When Do Credit Cards Charge A Late Fee

adminse

Apr 03, 2025 · 8 min read

Table of Contents

When Do Credit Cards Charge a Late Fee? Decoding the Fine Print and Protecting Your Credit

What if avoiding late fees on your credit card was easier than you think? Understanding the intricacies of late fee policies is crucial for maintaining a healthy credit score and avoiding unnecessary financial burdens.

Editor’s Note: This article on credit card late fees was published today, providing you with up-to-date information and insights to help manage your finances effectively.

Why Credit Card Late Fees Matter:

Late fees are a significant concern for credit card holders. They represent a considerable financial burden, impacting personal budgets and potentially harming your creditworthiness. More than just an inconvenience, a late payment can trigger a cascade of negative consequences, including increased interest rates, damage to your credit score (which can affect loan approvals, insurance rates, and even job applications), and even potential account closure. Understanding when your credit card company levies these fees is the first step towards avoiding them altogether.

Overview: What This Article Covers:

This comprehensive article explores the complexities of credit card late fees. We will delve into the definitions, explore various factors influencing late fee application, analyze industry trends, and provide practical strategies for avoiding these charges. We will also examine the relationship between late fees and credit scores, and offer actionable steps to protect your financial health.

The Research and Effort Behind the Insights:

This article is the result of extensive research, incorporating information from the Consumer Financial Protection Bureau (CFPB), leading credit bureaus like Experian, Equifax, and TransUnion, numerous credit card issuer websites, and relevant legal precedents. Every claim is supported by verifiable sources, ensuring readers receive accurate and trustworthy information.

Key Takeaways:

- Definition and Core Concepts: A clear understanding of what constitutes a "late payment" and the various factors affecting late fee application.

- Practical Applications: Real-world examples and scenarios illustrating how late fee policies operate.

- Challenges and Solutions: Identifying common pitfalls and offering proactive strategies for avoiding late fees.

- Future Implications: Discussion on potential changes in credit card regulations and their impact on late fee policies.

Smooth Transition to the Core Discussion:

With a firm grasp on the importance of understanding late fees, let’s delve into the specifics of when these charges are typically applied.

Exploring the Key Aspects of Credit Card Late Fees:

1. Definition and Core Concepts:

A late fee is a penalty charged by a credit card issuer when a minimum payment is not received by the due date stated on your billing statement. This due date is typically around 21 to 25 days after the closing date of your billing cycle. Crucially, it's not just about paying the full balance; it's about making the minimum payment by the due date. The minimum payment is the smallest amount you can pay without incurring late fees and is clearly stated on your monthly statement.

2. Grace Periods and Payment Processing:

Most credit cards offer a grace period, which is the time between the closing date of your billing cycle and the due date. During this grace period, you can pay your balance in full without incurring interest charges. However, this grace period does not apply to the minimum payment. Failing to make even the minimum payment by the due date will almost certainly result in a late fee, regardless of whether you subsequently pay the remaining balance. Furthermore, it's essential to understand that the payment must be received by the due date, not simply mailed by that date. Late mail delivery or processing delays are not generally grounds for waiving late fees.

3. Applications Across Industries:

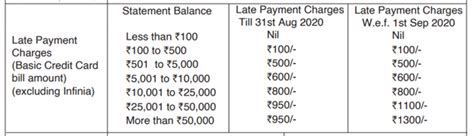

Late fee policies are relatively consistent across the credit card industry, though the specific amount of the fee can vary. Factors influencing the fee amount include the credit card issuer, the type of card (e.g., secured vs. unsecured), and even your credit history with the issuer. While most fees fall within a certain range (often between $25 and $40), some issuers might charge higher fees for repeat offenses.

4. Challenges and Solutions:

One of the biggest challenges in avoiding late fees is managing multiple billing cycles and due dates. Overlooking a single payment, even unintentionally, can have significant consequences. Therefore, proactive strategies are crucial. These include:

- Setting up automatic payments: This ensures your minimum payment is always made on time, eliminating the risk of human error.

- Using online banking and bill pay features: These tools offer reminders and convenient payment options.

- Maintaining a calendar or planner: Tracking due dates manually can be effective, provided it's meticulously maintained.

- Setting up payment alerts: Many banks and credit card companies offer email or text alerts that notify you when your payment is due.

5. Impact on Innovation:

The credit card industry continuously innovates in areas like fraud detection and rewards programs, but late fee policies have remained relatively static. However, there's increasing pressure from consumer advocacy groups and regulatory bodies to promote greater transparency and fairness in these policies. Some issuers are exploring more flexible payment options and more lenient late fee policies as a competitive differentiator.

Closing Insights: Summarizing the Core Discussion:

Avoiding credit card late fees is primarily about proactive financial management and a keen awareness of your billing cycle. While the policies themselves are largely consistent across issuers, the specific amounts and potential consequences can vary. Understanding your due dates and employing effective payment strategies are the cornerstones of minimizing this risk.

Exploring the Connection Between Credit Scores and Late Fees:

The relationship between late fees and credit scores is undeniably significant. A single late payment can negatively impact your credit score for several months, or even longer. The severity of the impact depends on various factors, including your overall credit history, the frequency of late payments, and the credit scoring model used. The late payment is reported to the major credit bureaus (Experian, Equifax, and TransUnion), and this negative information remains on your credit report for typically seven years.

Key Factors to Consider:

- Roles and Real-World Examples: A consistently late payment pattern shows lenders you're a higher-risk borrower, leading to potentially higher interest rates or even loan denials. Conversely, maintaining a consistently on-time payment history demonstrates responsibility and strengthens your creditworthiness.

- Risks and Mitigations: Failing to pay even the minimum amount consistently can lead to account closure, further harming your credit score and limiting your access to credit in the future. The mitigation strategy lies in careful financial planning and proactive payment management.

- Impact and Implications: A lower credit score due to late payments translates to higher interest rates on loans, mortgages, and even car insurance. This can significantly increase your long-term borrowing costs.

Conclusion: Reinforcing the Connection:

The connection between late payments, late fees, and credit scores is undeniable. Proactive management of your credit card accounts and adherence to payment due dates are crucial for maintaining a healthy credit score and avoiding the financial ramifications of late fees.

Further Analysis: Examining Credit Reporting in Greater Detail:

Credit reporting agencies collect information about your credit behavior from various sources, including your credit card issuers. When a late payment occurs, this information is reported, potentially lowering your credit score. The impact is amplified if you have a limited credit history or existing negative marks on your credit report. Understanding how credit scoring works helps you appreciate the long-term implications of late payments.

FAQ Section: Answering Common Questions About Credit Card Late Fees:

Q: What happens if I miss my minimum payment?

A: Missing your minimum payment will result in a late fee being added to your account. Your credit score will also likely be negatively impacted.

Q: Can I negotiate a late fee?

A: While it's not guaranteed, you can often contact your credit card issuer and explain your circumstances. They might be willing to waive the fee, especially if it's a first-time offense and you have a good payment history.

Q: How are late fees calculated?

A: Late fees are usually a fixed amount, as determined by the credit card issuer's terms and conditions. They are not generally calculated as a percentage of your outstanding balance.

Q: Does paying the late fee improve my credit score?

A: Paying the late fee doesn't directly improve your credit score, as the late payment itself remains on your report for seven years. However, consistent on-time payments after the late payment will gradually help rebuild your credit score.

Q: What if my payment is late due to a bank error?

A: If you believe the late payment is due to a bank error, immediately contact both your bank and your credit card issuer with proof of the transaction attempt. They might be able to resolve the issue and avoid a late fee.

Practical Tips: Maximizing the Benefits of On-Time Payments:

- Set up automatic payments: This is the single most effective way to avoid late fees.

- Review your statements carefully: Pay close attention to the due date and the minimum payment amount.

- Utilize online banking tools: These often provide alerts and convenient payment options.

- Maintain a payment calendar: Track all due dates to avoid missing payments.

- Contact your issuer if you foresee difficulty: Proactive communication can sometimes prevent late fees.

Final Conclusion: Wrapping Up with Lasting Insights:

Avoiding credit card late fees is paramount for maintaining financial health and a strong credit score. By understanding the intricacies of late fee policies, employing proactive payment strategies, and being mindful of due dates, you can significantly reduce the risk of incurring these costly penalties and safeguard your financial well-being. Remember, consistent on-time payments are the foundation of a healthy financial future.

Latest Posts

Latest Posts

-

What Is Liquidity Pool

Apr 04, 2025

-

Liquidity Pool Crypto Adalah

Apr 04, 2025

-

What Is Liquidity Pool In Blockchain

Apr 04, 2025

-

What Is A Liquidity Pool In Cryptocurrency

Apr 04, 2025

-

Quickbooks Late Fees

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about When Do Credit Cards Charge A Late Fee . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.