How Credit Card Grace Period Works

adminse

Apr 02, 2025 · 8 min read

Table of Contents

Unlocking the Secrets of Your Credit Card Grace Period: A Comprehensive Guide

What if maximizing your credit card's grace period could significantly improve your financial health? Understanding this crucial aspect of credit card management is key to avoiding unnecessary interest charges and building a strong credit history.

Editor’s Note: This article on credit card grace periods was published today, providing you with the most up-to-date information to navigate the complexities of credit card billing cycles and interest calculations.

Why Understanding Your Grace Period Matters:

Understanding your credit card grace period is paramount for responsible credit card usage. It's the window of opportunity you have to pay your statement balance in full and avoid paying any interest charges. This seemingly small detail can dramatically impact your overall spending and borrowing costs over time. Ignoring it can lead to accumulating debt and paying far more than the initial purchase price. Effective grace period management is crucial for maintaining a healthy credit score and building financial stability.

Overview: What This Article Covers:

This article comprehensively explores the intricacies of credit card grace periods. We will define the concept, delve into the mechanics of billing cycles, explain how interest is calculated, address common misconceptions, and provide actionable strategies for maximizing your grace period benefits. We’ll also examine the nuances related to different types of credit cards and how various payment methods impact your grace period.

The Research and Effort Behind the Insights:

This article is the product of extensive research, drawing on information from reputable financial institutions, consumer protection agencies, and credit reporting bureaus. The information presented is based on widely accepted industry practices and is intended to provide clear and accurate guidance for consumers.

Key Takeaways:

- Definition of Grace Period: A clear definition and explanation of the credit card grace period.

- Billing Cycle Mechanics: Understanding how billing cycles influence grace periods.

- Interest Calculation: How interest accrues if the balance isn't paid in full during the grace period.

- Impact of Payment Methods: How different payment methods affect grace period utilization.

- Strategies for Maximizing Grace Period: Practical tips to optimize your grace period benefits.

- Grace Period and Different Credit Card Types: Specific considerations for various credit cards (e.g., rewards cards, balance transfer cards).

- Addressing Common Misconceptions: Clarifying common misunderstandings surrounding grace periods.

- Protecting Yourself from Unexpected Charges: Steps to prevent unintentional interest charges.

Smooth Transition to the Core Discussion:

With a foundational understanding of why comprehending your credit card grace period is essential, let's now delve into the specifics, demystifying this often-misunderstood aspect of credit card management.

Exploring the Key Aspects of Credit Card Grace Periods:

1. Definition and Core Concepts:

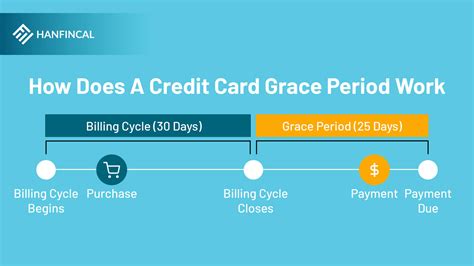

A credit card grace period is the time between the end of your billing cycle and the due date of your payment. During this period, you can pay your statement balance in full without incurring interest charges. The length of the grace period varies, typically ranging from 21 to 25 days, but it's always clearly specified on your credit card statement. It's crucial to understand that this grace period only applies to purchases made during the previous billing cycle, not to balances carried over from previous months (unless specifically stated otherwise by your card issuer).

2. Billing Cycle Mechanics:

The billing cycle is the period over which your credit card transactions are tallied to create your monthly statement. The statement reflects all purchases, payments, and fees incurred during that cycle. Once the billing cycle ends, the grace period begins, offering you the time to pay the statement balance before interest charges start to accrue. Understanding your billing cycle start and end dates is crucial for effective grace period management.

3. Interest Calculation:

If you don't pay your statement balance in full within the grace period, interest charges begin to accrue on the outstanding amount. The interest rate is your Annual Percentage Rate (APR), which is typically expressed as a percentage per year. This APR is divided by the number of days in a year to determine the daily interest rate. The daily interest rate is then multiplied by your outstanding balance and the number of days the balance remains unpaid to calculate the total interest. This is a compounding interest system, meaning interest is charged not only on the principal balance but also on accumulated interest.

4. Impact of Payment Methods:

The method you use to make your payment can indirectly affect your grace period. While the payment itself doesn't directly change the grace period length, late payments, even by a single day, can negate your grace period for the entire billing cycle. This means interest will accrue on the previous month's balance, even if you pay the current statement in full. Therefore, reliable and timely payment methods are essential.

5. Strategies for Maximizing Your Grace Period:

- Understand your billing cycle: Track your billing cycle start and end dates meticulously.

- Pay on time: Always aim to pay your statement balance in full before the due date. Automatic payments can help prevent late payments.

- Review your statement carefully: Check your statement for any errors or discrepancies.

- Set reminders: Use calendar reminders or automated payment systems to ensure timely payments.

- Pay online: Online payments often offer quicker processing times.

Closing Insights: Summarizing the Core Discussion:

Effectively utilizing your credit card's grace period is a fundamental aspect of responsible credit management. By understanding the billing cycle, interest calculation, and the consequences of late payments, you can significantly reduce the overall cost of using your credit card. The key takeaway is to consistently pay your statement balance in full before the due date to fully benefit from the grace period and avoid unnecessary interest charges.

Exploring the Connection Between Credit Score and Grace Period Utilization:

The relationship between your credit score and the effective use of your grace period is significant. Consistently paying your credit card balance in full within the grace period demonstrates responsible credit behavior, which positively impacts your credit score. Conversely, consistently carrying a balance and incurring interest charges can negatively affect your credit score. Late payments, which nullify the grace period, are particularly detrimental.

Key Factors to Consider:

- Roles and Real-World Examples: Individuals with excellent credit scores consistently utilize their grace periods, reflecting responsible credit behavior. Conversely, individuals with poor credit scores often struggle with timely payments, negating their grace periods and incurring substantial interest charges.

- Risks and Mitigations: The primary risk is incurring interest charges due to late or partial payments. Mitigation strategies include setting automatic payments, utilizing online banking, and setting reminders.

- Impact and Implications: Effective grace period utilization contributes to a higher credit score, leading to better loan terms, lower interest rates, and access to a wider range of financial products.

Conclusion: Reinforcing the Connection:

The link between grace period management and credit score is undeniable. By diligently paying your credit card balance in full before the due date, you demonstrate responsible financial behavior that contributes positively to your creditworthiness. Conversely, neglecting this crucial aspect of credit management can have long-term financial repercussions.

Further Analysis: Examining Late Payment Penalties in Greater Detail:

Late payment penalties are significant consequences of not meeting your credit card payment due date. These penalties vary among card issuers but generally include late fees and increased interest charges. Late fees can range from $25 to $40 or more, and these fees can compound over time if payments repeatedly fall behind. The late payment will also be reported to the credit bureaus, negatively impacting your credit score.

FAQ Section: Answering Common Questions About Credit Card Grace Periods:

Q: What happens if I make a partial payment during the grace period?

A: While a partial payment is better than no payment, it doesn't eliminate interest charges. Interest will still accrue on the outstanding balance.

Q: Does the grace period apply to cash advances?

A: No, the grace period generally does not apply to cash advances. Interest typically begins accruing immediately on cash advances.

Q: Can my grace period change?

A: While the standard grace period is generally consistent, it can be impacted by late payments or changes in your credit card agreement. Always review your statement for updated terms.

Q: What if my statement doesn't show a grace period?

A: Contact your card issuer immediately. The absence of a grace period is unusual and may indicate an error or a change in your agreement.

Practical Tips: Maximizing the Benefits of Your Credit Card Grace Period:

- Set up automatic payments: Automate your payments to ensure on-time payments.

- Use online banking: Online banking provides convenient payment options and detailed transaction tracking.

- Check your statement thoroughly: Verify the billing cycle dates and the due date to avoid any surprises.

- Utilize calendar reminders: Set reminders to pay your balance before the due date.

- Contact customer service if needed: Don't hesitate to contact your card issuer if you have any questions or concerns.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding and effectively utilizing your credit card grace period is a cornerstone of responsible credit card management. By consistently paying your balance in full before the due date, you avoid interest charges, protect your credit score, and ultimately save money. Make grace period management a priority to build a strong financial foundation.

Latest Posts

Latest Posts

-

What Is Liquidity In Crypto Coin

Apr 03, 2025

-

What Is Liquidity In Cryptocurrency In Urdu

Apr 03, 2025

-

What Is Liquidity In Crypto Reddit

Apr 03, 2025

-

What Is Liquidity In Crypto Exchange

Apr 03, 2025

-

What Is Liquidity In Crypto Market

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about How Credit Card Grace Period Works . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.