? The length of the grace period varies but is typically 21-25 days after the statement date.

What happens if I miss my grace period? You will be charged interest on your outstanding balance from the day the grace period ends.

Can I lose my grace period? Yes, late payments, cash advances, and balance transfers can often cause you to lose your grace period.

How can I avoid losing my grace period? Pay your balance in full and on time, each and every month.

Practical Tips: Maximizing the Benefits of Your Credit Card Grace Period:

- Understand the Basics: Thoroughly read your credit card agreement to understand your specific grace period terms.

- Set Payment Reminders: Use calendar alerts, online banking features, or budgeting apps to ensure timely payments.

- Automate Payments: Consider setting up automatic payments to eliminate the risk of forgetting payment deadlines.

- Review Statements Regularly: Check your statements for accuracy and promptly address any discrepancies.

- Pay in Full, On Time: Always aim to pay your entire statement balance before the due date.

Final Conclusion: Wrapping Up with Lasting Insights:

Mastering the mechanics of your credit card grace period is a cornerstone of responsible credit card management. By understanding how it works, utilizing effective strategies, and avoiding common pitfalls, you can significantly reduce interest charges and enhance your overall financial well-being. The grace period is a valuable tool; use it wisely.

Latest Posts

Latest Posts

-

What Is Liquidity Pool In Blockchain

Apr 04, 2025

-

What Is A Liquidity Pool In Cryptocurrency

Apr 04, 2025

-

Quickbooks Late Fees

Apr 04, 2025

-

How To Set Up Automatic Late Fees In Quickbooks Desktop

Apr 04, 2025

-

How To Charge Late Fees In Quickbooks

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about How Does A Credit Card Grace Period Work . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.