What Is The Minimum Payment On A 25000 Credit Card

adminse

Apr 04, 2025 · 8 min read

Table of Contents

What's the magic number? Unveiling the minimum payment mystery on a $25,000 credit card.

Understanding your minimum payment is key to avoiding crippling debt; it's not as simple as you might think.

Editor’s Note: This article on minimum credit card payments, specifically concerning a $25,000 balance, was published today. It provides up-to-date information and strategies for managing high-balance credit card debt.

Why Understanding Minimum Payments on a $25,000 Credit Card Matters

Carrying a $25,000 balance on a credit card is a significant financial burden. Ignoring or misunderstanding the minimum payment can lead to a vicious cycle of accumulating interest, escalating debt, and potential damage to your credit score. Knowing what your minimum payment is and its implications is crucial for responsible debt management and financial well-being. This knowledge empowers you to make informed decisions, potentially saving thousands of dollars in interest charges over time. The information presented here is vital for anyone struggling with high-balance credit card debt, offering insights into managing their finances effectively.

Overview: What This Article Covers

This article will comprehensively examine the concept of minimum credit card payments, focusing specifically on a $25,000 balance. We’ll explore how minimum payments are calculated, the factors influencing their amount, the long-term consequences of only paying the minimum, strategies for paying down debt more effectively, and resources available to help manage high-balance credit card debt. We'll also address frequently asked questions and provide practical tips for improving your financial health.

The Research and Effort Behind the Insights

The information presented in this article is based on extensive research, incorporating data from reputable financial institutions, consumer finance websites, and credit counseling agencies. We’ve analyzed various credit card agreements, interest rate calculations, and debt repayment strategies to ensure accuracy and provide practical guidance to readers. Every piece of advice is backed by evidence and intended to help you navigate the complexities of managing high-balance credit card debt.

Key Takeaways:

- Minimum Payment Calculation: Understanding the formula and variables involved.

- Impact of Minimum Payments: The long-term cost of only paying the minimum.

- Debt Repayment Strategies: Accelerated payment methods to reduce debt faster.

- Credit Score Implications: How minimum payments affect your creditworthiness.

- Available Resources: Organizations offering assistance with credit card debt.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding minimum payments on a significant credit card balance, let's delve into the specifics. We'll begin by examining how these minimum payments are actually determined.

Exploring the Key Aspects of Minimum Credit Card Payments

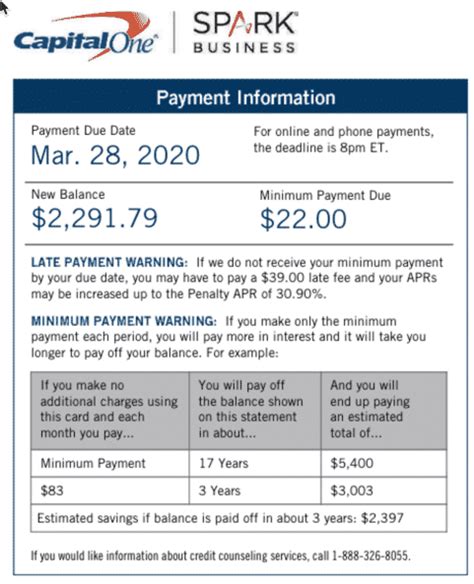

1. Definition and Core Concepts: The minimum payment is the smallest amount a credit card issuer requires you to pay each month to avoid late fees and keep your account in good standing. It typically represents a small percentage of your outstanding balance (often 1-3%), plus any accrued interest and fees.

2. Applications Across Industries: While the core concept remains consistent across credit card issuers, the exact calculation method might vary slightly. Some issuers might use a fixed minimum payment amount, while others use a percentage-based calculation.

3. Challenges and Solutions: The primary challenge with minimum payments is their slow progress in reducing the principal balance. A high balance combined with a minimum payment approach will see a disproportionate amount going towards interest, perpetuating the debt. The solution involves understanding the compound interest effect and actively seeking strategies to pay more than the minimum.

4. Impact on Innovation (Debt Management Strategies): The financial industry continuously develops innovative debt management tools and strategies, including balance transfer cards, debt consolidation loans, and credit counseling services. These options offer alternative pathways to efficiently reduce high-balance credit card debt.

Calculating the Minimum Payment: The Unseen Factors

There's no single, universally applicable formula to determine the minimum payment on a $25,000 credit card. It varies depending on the card issuer's policies and your specific card agreement. However, the most common method involves a combination of:

- Percentage of the outstanding balance: This is often 1% to 3% of your balance. On a $25,000 balance, this could range from $250 to $750.

- Accrued interest: The interest calculated on your outstanding balance since the last payment is always added to the minimum payment. This amount varies based on your Annual Percentage Rate (APR). A higher APR means a higher interest component.

- Fees: Any late fees, over-limit fees, or other charges incurred are added to the minimum payment.

The exact minimum payment will be clearly stated on your monthly credit card statement. It's crucial to review this statement carefully to understand the breakdown of your payment and the proportion allocated to principal vs. interest.

The Long-Term Cost of Minimum Payments: The Debt Trap

While the minimum payment seems manageable, consistently paying only the minimum on a $25,000 balance can have devastating long-term financial consequences. The primary issue is the power of compound interest. A significant portion of your monthly payment goes towards interest, meaning only a small amount is reducing the principal. This can trap you in a cycle of debt for years, potentially costing tens of thousands of dollars in additional interest.

Exploring the Connection Between Interest Rates and Minimum Payments

The Annual Percentage Rate (APR) is a crucial factor influencing the minimum payment and the overall cost of debt. A higher APR significantly increases the interest component of your minimum payment, leaving less money to reduce the principal balance. This makes paying down high-interest debt even more challenging. It's therefore critical to understand your APR and explore options to lower it, if possible.

Key Factors to Consider:

- Roles and Real-World Examples: Consider someone consistently paying only the minimum on a $25,000 credit card with a 19% APR. The majority of their payments would be interest, resulting in slow or no progress toward reducing the principal.

- Risks and Mitigations: The risk is prolonged debt and substantial interest charges. Mitigations include proactively seeking lower interest rates, exploring balance transfers, or accelerating payments.

- Impact and Implications: The impact can be significant financial stress, damage to credit scores, and long-term financial instability.

Strategies for Accelerated Debt Repayment: Breaking Free

The most effective strategy for overcoming a $25,000 credit card debt is to pay more than the minimum each month. Consider these options:

- Debt Avalanche Method: Focus on paying off the highest-interest debt first. This minimizes the overall interest paid.

- Debt Snowball Method: Pay off the smallest debt first, for a motivational boost. Then, roll that payment amount into the next smallest debt.

- Balance Transfer: Transfer your balance to a card with a lower APR to reduce interest charges.

- Debt Consolidation Loan: Consolidate your debt into a single loan with a potentially lower interest rate.

- Credit Counseling: Seek professional help from a reputable credit counseling agency to develop a debt management plan.

Conclusion: Reinforcing the Connection

The relationship between minimum payments and high-balance credit card debt is critical. While minimum payments provide a short-term solution for avoiding immediate penalties, they ultimately delay debt reduction and increase the overall cost. Paying more than the minimum, exploring various repayment strategies, and seeking professional help are crucial steps towards financial freedom.

Further Analysis: Examining Interest Calculation in Greater Detail

The interest calculation on credit cards is typically done using the average daily balance method. This method calculates the interest based on your average daily balance for the billing cycle. Understanding this method is essential for accurately predicting your interest charges and planning your repayment strategy.

FAQ Section: Answering Common Questions About Minimum Payments

- Q: What happens if I only pay the minimum payment on my credit card? A: You'll pay more interest over time, and it will take much longer to pay off your balance.

- Q: Can I negotiate my minimum payment with my credit card company? A: Generally, this isn't possible. However, you can explore debt consolidation or balance transfer options.

- Q: What if I miss a minimum payment? A: You’ll likely incur late fees, negatively impacting your credit score.

- Q: How does paying more than the minimum impact my credit score? A: It demonstrates responsible credit management, positively impacting your credit score over time.

Practical Tips: Maximizing the Benefits of Responsible Credit Management

- Create a Budget: Track your income and expenses to identify areas for savings.

- Prioritize Debt Repayment: Allocate more funds towards your credit card debt each month.

- Explore Debt Management Strategies: Evaluate options like balance transfers, debt consolidation, or credit counseling.

- Seek Professional Help: If overwhelmed, consult a financial advisor or credit counselor.

- Monitor Your Credit Report: Regularly check your credit report for accuracy and identify any issues.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your minimum payment on a $25,000 credit card is just the first step towards effective debt management. While the minimum payment might seem manageable in the short term, it’s a costly trap in the long run. By understanding the implications, exploring alternative strategies, and taking proactive steps, you can regain control of your finances and move towards a debt-free future. Proactive management and a well-defined repayment plan are your best tools to navigate this challenge and achieve long-term financial stability.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On A Home Equity Line Of Credit

Apr 05, 2025

-

What Is The Minimum Payment On A Cibc Line Of Credit

Apr 05, 2025

-

What Is The Minimum Payment On A Bmo Line Of Credit

Apr 05, 2025

-

What Is The Minimum Payment On A Scotiabank Line Of Credit

Apr 05, 2025

-

What Is The Minimum Payment On A Td Line Of Credit

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A 25000 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.