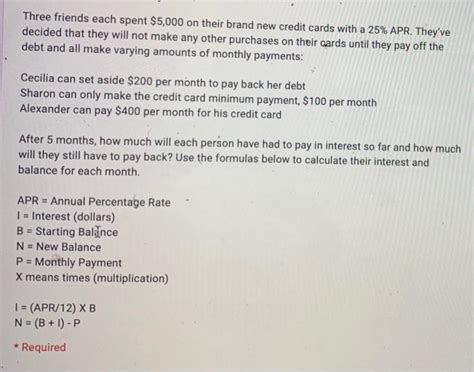

What Is The Minimum Payment On A $5000 Credit Card Balance

adminse

Apr 04, 2025 · 7 min read

Table of Contents

Decoding Minimum Payments: Understanding Your $5,000 Credit Card Balance

What if the seemingly innocuous minimum payment on a $5,000 credit card balance could trap you in a cycle of debt for years? Understanding this seemingly small number is crucial for financial health and avoiding a debt spiral.

Editor’s Note: This article provides up-to-date information on minimum credit card payments and their implications. The information is for educational purposes and should not be considered financial advice. Consult with a financial professional for personalized guidance.

Why Minimum Payments Matter: A $5,000 Debt Reality Check

A $5,000 credit card balance represents a significant debt burden. Many individuals grapple with this level of debt, often relying on minimum payments to manage their finances. However, relying solely on minimum payments can have severe long-term consequences, including:

- Prolonged Debt: Minimum payments typically only cover the interest accrued, leaving the principal balance largely untouched. This significantly extends the repayment period, potentially costing thousands more in interest over time.

- Increased Interest Charges: High interest rates on credit cards can quickly accumulate, making it challenging to make substantial progress on the principal balance. The longer the debt remains outstanding, the more interest will be added.

- Damage to Credit Score: A high credit utilization ratio (the percentage of available credit used) negatively impacts your credit score. Consistently carrying a large balance on your credit card will likely hurt your creditworthiness.

- Financial Stress: The constant worry and stress associated with managing a large debt can negatively affect mental and emotional well-being.

Understanding the mechanics of minimum payments, particularly with a sizable balance like $5,000, is crucial for developing a responsible repayment strategy.

Overview: What This Article Covers

This article explores the complexities of minimum payments on a $5,000 credit card balance. We'll examine:

- How minimum payments are calculated.

- The factors influencing minimum payment amounts.

- The long-term cost of minimum payments.

- Strategies for faster debt repayment.

- Resources and tools for managing credit card debt.

The Research and Effort Behind the Insights

This article draws upon extensive research from reputable financial institutions, government agencies (like the Consumer Financial Protection Bureau), and peer-reviewed academic studies on consumer debt. We've analyzed various credit card agreements and employed realistic scenarios to illustrate the implications of different repayment strategies.

Key Takeaways:

- Minimum payment calculations vary: They're not a fixed percentage and depend on several factors.

- Minimum payments primarily cover interest: They barely dent the principal balance.

- High interest rates accelerate debt growth: Ignoring this aspect can lead to financial trouble.

- Debt snowball and avalanche methods are effective: They offer structured repayment strategies.

Smooth Transition to the Core Discussion:

Now that we understand the potential consequences of relying solely on minimum payments, let's delve into the specifics of how these amounts are determined and the best ways to navigate a $5,000 credit card balance.

Exploring the Key Aspects of Minimum Payments

1. Definition and Core Concepts: The minimum payment is the smallest amount a credit card company requires you to pay each month to remain in good standing. Failing to meet this minimum can result in late fees, penalties, and negative impacts on your credit score.

2. Applications Across Industries: While the fundamental principle of minimum payments remains consistent across credit card issuers, the specific calculation methods and minimum payment amounts can vary slightly. Some companies may use a fixed percentage (e.g., 2% of the balance), while others may use a sliding scale based on the outstanding balance.

3. Challenges and Solutions: The primary challenge with minimum payments is their slow pace of debt reduction. The solution is to pay more than the minimum whenever possible, accelerating debt repayment and reducing overall interest paid.

4. Impact on Innovation: The credit card industry is constantly evolving, with some companies introducing features aimed at helping consumers manage their debt more effectively. However, the core mechanics of minimum payments and their potential for creating debt traps remain largely unchanged.

Closing Insights: Summarizing the Core Discussion

Understanding your minimum payment is vital for managing credit card debt, especially with a substantial balance. While it might seem manageable to pay the minimum on a $5,000 debt, this approach will prolong your repayment significantly and increase the total interest paid. Strategic repayment strategies are crucial for faster debt elimination and improved financial health.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is paramount. High interest rates significantly impact the efficacy of minimum payments. A higher interest rate means a larger portion of your minimum payment goes towards interest, leaving less to reduce the principal balance.

Key Factors to Consider:

-

Roles and Real-World Examples: Imagine a credit card with a 20% APR and a $5,000 balance. The minimum payment might only be $100, but a significant portion of that goes to interest. This leaves a minimal amount to reduce the principal, leading to slow progress.

-

Risks and Mitigations: The risk is getting trapped in a cycle of debt. Mitigation involves increasing your payments beyond the minimum, exploring balance transfer options with lower interest rates, or seeking debt consolidation options.

-

Impact and Implications: Failing to address the high interest rate can significantly extend repayment, costing thousands in extra interest. This can severely impact your financial stability and long-term goals.

Conclusion: Reinforcing the Connection

The connection between high interest rates and minimum payments is critical to understand. High interest rates drastically reduce the effectiveness of minimum payments, leading to slow debt reduction and increased overall cost. Taking proactive steps to address this dynamic is crucial for responsible debt management.

Further Analysis: Examining Interest Rate Calculation in Greater Detail

Interest rates on credit cards are typically expressed as an Annual Percentage Rate (APR). This APR is divided by 12 to calculate the monthly interest charge. The monthly interest is then applied to the outstanding balance, impacting the calculation of the minimum payment. Understanding this calculation highlights the importance of minimizing your balance as quickly as possible.

FAQ Section: Answering Common Questions About Minimum Payments on a $5,000 Balance

-

Q: What is the typical minimum payment percentage on a credit card? A: There's no single answer; it varies from 1% to 3% or more, depending on the issuer and balance.

-

Q: How long will it take to pay off a $5,000 credit card balance using only minimum payments? A: This depends heavily on the APR and minimum payment amount, but it could take many years, resulting in significantly increased interest charges.

-

Q: What happens if I don't make the minimum payment? A: You'll likely incur late fees and penalties, your credit score will suffer, and your account may be reported to collections agencies.

-

Q: Are there any strategies to pay off my $5,000 balance faster? A: Yes, consider debt snowball or avalanche methods, balance transfer cards, or debt consolidation loans.

Practical Tips: Maximizing the Benefits of Strategic Repayment

- Understand your APR: Knowing your interest rate is the first step in developing a repayment plan.

- Create a budget: Track your income and expenses to determine how much extra you can allocate to debt repayment.

- Explore debt repayment methods: Consider the debt snowball or avalanche methods.

- Negotiate with your creditor: Inquire about options for lower interest rates or payment plans.

- Seek professional help: If you're struggling, consult a credit counselor or financial advisor.

Final Conclusion: Wrapping Up with Lasting Insights

The minimum payment on a $5,000 credit card balance might seem manageable, but it's a deceptive figure. Ignoring the high interest rates and the slow repayment it implies can trap you in a cycle of debt for years. By understanding how minimum payments work, strategically allocating extra funds, and exploring different repayment strategies, you can take control of your finances and achieve debt freedom faster. Don't let the illusion of a small minimum payment overshadow the significant long-term financial implications. Proactive debt management is key to securing your financial future.

Latest Posts

Latest Posts

-

What Is The Lowest Paying Job At Home Depot

Apr 05, 2025

-

What Is The Minimum Age For Home Depot

Apr 05, 2025

-

What Is The Lowest Pay At Home Depot

Apr 05, 2025

-

What Is The Minimum Pay At Home Depot

Apr 05, 2025

-

What Is The Minimum Payment On Home Depot Credit Card

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A $5000 Credit Card Balance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.