Why Is It A Bad Idea To Only Pay Your Minimum Monthly Payment

adminse

Apr 05, 2025 · 7 min read

Table of Contents

The High Cost of Minimum Payments: Why Paying Only the Minimum is a Financial Disaster

Why settle for a slow, agonizing crawl towards debt freedom when you could sprint towards financial independence? Paying only the minimum on your credit cards and loans is a recipe for financial ruin, trapping you in a cycle of debt and hindering your long-term financial goals.

Editor’s Note: This article provides a comprehensive analysis of the dangers of only making minimum payments on debt. We'll explore the underlying math, the psychological impact, and practical strategies for escaping the minimum payment trap. This information is current as of October 26, 2023.

Why Paying Only the Minimum Matters: Relevance, Practical Applications, and Industry Significance

The seemingly innocuous act of paying only the minimum payment on your credit cards and loans carries significant consequences. It's a pervasive problem, impacting millions and contributing significantly to the national debt burden. Understanding the true cost of this practice is crucial for achieving financial stability and building wealth. This article will demonstrate how minimum payments lead to exponentially higher total interest paid, extended repayment periods, and ultimately, a severely hampered ability to achieve financial goals like homeownership, retirement savings, and emergency fund creation.

Overview: What This Article Covers

This article will delve into the intricate workings of minimum payments, unveiling the hidden costs and illustrating their long-term detrimental effects. We'll cover the mathematical realities of compound interest, the psychological aspects of debt, and offer practical strategies for escaping the minimum payment trap and building a healthier financial future. Readers will gain actionable insights into managing debt effectively, budgeting strategically, and building a strong financial foundation.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon data from reputable financial institutions, consumer protection agencies, and academic studies on consumer debt. We've analyzed various repayment scenarios to demonstrate the stark differences between minimum payment strategies and more aggressive repayment approaches. The information presented is intended to be objective, informative, and empower readers to make informed decisions about their personal finances.

Key Takeaways:

- The Power of Compound Interest: Understanding how compound interest works and its impact on minimum payment strategies.

- Hidden Costs Revealed: Quantifying the extra interest paid and the extended repayment timelines associated with minimum payments.

- Psychological Impact of Debt: Addressing the emotional toll of prolonged debt and its effect on financial well-being.

- Strategic Repayment Plans: Exploring various debt repayment strategies, such as the debt snowball and debt avalanche methods.

- Budgeting and Financial Planning: Developing effective budgeting techniques to allocate funds for debt repayment and other financial goals.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding minimum payments, let's dissect the mechanics and consequences of this common financial practice.

Exploring the Key Aspects of Minimum Payments

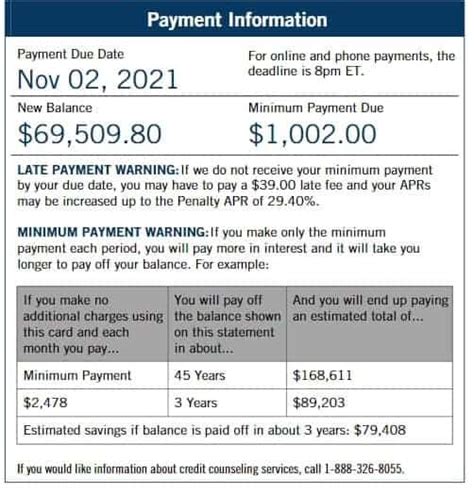

1. Definition and Core Concepts: The minimum payment is the smallest amount a borrower is required to pay on a credit card or loan each month to avoid late fees and maintain their account in good standing. However, this payment typically covers only a small portion of the principal balance, with the remaining amount accruing interest.

2. Applications Across Industries: Minimum payments are standard practice across various lending institutions, including credit card companies, banks, and mortgage lenders. The calculation of the minimum payment varies depending on the type of debt, but generally includes a portion of the interest accrued and a small percentage of the principal.

3. Challenges and Solutions: The primary challenge with minimum payments is the slow pace of debt reduction and the significant accumulation of interest over time. Solutions involve creating a budget, prioritizing debt repayment, and exploring different repayment strategies.

4. Impact on Innovation: Ironically, the prevalence of minimum payments has inadvertently fueled innovation in the personal finance sector, leading to the development of various debt management tools, apps, and financial counseling services aimed at helping consumers break free from the cycle of debt.

Closing Insights: Summarizing the Core Discussion

Paying only the minimum payment prolongs the debt repayment process, significantly increasing the total interest paid and delaying financial freedom. This practice creates a vicious cycle, making it difficult to save, invest, and achieve long-term financial goals.

Exploring the Connection Between Compound Interest and Minimum Payments

The relationship between compound interest and minimum payments is the crux of the problem. Compound interest is the interest calculated on both the principal amount and accumulated interest. When only minimum payments are made, a larger portion of the monthly payment goes towards interest, leaving a smaller amount to reduce the principal. This means that interest is constantly accumulating on a larger outstanding balance, leading to a snowball effect that dramatically increases the overall cost of borrowing.

Key Factors to Consider:

Roles and Real-World Examples: Consider a credit card with a $5,000 balance and a 18% APR. Making only the minimum payment (often around 2% of the balance) will result in paying significantly more in interest over time compared to making larger payments. The longer it takes to repay the debt, the more interest you will pay.

Risks and Mitigations: The primary risk is the potential for the debt to grow exponentially, leading to financial distress. Mitigation strategies involve creating a budget, increasing monthly payments, and considering debt consolidation or balance transfer options.

Impact and Implications: The long-term implications include delayed financial goals, reduced credit score, and increased financial stress. It can severely hinder your ability to save for retirement, buy a home, or handle unexpected expenses.

Conclusion: Reinforcing the Connection

The connection between compound interest and minimum payments is undeniable. Compound interest works against borrowers who make only minimum payments, resulting in a protracted repayment period and significantly increased total interest expense. Understanding this dynamic is paramount for effective debt management.

Further Analysis: Examining Compound Interest in Greater Detail

Compound interest, while beneficial for savers, acts as a formidable opponent when dealing with debt. The frequency of compounding (daily, monthly, annually) influences the total interest paid. The higher the interest rate, the more pronounced the effect of compound interest. It’s a crucial concept that every borrower must grasp to make informed financial decisions.

FAQ Section: Answering Common Questions About Minimum Payments

Q: What is the typical minimum payment percentage on a credit card?

A: It usually ranges from 1% to 2% of the outstanding balance, but can vary based on the issuer.

Q: Can I ever pay off my debt if I only make minimum payments?

A: Technically, yes, but it will take an extremely long time, and the total interest paid will be significantly higher than if larger payments were made.

Q: What happens if I miss a minimum payment?

A: You’ll likely incur late fees, and your credit score will suffer. Your interest rate might even increase.

Q: What are some alternatives to minimum payments?

A: Debt consolidation, balance transfers, and debt management plans can be helpful alternatives.

Practical Tips: Maximizing the Benefits of Aggressive Debt Repayment

-

Create a Realistic Budget: Track your income and expenses to identify areas where you can cut back to allocate more funds towards debt repayment.

-

Prioritize Debt Repayment: Develop a plan to tackle your debts strategically, considering methods like the debt snowball or debt avalanche approaches.

-

Increase Your Monthly Payments: Even small increases in your monthly payments can significantly shorten your repayment timeline and reduce the total interest paid.

-

Explore Debt Consolidation or Balance Transfers: Consolidating high-interest debt into a lower-interest loan or transferring balances to a card with a promotional 0% APR can save you money.

-

Seek Professional Help: If you're struggling to manage your debt, consider seeking guidance from a credit counselor or financial advisor.

Final Conclusion: Wrapping Up with Lasting Insights

Paying only the minimum payment on your debts is a financially imprudent strategy that leads to a prolonged debt cycle, higher interest payments, and diminished financial well-being. By understanding the impact of compound interest and adopting proactive debt management strategies, you can escape the minimum payment trap, achieve financial freedom, and build a brighter financial future. Taking control of your debt is not just about numbers; it’s about securing your financial future and creating peace of mind.

Latest Posts

Latest Posts

-

What Is The Minimum Monthly Payment For American Express

Apr 06, 2025

-

What Is The Minimum Payment On An American Express Card

Apr 06, 2025

-

What Is The Minimum Payment On American Express Gold Card

Apr 06, 2025

-

Why Do Capital One Payments Take So Long

Apr 06, 2025

-

How Long Does Capital One Take To Process A Payment

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Why Is It A Bad Idea To Only Pay Your Minimum Monthly Payment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.