Which Party Bears The Most Financial Risk In A Credit Card Transaction

adminse

Apr 01, 2025 · 8 min read

Table of Contents

Who Bears the Most Financial Risk in a Credit Card Transaction? A Deep Dive

What if the seemingly simple act of swiping a credit card hides a complex web of financial risk? Determining who bears the brunt of this risk—the cardholder, the merchant, or the card issuer—requires a nuanced understanding of the intricate processes and agreements involved.

Editor’s Note: This article on the allocation of financial risk in credit card transactions was published today, offering an up-to-date analysis of the various players involved and the measures in place to mitigate potential losses.

Why This Matters: Protecting Stakeholders in a Multi-Billion Dollar Industry

Credit card transactions underpin a vast global economy. Billions of transactions occur daily, involving millions of merchants, cardholders, and financial institutions. Understanding the distribution of financial risk in this system is crucial for protecting all stakeholders. This knowledge informs business decisions, consumer protection policies, and the overall stability of the financial ecosystem. The risks extend beyond simple fraud; they encompass chargebacks, disputes, processing fees, and the ever-present threat of cybercrime.

Overview: What This Article Covers

This article will dissect the financial risks associated with credit card transactions, examining the roles and responsibilities of each party: the cardholder, the merchant, and the card issuer. We will delve into various scenarios, including fraudulent transactions, chargebacks, and processing fees, to determine where the primary financial burden lies. The analysis will consider both the immediate and long-term consequences of these risks.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon industry reports, legal frameworks (such as the Fair Credit Billing Act in the US), and analysis of credit card processing agreements. It incorporates insights from financial experts and case studies to provide a comprehensive and accurate representation of the risk landscape.

Key Takeaways:

- Understanding the Transaction Flow: A detailed examination of how a credit card transaction moves through the system.

- Cardholder Risk: Analysis of the potential financial risks for cardholders, including fraud and unauthorized charges.

- Merchant Risk: An in-depth look at the financial risks faced by merchants, including chargebacks and processing fees.

- Issuer Risk: An exploration of the financial risks borne by credit card issuers, including fraud losses and defaults.

- Risk Mitigation Strategies: Examining strategies employed by each party to minimize their financial exposure.

Smooth Transition to the Core Discussion:

Having established the importance of understanding risk allocation in credit card transactions, let's delve into the roles and responsibilities of each participating party.

Exploring the Key Aspects of Credit Card Transaction Risk

1. The Transaction Flow: A Step-by-Step Breakdown

To understand risk allocation, we must first understand the transaction flow. A typical credit card transaction involves several key players:

- Cardholder: The individual making the purchase.

- Merchant: The business accepting the credit card payment.

- Merchant Acquiring Bank: The bank that processes the transaction for the merchant.

- Payment Processor: A third-party company that facilitates the transaction between the merchant and the acquiring bank.

- Card Network (e.g., Visa, Mastercard): The network that connects the merchant's acquiring bank to the cardholder's issuing bank.

- Issuing Bank: The bank that issued the credit card to the cardholder.

The transaction progresses as follows: The cardholder presents their card; the merchant processes the transaction through a payment processor; the acquiring bank verifies the transaction with the card network; the issuing bank authorizes the transaction; funds are transferred from the issuing bank to the acquiring bank, and finally, the merchant receives the payment (minus processing fees). Each step presents potential points of failure and risk.

2. Cardholder Risk: Limited Liability, But Not No Liability

The cardholder's risk is relatively limited thanks to consumer protection laws. The Fair Credit Billing Act (FCBA) in the US, for example, protects cardholders from unauthorized charges. If a card is lost or stolen, the cardholder's liability is typically capped at $50, although many issuers offer zero liability protection.

However, cardholders still face risks:

- Fraudulent Transactions: Even with zero liability protection, the inconvenience and time spent disputing fraudulent charges represents a significant cost.

- Identity Theft: Credit card fraud can lead to identity theft, resulting in far-reaching and long-term financial damage.

- Late Payment Fees: Failing to pay balances on time incurs significant fees, impacting the cardholder's credit score and overall financial health.

- High Interest Rates: Carrying a balance on a credit card can result in accumulating substantial interest charges.

3. Merchant Risk: Chargebacks and Processing Fees

Merchants bear considerable financial risk, primarily through:

- Chargebacks: These occur when a cardholder disputes a transaction, leading the issuing bank to reverse the payment. Chargebacks can be costly, involving fees and the potential loss of revenue. High chargeback rates can lead to merchant account suspension.

- Processing Fees: Merchants pay a percentage of each transaction as a processing fee to the acquiring bank and payment processor. These fees can significantly impact profitability, especially for businesses with low margins.

- Fraudulent Transactions: Though the liability for fraudulent transactions often rests with the issuing bank, merchants can still experience losses due to delayed payments or administrative burdens associated with investigating and resolving fraudulent activity.

4. Issuer Risk: Fraud Losses and Defaults

Issuing banks face significant risk, primarily through:

- Fraud Losses: Unauthorized transactions and fraudulent applications cost issuers substantial sums annually. While zero liability programs protect cardholders, the issuer ultimately absorbs these losses.

- Defaults: When cardholders fail to repay their balances, the issuing bank incurs a loss. Managing defaults requires significant resources and can negatively impact the bank's profitability.

- Chargeback Costs: Although the merchant initially bears the chargeback fee, the issuing bank ultimately manages and absorbs the cost in many scenarios.

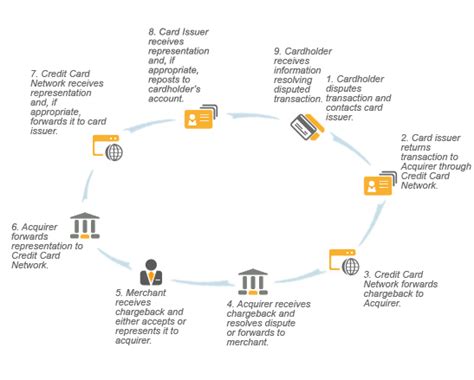

Exploring the Connection Between Chargebacks and the Allocation of Financial Risk

Chargebacks represent a pivotal point in understanding risk distribution. While the merchant initially receives the chargeback, the underlying risk often falls to the issuing bank. If a chargeback is deemed legitimate (e.g., fraudulent transaction or unauthorized purchase), the issuing bank credits the cardholder's account, absorbing the loss. The merchant, however, often bears the cost of the chargeback fee, regardless of the outcome.

Key Factors to Consider:

- Roles and Real-World Examples: Consider a case where a merchant sells counterfeit goods. The cardholder initiates a chargeback, and the issuing bank investigates. The merchant bears the chargeback fee, while the issuing bank may bear the cost of the refund, and potentially face reputational damage.

- Risks and Mitigations: Merchants can mitigate chargeback risk through robust fraud prevention measures, clear transaction descriptions, and excellent customer service. Issuers employ sophisticated fraud detection systems and risk management strategies.

- Impact and Implications: High chargeback rates can lead to merchant account closures and increased processing fees, impacting merchants' ability to accept credit cards. High fraud losses and default rates can negatively impact the profitability and stability of issuing banks.

Conclusion: Reinforcing the Connection

The interplay between chargebacks, fraud, and defaults highlights the complex and shared nature of financial risk in credit card transactions. While different parties bear different levels of responsibility at different points, the ultimate distribution of risk is multifaceted and involves multiple actors working together. No single party carries the entire burden; instead, the risk is dynamically allocated and mitigated through a series of agreements, regulations, and risk management practices.

Further Analysis: Examining Fraud Prevention Measures in Greater Detail

Effective fraud prevention measures are crucial for all parties. Merchants can implement address verification systems (AVS), card verification value (CVV) checks, and velocity checks to identify suspicious transactions. Issuers utilize sophisticated algorithms and machine learning to detect patterns of fraudulent activity. Collaboration between merchants, issuers, and payment processors is essential in combating fraud effectively.

FAQ Section: Answering Common Questions About Credit Card Transaction Risk

Q: What happens if a merchant refuses a chargeback?

A: The cardholder can escalate the dispute to their issuing bank, which will then investigate and decide on the legitimacy of the chargeback. The merchant could face further penalties.

Q: Can merchants dispute a chargeback?

A: Yes, merchants can provide evidence to support their case and attempt to overturn the chargeback.

Q: How are processing fees determined?

A: Processing fees are negotiated between the merchant and the acquiring bank, based on various factors such as transaction volume, industry, and risk profile.

Practical Tips: Maximizing the Benefits and Minimizing the Risks

- Cardholders: Protect your card information, monitor your statements regularly, and report suspicious activity immediately.

- Merchants: Implement robust fraud prevention measures, provide clear and accurate transaction descriptions, and maintain excellent customer service to minimize chargebacks.

- Issuers: Invest in advanced fraud detection systems and risk management strategies to minimize losses due to fraud and defaults.

Final Conclusion: Wrapping Up with Lasting Insights

The allocation of financial risk in credit card transactions is a dynamic and complex issue. While cardholders enjoy significant protections, merchants and issuers face substantial financial exposures. A well-functioning system requires collaboration and responsible risk management practices among all stakeholders to maintain stability and trust within this essential aspect of the global economy. Understanding the intricate web of risk is crucial for protecting all participants in this vast financial ecosystem.

Latest Posts

Latest Posts

-

How Much To Charge For Late Fee

Apr 03, 2025

-

Late Charge Fee

Apr 03, 2025

-

No Late Fees

Apr 03, 2025

-

What Is The Average Late Fee

Apr 03, 2025

-

How Much Are Late Fees

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about Which Party Bears The Most Financial Risk In A Credit Card Transaction . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.