Zero Swap Rate

adminse

Apr 02, 2025 · 9 min read

Table of Contents

Decoding the Zero Swap Rate: A Deep Dive into Interest Rate Dynamics

What if the future of interest rate forecasting hinges on a complete understanding of the zero swap rate? This fundamental concept underpins complex financial instruments and offers crucial insights into market expectations and economic health.

Editor’s Note: This article on zero swap rates provides a comprehensive overview of this critical interest rate metric, updated with the latest insights and market trends. It’s designed for financial professionals, students, and anyone interested in gaining a deeper understanding of interest rate dynamics.

Why Zero Swap Rates Matter: Relevance, Practical Applications, and Industry Significance

Zero swap rates, also known as zero-coupon swap rates or simply zero rates, are fundamental building blocks in the fixed-income market. They represent the theoretical interest rate at which an investor would lend or borrow money for a specific period, with no intermediate payments (hence "zero-coupon"). Unlike yields on coupon-bearing bonds, zero rates isolate the pure time value of money for each maturity, providing a clearer picture of the market’s expectations regarding future interest rates. They are crucial for pricing a wide range of interest rate derivatives, including swaps, caps, floors, and other complex structured products. Their accurate calculation and interpretation are essential for risk management, portfolio construction, and investment strategy across various sectors, from banking and insurance to asset management.

Overview: What This Article Covers

This article will delve into the intricacies of zero swap rates, providing a clear understanding of their definition, calculation methods, applications, and relationship with other interest rate benchmarks. We will explore the factors influencing zero swap rate curves, their role in risk management, and their implications for economic forecasting. Furthermore, we'll examine the connection between zero swap rates and other key financial concepts, specifically focusing on the yield curve.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon established financial literature, market data from reputable sources, and practical experience in fixed-income markets. The analysis presented is supported by established methodologies and aims to provide readers with accurate and reliable information.

Key Takeaways:

- Definition and Core Concepts: A precise explanation of zero swap rates and their underlying principles.

- Calculation Methods: Detailed exploration of bootstrapping and other techniques used to derive zero rates from market data.

- Applications in Finance: Illustrative examples of how zero rates are used in pricing and hedging interest rate derivatives.

- Relationship with the Yield Curve: Analysis of the connection between zero rates and the shape and dynamics of the yield curve.

- Economic Significance and Forecasting: Understanding the implications of zero rate curves for economic outlook and monetary policy.

- Risks and Challenges: Discussion of potential pitfalls and considerations in using zero rates.

Smooth Transition to the Core Discussion:

Having established the significance of zero swap rates, let's now delve into their core aspects and explore their practical applications within the financial landscape.

Exploring the Key Aspects of Zero Swap Rates

1. Definition and Core Concepts:

A zero swap rate is the implied forward interest rate for a particular maturity derived from the market prices of interest rate swaps. An interest rate swap involves exchanging fixed-rate payments for floating-rate payments over a specified period. By analyzing the market prices of these swaps, financial institutions and analysts can extract a series of zero rates, creating a zero rate curve that represents the market's expectations of future interest rates at different maturities. It's important to note that these rates are "theoretical" because they represent the interest rate on a hypothetical zero-coupon instrument.

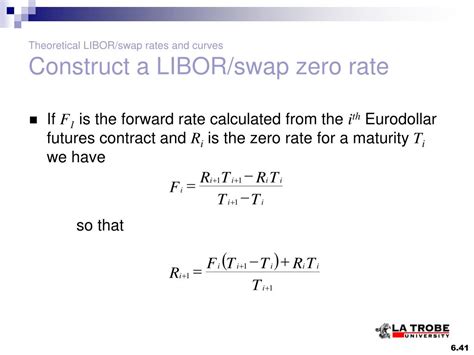

2. Calculation Methods: Bootstrapping the Zero Rate Curve

The most common method for calculating zero swap rates is bootstrapping. This iterative process uses observed market prices of interest rate swaps to derive the corresponding zero rates. It starts with the shortest maturity swap and works its way up the curve, using the previously calculated zero rates to determine the next one. The process requires solving a series of equations, often involving numerical methods. For example:

- Step 1: The shortest-maturity swap (e.g., a 1-year swap) directly provides the 1-year zero rate.

- Step 2: Using the 1-year zero rate and the market price of a 2-year swap, the 2-year zero rate is calculated.

- Step 3: This process is repeated for longer maturities, always using previously calculated zero rates and the observed prices of longer-term swaps.

Other methods, such as those employing interpolation techniques, might be used to smooth the curve and fill in gaps in market data.

3. Applications Across Industries:

Zero swap rates are vital for a multitude of financial applications:

-

Pricing Interest Rate Derivatives: They are fundamental inputs in pricing various interest rate derivatives, ensuring accurate valuation and risk management. For example, the price of a bond futures contract, interest rate swaps, or other derivatives hinges directly on the implied forward rates from zero rate curves.

-

Portfolio Management: Asset managers use zero curves to evaluate the performance and risk of their bond portfolios, enabling informed decisions regarding asset allocation and hedging strategies.

-

Risk Management: Banks and financial institutions use zero rates for stress testing, assessing potential losses under various interest rate scenarios. This is crucial for maintaining capital adequacy and mitigating financial risks.

-

Economic Forecasting: The shape and slope of the zero rate curve provide valuable insights into market sentiment and future economic prospects. An upward-sloping curve typically indicates expectations of future interest rate hikes, while a downward-sloping curve (inverted yield curve) can signal potential economic slowdown or recession.

4. Impact on Innovation:

The development of sophisticated models and techniques for calculating and analyzing zero swap rates has led to the creation of increasingly complex and innovative financial instruments. This constant evolution enhances market efficiency and provides more nuanced risk management tools.

Closing Insights: Summarizing the Core Discussion

Zero swap rates are not merely theoretical constructs; they represent a critical link between market observables and future interest rate expectations. Their accurate calculation and interpretation are paramount for a wide range of financial activities, from pricing complex derivatives to assessing economic risk.

Exploring the Connection Between the Yield Curve and Zero Swap Rates

The yield curve, a graphical representation of bond yields across different maturities, is intrinsically linked to zero swap rates. While the yield curve displays yields on coupon-bearing bonds, zero rates provide a clearer picture of the pure term structure of interest rates, free from the influence of coupon payments. The zero rate curve is often derived from the yield curve using bootstrapping techniques. Therefore, understanding the relationship between the two is crucial for a comprehensive understanding of interest rate dynamics.

Key Factors to Consider:

-

Roles and Real-World Examples: The yield curve serves as a source for extracting zero rates, while zero rates refine the understanding of the implied forward rates embedded within the yield curve. For instance, an upward-sloping yield curve may imply higher future short-term rates, which can be confirmed or refined using the zero rate curve.

-

Risks and Mitigations: Inaccuracies in the yield curve data used for bootstrapping can lead to inaccuracies in the derived zero rate curve. Robust data sources and careful attention to methodology are crucial to mitigate these risks.

-

Impact and Implications: The shape of the zero rate curve, just like the yield curve, reflects market expectations of future interest rates and can be used as an indicator of economic conditions. For example, a steep upward-sloping zero rate curve suggests strong economic growth expectations, whereas an inverted curve could indicate an impending recession.

Conclusion: Reinforcing the Connection

The yield curve and zero swap rates are interconnected facets of the interest rate market. The yield curve provides the raw data, while the zero rate curve offers a more refined and accurate representation of the term structure of interest rates. By using both, analysts can gain a richer understanding of market dynamics and make better-informed financial decisions.

Further Analysis: Examining Bootstrapping in Greater Detail

Bootstrapping, the cornerstone of zero rate curve construction, requires careful consideration of various factors. The accuracy of the bootstrapped curve heavily relies on the quality and completeness of the underlying swap data. Market imperfections, such as liquidity differences across different maturities, can introduce biases into the calculated zero rates. Furthermore, interpolation techniques used to fill gaps in the data can significantly impact the shape and smoothness of the resulting curve. Advanced techniques might incorporate stochastic models to account for the uncertainty and volatility inherent in interest rate markets.

FAQ Section: Answering Common Questions About Zero Swap Rates

-

What is a zero swap rate? A zero swap rate is the theoretical interest rate on a hypothetical zero-coupon bond with a specific maturity, derived from the market prices of interest rate swaps.

-

How are zero swap rates used in pricing derivatives? Zero swap rates provide the implied forward rates necessary for accurately valuing a wide range of interest rate derivatives, including swaps, caps, floors, and bond options.

-

What are the limitations of using zero swap rates? The accuracy of zero swap rates depends on the quality of market data and the chosen methodology. Market imperfections and model assumptions can introduce inaccuracies.

-

How are zero swap rates related to the yield curve? Zero swap rates are derived from the yield curve using bootstrapping techniques, offering a refined picture of the term structure of interest rates, free from the effects of coupon payments.

Practical Tips: Maximizing the Benefits of Understanding Zero Swap Rates

-

Understand the Basics: Begin by grasping the fundamental concepts of zero swap rates and their role in interest rate markets.

-

Learn Bootstrapping: Familiarize yourself with the bootstrapping methodology and the underlying principles involved in deriving zero rates from swap data.

-

Utilize Financial Software: Employ specialized financial software packages that provide tools for calculating and analyzing zero rate curves.

-

Stay Updated: Keep abreast of market developments and changes in methodology that could impact the accuracy and interpretation of zero swap rates.

Final Conclusion: Wrapping Up with Lasting Insights

Zero swap rates are a cornerstone of fixed-income markets, providing critical insights into interest rate dynamics and facilitating accurate pricing and risk management of interest rate derivatives. By understanding their calculation, applications, and limitations, financial professionals can enhance their decision-making and gain a competitive advantage in today's complex financial landscape. The continuous evolution of models and techniques for deriving and utilizing zero swap rates highlights their enduring significance in the world of finance.

Latest Posts

Latest Posts

-

Why Is Td Bank Charging Me A Maintenance Fee

Apr 03, 2025

-

What Fees Are Charged If You Are Late On A Payment

Apr 03, 2025

-

When Will I Be Charged

Apr 03, 2025

-

When To Charge A Late Fee

Apr 03, 2025

-

How To Assess Late Fees In Quickbooks Online

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about Zero Swap Rate . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.