Credit Card Charges For Late Payment

adminse

Apr 03, 2025 · 7 min read

Table of Contents

Late Credit Card Payment Charges: Understanding the Fees and Protecting Your Finances

What if overlooking a credit card due date could significantly impact your financial well-being? Late payment fees on credit cards are a substantial cost to consumers, often leading to a cycle of debt and impacting credit scores.

Editor’s Note: This article on credit card late payment charges was published today and provides up-to-date information on fees, strategies for avoidance, and the impact on your credit.

Why Late Credit Card Payment Charges Matter:

Late payment fees on credit cards are a significant concern for millions. These charges can quickly escalate, transforming a minor oversight into a major financial burden. Understanding the mechanics of these fees, their impact on your credit score, and strategies for avoiding them is crucial for maintaining healthy personal finances. The implications extend beyond immediate costs; they can affect your ability to secure loans, rent an apartment, or even get certain jobs. This article serves as a comprehensive guide, empowering readers to navigate the complexities of credit card payments and protect their financial future.

Overview: What This Article Covers:

This article provides a detailed exploration of late credit card payment charges. We'll examine the various types of fees, the factors influencing their amount, the legal framework surrounding them, and the long-term consequences of late payments. We will also offer practical strategies for avoiding late fees and managing credit responsibly. Finally, we'll delve into frequently asked questions and provide actionable tips for maintaining good credit.

The Research and Effort Behind the Insights:

This article is based on extensive research, incorporating information from the Consumer Financial Protection Bureau (CFPB), the Fair Credit Reporting Act (FCRA), numerous credit card issuer websites, and financial literacy resources. Data on average late fees and their impact on credit scores is sourced from reputable financial institutions and consumer credit reporting agencies. The analysis strives to provide accurate, unbiased information to guide readers toward informed financial decisions.

Key Takeaways:

- Definition and Core Concepts: A clear understanding of what constitutes a late payment and the different types of associated fees.

- Practical Applications: Strategies for avoiding late payments and managing credit effectively.

- Challenges and Solutions: Identifying common obstacles leading to late payments and solutions to overcome them.

- Future Implications: The long-term effects of late payments on credit scores and financial health.

Smooth Transition to the Core Discussion:

With a foundational understanding of the importance of timely credit card payments, let’s delve into the specifics of late payment charges and their ramifications.

Exploring the Key Aspects of Late Credit Card Payment Charges:

1. Definition and Core Concepts:

A late payment occurs when a credit card minimum payment isn't received by the issuer by the due date stated on your billing statement. This date is typically 21 to 25 days after the closing date of your billing cycle. The grace period, the time between the closing date and the due date, allows you to pay your balance in full without incurring interest charges. However, even paying a portion of your balance after the due date can trigger a late payment fee. This fee is separate from any interest charges accrued on the outstanding balance.

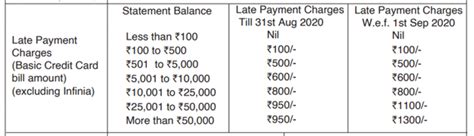

2. Types of Late Payment Fees:

Credit card issuers generally charge one or more of the following fees for late payments:

- Late Payment Fee: This is the most common fee, typically ranging from $25 to $39, but can be significantly higher depending on the issuer and your credit history.

- Returned Payment Fee: If your payment is returned due to insufficient funds or incorrect account information, you'll face an additional fee, often between $25 and $35.

- Over-the-Limit Fee: If your purchases exceed your credit limit, you might incur a fee, adding to the financial strain.

3. Factors Influencing Late Payment Fee Amounts:

Several factors determine the exact amount of your late payment fee:

- Credit Card Issuer: Different credit card companies have varying fee structures. Some premium cards might have higher fees than basic cards.

- Your Credit History: Issuers may charge higher fees to cardholders with a history of late payments, reflecting a higher perceived risk.

- Your Credit Card Agreement: The specifics of your late payment fee are outlined in your credit card agreement. Review this document carefully to understand your obligations.

4. Impact on Credit Score:

A late payment significantly impacts your credit score. This negative mark remains on your credit report for seven years. Multiple late payments further damage your creditworthiness, making it difficult to obtain loans, mortgages, or even rent an apartment in the future. The severity of the impact depends on factors like the number of late payments and your overall credit history. A single late payment can lower your score by 30 to 100 points.

5. Legal Framework and Consumer Protection:

The Truth in Lending Act (TILA) and the Fair Credit Reporting Act (FCRA) offer some protection to consumers. TILA mandates that credit card issuers clearly disclose all fees, including late payment charges, in your credit card agreement. The FCRA ensures accuracy and fairness in reporting credit information. However, it doesn't prevent late payment fees from being assessed.

Exploring the Connection Between Grace Periods and Late Payment Charges:

The grace period plays a critical role in avoiding late payment charges. Understanding its mechanics is crucial. The grace period is the time between the closing date of your billing cycle and the due date. It allows you to pay your balance in full and avoid interest charges. However, even if you make a partial payment during the grace period, it will not prevent a late payment fee if the full payment isn't received by the due date.

Key Factors to Consider:

- Roles and Real-World Examples: Many people unintentionally miss payment due dates due to busy schedules, overlooked bills, or unexpected financial setbacks. This underscores the need for proactive payment management strategies.

- Risks and Mitigations: Failing to understand your due date or relying solely on memory can lead to costly late fees. Setting up automatic payments or reminders is a crucial mitigation strategy.

- Impact and Implications: Repeated late payments severely damage your credit score, hindering your ability to access credit and potentially affecting your insurance rates and employment opportunities.

Conclusion: Reinforcing the Connection:

The connection between understanding grace periods and diligently managing payments is undeniable. Failing to pay on time, even by a single day, can lead to significant financial repercussions. Proactive planning is vital in preventing late payments and safeguarding your financial future.

Further Analysis: Examining Automated Payment Systems in Greater Detail:

Automating credit card payments significantly reduces the risk of late payments. Several methods exist:

- Automatic Payments from Checking Account: This allows your credit card issuer to automatically debit your checking account each month.

- Scheduled Online Payments: You can set up online payments to automatically debit from your account on a specific date.

- Bill Payment Services: Third-party bill payment services can manage all your bills, including credit card payments.

FAQ Section: Answering Common Questions About Late Credit Card Payment Charges:

- What is considered a late payment? A payment received after the due date stated on your credit card statement.

- How much can a late payment fee be? Fees vary widely, typically ranging from $25 to $39, but can be much higher.

- Will a late payment affect my credit score? Yes, significantly. It can lower your score by 30-100 points or more.

- Can I negotiate a late payment fee? It's possible but not guaranteed. Contact your issuer promptly and explain your situation.

- What if I consistently make late payments? Your credit score will be severely damaged, potentially making it harder to get loans or rent.

Practical Tips: Maximizing the Benefits of Timely Payments:

- Set Reminders: Use calendar reminders, phone apps, or online banking features to set payment reminders.

- Automate Payments: Set up automatic payments to ensure timely payments each month.

- Review Your Statement Carefully: Note the due date on your statement and mark it on your calendar.

- Track Your Spending: Regularly monitor your spending to avoid exceeding your credit limit.

- Communicate with Your Issuer: If you anticipate difficulty making a payment, contact your issuer immediately to discuss options.

Final Conclusion: Wrapping Up with Lasting Insights:

Late credit card payment charges are a costly mistake that can have long-lasting financial implications. By understanding the fees, their impact on credit scores, and implementing effective payment strategies, you can protect your financial health and avoid the significant financial burden of late payments. Proactive planning and responsible credit management are essential for maintaining a strong financial standing. Avoiding late fees is not just about saving money; it’s about building a strong financial foundation for the future.

Latest Posts

Latest Posts

-

What Is Liquidity Pool In Blockchain

Apr 04, 2025

-

What Is A Liquidity Pool In Cryptocurrency

Apr 04, 2025

-

Quickbooks Late Fees

Apr 04, 2025

-

How To Set Up Automatic Late Fees In Quickbooks Desktop

Apr 04, 2025

-

How To Charge Late Fees In Quickbooks

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Credit Card Charges For Late Payment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.