What Is Fraud Protection On A Credit Card

adminse

Apr 01, 2025 · 9 min read

Table of Contents

What safeguards are in place to protect your credit card from fraud?

Credit card fraud protection is a multifaceted system designed to minimize financial losses and safeguard cardholders from unauthorized transactions.

Editor’s Note: This article on credit card fraud protection was published on [Date]. This comprehensive guide provides up-to-date information on the various methods and technologies used to protect consumers from credit card fraud.

Why Credit Card Fraud Protection Matters:

Credit card fraud poses a significant threat to both individuals and financial institutions. The rise of e-commerce and digital transactions has expanded the avenues for fraudulent activities, making robust protection mechanisms crucial. Understanding the intricacies of credit card fraud protection allows consumers to make informed decisions, minimize their risk, and take proactive steps to safeguard their finances. Businesses also benefit from understanding these protections as they directly impact their operational costs and customer trust. The consequences of fraud extend beyond monetary loss; they can damage credit scores, lead to identity theft, and cause significant emotional distress.

Overview: What This Article Covers:

This article delves into the comprehensive landscape of credit card fraud protection. We will explore various layers of security, including the roles of issuers, merchants, and consumers; technological advancements like EMV chips and tokenization; and proactive measures individuals can take to minimize their vulnerability. We will also examine the impact of fraud on businesses and the evolving strategies employed to combat this ongoing challenge.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing upon reports from reputable organizations like the Federal Trade Commission (FTC), Nilson Report, and industry publications. Information is synthesized from various sources, including consumer protection agencies, financial institutions, and cybersecurity experts. The goal is to present an accurate, unbiased, and up-to-date perspective on credit card fraud protection.

Key Takeaways:

- Definition and Core Concepts: Understanding the basics of credit card fraud and the different types of fraud.

- Issuer-Level Protections: Examining the security measures implemented by credit card companies.

- Merchant-Level Protections: Exploring the role of businesses in preventing and detecting fraud.

- Cardholder Responsibilities: Highlighting the proactive steps consumers can take to protect themselves.

- Technological Advancements: Discussing the role of EMV chips, tokenization, and other technologies.

- Fraud Detection and Prevention Methods: Exploring how fraud is identified and prevented.

- Dispute Resolution Processes: Understanding how to report and resolve fraudulent transactions.

Smooth Transition to the Core Discussion:

Now that we've established the importance of credit card fraud protection, let's delve into the specifics of how this protection works and what measures are in place to safeguard your financial security.

Exploring the Key Aspects of Credit Card Fraud Protection:

1. Definition and Core Concepts:

Credit card fraud encompasses any unauthorized use of a credit card to make purchases or withdraw cash. This can range from stolen cards used for in-person transactions to online scams involving phishing or data breaches. Different types of fraud include:

- Card-Present Fraud: Fraudulent transactions made with the physical card present at a point-of-sale terminal.

- Card-Not-Present Fraud: Fraudulent transactions made without the physical card present, typically online or over the phone.

- Account Takeover Fraud: Fraudsters gain access to a cardholder's account information and make unauthorized transactions.

- Application Fraud: Fraudsters apply for credit cards using stolen identities or fabricated information.

2. Issuer-Level Protections:

Credit card issuers play a crucial role in preventing and mitigating fraud. These protections include:

- Fraud Monitoring Systems: Sophisticated systems that analyze transaction data in real-time to identify suspicious patterns and flag potential fraud. These systems use machine learning algorithms to detect anomalies based on factors like location, transaction amount, and spending habits.

- Zero Liability Policies: Many issuers offer zero liability policies, protecting cardholders from unauthorized charges if they report the fraud promptly. This shifts the financial burden from the consumer to the issuer.

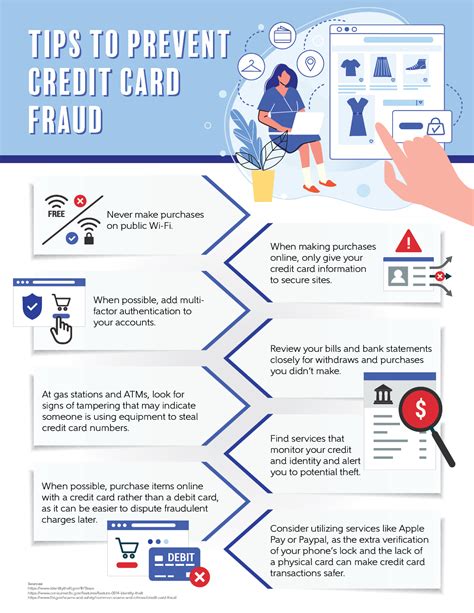

- Transaction Alerts: Cardholders can often enroll in transaction alert services, receiving notifications via text message or email whenever a purchase is made. This allows for prompt detection of unauthorized activity.

- Enhanced Security Measures: Issuers continuously update their security protocols to combat emerging threats. This includes implementing advanced encryption methods and regularly patching vulnerabilities in their systems.

3. Merchant-Level Protections:

Merchants also have a responsibility to protect cardholder data and prevent fraud. Key merchant-level protections include:

- Point-of-Sale (POS) Security: Merchants should utilize secure POS systems with encryption to protect card data during transactions. Regular software updates and security audits are essential.

- EMV Chip Card Acceptance: The adoption of EMV (Europay, MasterCard, and Visa) chip cards and chip card readers significantly reduces card-present fraud by making it more difficult to counterfeit cards.

- Data Encryption: Protecting cardholder data through encryption during transmission and storage is crucial. Compliance with industry standards like PCI DSS (Payment Card Industry Data Security Standard) is mandatory for merchants.

4. Cardholder Responsibilities:

Consumers play a vital role in preventing credit card fraud. Proactive measures include:

- Regularly Monitoring Account Statements: Checking statements for unauthorized transactions is essential for early fraud detection.

- Strong Password Protection: Creating strong, unique passwords for online accounts is crucial to prevent account takeover fraud.

- Avoiding Phishing Scams: Being wary of suspicious emails or phone calls requesting personal or financial information is paramount.

- Using Secure Wi-Fi Networks: Avoiding public Wi-Fi for online transactions minimizes the risk of data interception.

- Reporting Suspicious Activity Immediately: Contacting the issuer immediately if any unauthorized activity is suspected is crucial.

5. Technological Advancements:

Technological advancements are continuously enhancing credit card fraud protection:

- EMV Chip Cards: These cards embed a microchip that encrypts transaction data, making it much more difficult for fraudsters to clone or counterfeit cards.

- Tokenization: Replacing sensitive card data with unique tokens for online transactions reduces the risk of data breaches.

- Biometric Authentication: Using fingerprints, facial recognition, or other biometric data adds an extra layer of security to online transactions.

- Artificial Intelligence (AI) and Machine Learning (ML): AI and ML algorithms are used in fraud detection systems to analyze vast amounts of transaction data and identify suspicious patterns in real-time.

6. Fraud Detection and Prevention Methods:

Credit card fraud detection involves a combination of technology and human analysis. Sophisticated algorithms analyze transaction data, identifying anomalies that might indicate fraudulent activity. These systems often use machine learning to improve their accuracy over time, adapting to new fraud techniques. Human analysts also review flagged transactions, confirming or refuting suspicions.

7. Dispute Resolution Processes:

If a fraudulent transaction occurs, the cardholder should immediately contact their issuer to report the incident. The issuer will investigate the claim and determine whether the charge is legitimate. If the charge is deemed fraudulent, the issuer will typically reverse the charge and credit the account. Documentation of the fraudulent activity, such as copies of statements and police reports, can expedite the dispute resolution process.

Exploring the Connection Between Account Monitoring and Credit Card Fraud Protection:

The relationship between diligent account monitoring and credit card fraud protection is paramount. Regularly reviewing account statements allows for early detection of fraudulent transactions, minimizing potential financial losses. This proactive approach complements other layers of protection, providing a crucial safeguard against unauthorized activity.

Key Factors to Consider:

- Roles and Real-World Examples: Account monitoring is a consumer-led initiative, enhancing the effectiveness of issuer-level fraud detection systems. For example, a cardholder noticing an unauthorized purchase at a store they haven't visited can immediately report it, preventing further losses.

- Risks and Mitigations: The risk of delayed fraud detection increases with infrequent account monitoring. Regular statement review and utilizing transaction alerts mitigate this risk significantly.

- Impact and Implications: Effective account monitoring can reduce financial losses, protect credit scores, and prevent identity theft. Conversely, neglecting account monitoring can lead to significant financial hardship and damage to creditworthiness.

Conclusion: Reinforcing the Connection:

Diligent account monitoring forms an integral part of a comprehensive credit card fraud protection strategy. It is a proactive measure that empowers consumers to detect and report fraudulent activity quickly, working in tandem with issuer-level protections and technological advancements to safeguard financial security.

Further Analysis: Examining Account Monitoring in Greater Detail:

Account monitoring goes beyond simply reviewing statements. It includes utilizing online banking features to track transactions in real-time, opting for transaction alerts, and regularly reviewing credit reports for any unauthorized accounts or inquiries. This comprehensive approach enhances fraud detection and provides multiple layers of defense against fraudulent activities.

FAQ Section: Answering Common Questions About Credit Card Fraud Protection:

Q: What is zero liability protection? A: Zero liability protection means that cardholders are not responsible for unauthorized charges if they report the fraud promptly. However, the specific terms and conditions can vary depending on the issuer.

Q: How do I report credit card fraud? A: Contact your credit card issuer immediately upon suspecting fraudulent activity. They will provide instructions on how to report the fraud and initiate the dispute resolution process.

Q: What is EMV chip technology? A: EMV chip technology embeds a microchip into credit cards, encrypting transaction data and making it more secure than traditional magnetic stripe cards.

Q: How can I protect myself from phishing scams? A: Be wary of unsolicited emails or phone calls requesting personal or financial information. Never click on links in suspicious emails or provide your card details over the phone unless you initiated the contact.

Q: What is tokenization? A: Tokenization replaces sensitive card details with unique tokens, protecting the actual card information during online transactions.

Practical Tips: Maximizing the Benefits of Credit Card Fraud Protection:

- Enroll in Transaction Alerts: Receive immediate notifications about transactions on your account.

- Review Your Statements Regularly: Check your statements for unfamiliar charges or unusual activity.

- Use Strong Passwords: Create unique, strong passwords for all your online accounts.

- Be Cautious Online: Avoid using public Wi-Fi for online banking or shopping.

- Report Suspicious Activity Immediately: Don't delay reporting any potential fraud to your card issuer.

Final Conclusion: Wrapping Up with Lasting Insights:

Credit card fraud protection is a continuous evolution, with both issuers and consumers needing to adapt to emerging threats. By understanding the various layers of protection, taking proactive steps, and staying informed about the latest security measures, individuals and businesses can significantly minimize their vulnerability to credit card fraud and safeguard their financial security in an increasingly digital world. Vigilance and proactive engagement are key to maintaining a robust defense against this persistent threat.

Latest Posts

Latest Posts

-

What Is The Fee For Renewal Of Driving License

Apr 03, 2025

-

Why Is Td Charging Me A Monthly Account Fee

Apr 03, 2025

-

Is Td Bank Charging Overdraft Fees

Apr 03, 2025

-

Why Does Td Charge A Maintenance Fee

Apr 03, 2025

-

Why Does Td Bank Charge A Maintenance Fee

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about What Is Fraud Protection On A Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.