Wm/reuters Benchmark Rates

adminse

Apr 01, 2025 · 7 min read

Table of Contents

Decoding the WM/Reuters Benchmark Rates: A Deep Dive into Global Financial Benchmarks

What if the stability of global financial markets hinges on the accuracy and integrity of benchmark interest rates? The WM/Reuters benchmark rates, once considered the gold standard, now stand under intense scrutiny, highlighting the critical role these seemingly obscure numbers play in our financial world.

Editor’s Note: This article on WM/Reuters benchmark rates provides a comprehensive overview of their history, methodology, significance, and the controversies that have shaped their future. It offers insights into the evolving landscape of financial benchmarks and the ongoing efforts to enhance their integrity.

Why WM/Reuters Benchmark Rates Matter: Relevance, Practical Applications, and Industry Significance

WM/Reuters benchmark rates, historically known as the London Interbank Offered Rate (LIBOR) submissions from Reuters and the Wholesale Money Market (WM) Company, served as the foundation for a vast array of financial instruments. Trillions of dollars worth of loans, derivatives, and other financial contracts were pegged to these rates, influencing everything from mortgages and credit card interest rates to complex financial derivatives. Their influence extended globally, impacting businesses, individuals, and governments alike. The integrity of these rates was, therefore, paramount to the stability and fairness of global financial markets. Any manipulation or inaccuracy directly impacted the pricing of financial products and potentially led to unfair gains or losses for market participants.

Overview: What This Article Covers

This article will explore the historical context of WM/Reuters benchmark rates, primarily focusing on the LIBOR scandal and its aftermath. It will delve into the methodology of rate submissions, the controversies surrounding manipulation, and the ongoing transition to alternative reference rates (ARRs). We will also examine the regulatory response, the implications for financial institutions, and the future of benchmark interest rates.

The Research and Effort Behind the Insights

This article draws upon extensive research, including regulatory reports from bodies like the Financial Conduct Authority (FCA), academic papers analyzing the LIBOR scandal, and news articles covering the transition to ARRs. The analysis presented aims to provide a balanced and factual account of this complex topic, supported by credible sources and expert commentary.

Key Takeaways:

- Definition and Core Concepts: Understanding the historical role of LIBOR and the WM/Reuters contribution to its calculation.

- Practical Applications: Exploring the widespread use of LIBOR-based financial instruments.

- Challenges and Solutions: Analyzing the LIBOR scandal, its causes, and the regulatory response.

- Future Implications: Examining the transition to ARRs and the implications for the financial industry.

Smooth Transition to the Core Discussion

Having established the significance of WM/Reuters benchmark rates, let's now delve into the intricacies of their history, methodology, and the challenges that led to their eventual demise as the primary global benchmark.

Exploring the Key Aspects of WM/Reuters Benchmark Rates (primarily LIBOR)

Definition and Core Concepts:

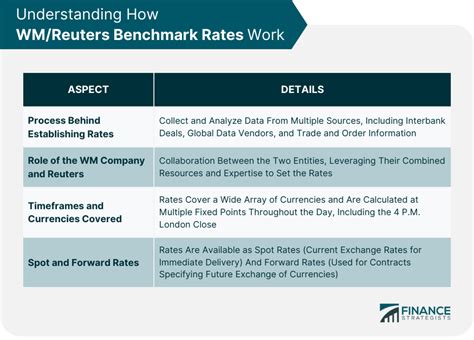

The WM/Reuters benchmark rates, primarily centered around LIBOR, were designed to represent the average rate at which banks could borrow unsecured funds from one another in the interbank market. The daily LIBOR rates were calculated for various currencies and maturities (overnight to 12 months), reflecting the prevailing borrowing costs in the London interbank market. The WM Company and Reuters played a crucial role in collecting submissions from a panel of contributing banks. These submissions, supposedly representing the banks' borrowing costs, were then used to calculate the final LIBOR rate after discarding the highest and lowest quartiles.

Applications Across Industries:

LIBOR’s ubiquity was staggering. It underpinned:

- Loans: Mortgages, corporate loans, and consumer credit products often referenced LIBOR as the basis for calculating interest rates.

- Derivatives: A vast array of interest rate derivatives, including swaps, futures, and options, were priced relative to LIBOR.

- Bonds: Some bonds incorporated LIBOR into their coupon payments or pricing mechanisms.

- Securities Lending: The cost of borrowing securities could be tied to LIBOR.

Challenges and Solutions: The LIBOR Scandal and its Aftermath

The LIBOR scandal, which came to light in the late 2000s and early 2010s, exposed significant flaws in the methodology and integrity of LIBOR submissions. Investigations revealed that some banks had manipulated their submissions to benefit their trading positions or to present a more favorable image of their financial health. This manipulation undermined the very foundation of LIBOR, casting doubt on its accuracy and reliability.

The response to the scandal involved extensive regulatory scrutiny, hefty fines for participating banks, and ultimately, a concerted effort to transition away from LIBOR. Key regulatory bodies, including the FCA and the US Federal Reserve, actively pushed for the adoption of alternative reference rates (ARRs).

Impact on Innovation: The Rise of Alternative Reference Rates (ARRs)

The LIBOR scandal served as a catalyst for innovation in the world of benchmark interest rates. The focus shifted towards developing more robust, transparent, and reliable benchmarks based on actual transactions rather than expert judgment or potentially manipulated submissions.

Several ARRs emerged, including:

- SOFR (Secured Overnight Financing Rate): A US-dollar benchmark based on the rates of repurchase agreements (repos) in the US Treasury market.

- SONIA (Sterling Overnight Index Average): A UK sterling benchmark based on overnight unsecured lending rates.

- ESTR (Euro Short-Term Rate): A euro benchmark based on overnight transactions in the euro money market.

These ARRs are generally considered more robust because they are based on actual transactions, offering greater transparency and reducing the potential for manipulation. However, the transition to these ARRs has not been without its complexities.

Exploring the Connection Between Regulatory Scrutiny and WM/Reuters Benchmark Rates

The relationship between regulatory scrutiny and WM/Reuters benchmark rates (specifically LIBOR) is undeniable. The lack of robust oversight and the inherent flaws in the LIBOR submission process allowed for manipulation to occur. The subsequent regulatory crackdown, including investigations, fines, and the push for ARRs, directly resulted from the failures exposed by the scandal.

Key Factors to Consider:

- Roles and Real-World Examples: The FCA’s investigation and subsequent penalties imposed on banks highlight the critical role of regulatory oversight in maintaining the integrity of benchmark rates. The LIBOR scandal itself serves as a stark real-world example of what can happen when such oversight is lacking.

- Risks and Mitigations: The reliance on self-reported data, as was the case with LIBOR, presents inherent risks. Mitigations include increased regulatory oversight, transparent methodologies, and the use of transaction-based benchmarks like ARRs.

- Impact and Implications: The LIBOR scandal eroded trust in financial markets and highlighted the systemic risk associated with flawed benchmarks. The transition to ARRs represents a significant step towards mitigating these risks.

Conclusion: Reinforcing the Connection

The regulatory response to the LIBOR scandal underscores the critical link between effective oversight and the integrity of benchmark interest rates. The lack of sufficient regulatory scrutiny allowed for manipulation, ultimately damaging the stability of global financial markets. The transition to ARRs, while complex, represents a vital step towards creating a more robust and transparent system.

Further Analysis: Examining Regulatory Reforms in Greater Detail

Regulatory reforms post-LIBOR scandal included stricter guidelines on benchmark rate submissions, increased penalties for manipulation, and a greater emphasis on transaction-based benchmarks. These reforms are designed to improve transparency, reduce the potential for manipulation, and enhance the overall integrity of financial benchmarks.

FAQ Section: Answering Common Questions About WM/Reuters Benchmark Rates

Q: What is the difference between LIBOR and the ARRs?

A: LIBOR was based on estimates of interbank borrowing costs, susceptible to manipulation. ARRs are based on actual transactions, making them more robust and transparent.

Q: Why was the transition from LIBOR to ARRs so complex?

A: The transition involved rewriting countless contracts, updating systems, and educating market participants. The sheer scale and interconnectedness of LIBOR-based instruments made the switch a significant undertaking.

Q: Are the ARRs completely immune to manipulation?

A: While ARRs are significantly more robust than LIBOR, no system is completely immune to manipulation. Continued vigilance and regulatory oversight are essential.

Practical Tips: Maximizing the Benefits of the Transition to ARRs

- Understand the specifics of the relevant ARRs: Familiarize yourself with the methodology and characteristics of the ARRs applicable to your specific financial instruments.

- Update contracts and systems: Ensure all contracts and systems are updated to reflect the use of ARRs.

- Stay informed about regulatory changes: Keep abreast of regulatory developments related to benchmark rates.

Final Conclusion: Wrapping Up with Lasting Insights

The saga of WM/Reuters benchmark rates, particularly the LIBOR scandal, serves as a cautionary tale about the importance of integrity and transparency in financial markets. The transition to ARRs is a crucial step towards building a more robust and resilient financial system. The lessons learned from the LIBOR scandal highlight the critical need for effective regulation, transparent methodologies, and a constant commitment to maintaining the trust and integrity of global financial benchmarks. The future of financial markets depends on it.

Latest Posts

Latest Posts

-

How To Lower Minimum Payment On Credit Card

Apr 04, 2025

-

What Is Minimum Payment Credit Card Rbc

Apr 04, 2025

-

What Is Minimum Payment For 10000 Credit Card

Apr 04, 2025

-

What Is The Minimum Payment For A Visa Credit Card

Apr 04, 2025

-

What Is The Minimum Payment For A 1000 Credit Card

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Wm/reuters Benchmark Rates . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.