What Is An Ideal Credit Utilization Percentage

adminse

Apr 07, 2025 · 7 min read

Table of Contents

What's the Ideal Credit Utilization Percentage? Unlocking the Secrets to a Healthy Credit Score

What if maintaining a pristine credit score was as simple as understanding one key metric? Your credit utilization ratio holds the key to unlocking financial freedom and achieving your credit goals.

Editor’s Note: This article on ideal credit utilization percentage was published today, providing readers with up-to-date insights and strategies for credit score management.

Why Credit Utilization Matters: Relevance, Practical Applications, and Industry Significance

Credit utilization, simply put, is the ratio of your outstanding credit card debt to your total available credit. It’s a critical factor influencing your credit score, significantly more so than many realize. Lenders closely scrutinize this metric because it offers a glimpse into your borrowing habits and your ability to manage debt responsibly. A high utilization ratio suggests overreliance on credit, potentially indicating a higher risk of default. Conversely, a low utilization ratio demonstrates financial discipline and responsible credit management, boosting your creditworthiness and making you a more attractive borrower. This impacts not only your credit score but also your interest rates on loans, your ability to secure credit in the future, and even your insurance premiums.

Overview: What This Article Covers

This article provides a comprehensive exploration of ideal credit utilization percentages. We will delve into the definition, the impact on credit scores, strategies for maintaining a healthy utilization ratio, and address common misconceptions. We will also examine the nuances of different credit card types and explore how to navigate specific situations that may impact your utilization. Readers will gain actionable insights and practical advice to improve their credit health.

The Research and Effort Behind the Insights

This article draws upon extensive research, incorporating data from leading credit bureaus like Experian, Equifax, and TransUnion, along with analysis from financial experts and industry publications. We have carefully examined numerous studies on the correlation between credit utilization and credit scores to provide accurate and reliable information.

Key Takeaways:

- Definition and Core Concepts: A clear understanding of credit utilization and its components.

- Impact on Credit Scores: The direct correlation between utilization and credit score fluctuations.

- Ideal Utilization Range: Identifying the optimal percentage for maximizing credit health.

- Strategies for Improvement: Practical tips and techniques for lowering credit utilization.

- Addressing Specific Scenarios: Guidance on managing utilization in various situations (e.g., unexpected expenses, multiple credit cards).

- Mythbusting: Dispelling common misconceptions about credit utilization.

Smooth Transition to the Core Discussion

Now that we understand the importance of credit utilization, let’s delve into the specifics. What constitutes an ideal percentage, and how can you achieve and maintain it?

Exploring the Key Aspects of Credit Utilization

1. Definition and Core Concepts:

Credit utilization is calculated as the total amount of credit you're using divided by your total available credit, expressed as a percentage. For example, if you have a total credit limit of $10,000 across all your cards and currently owe $2,000, your credit utilization is 20%. This simple calculation is a powerful indicator of your financial responsibility to lenders.

2. Impact on Credit Scores:

Credit utilization is one of the most significant factors influencing your credit score, accounting for approximately 30%. A higher utilization percentage negatively impacts your score because it suggests a greater risk of default. Lenders perceive borrowers with high utilization as more likely to struggle with repayments, leading to a higher risk assessment. Conversely, maintaining a low utilization ratio demonstrates responsible financial behavior, signaling to lenders that you manage your credit effectively.

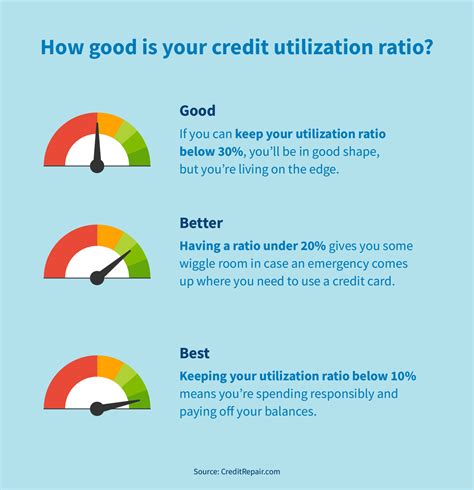

3. Ideal Utilization Range:

While there's no universally agreed-upon "ideal" percentage, experts generally recommend keeping your credit utilization below 30%. Aiming for under 10% is even better, as this significantly reduces your risk profile and potentially boosts your score. The lower your utilization, the better your creditworthiness appears to lenders.

4. Strategies for Improvement:

- Pay Down Existing Debt: The most straightforward way to lower your utilization is to pay down your outstanding balances. Prioritize high-interest debt to save money and improve your credit health more quickly.

- Increase Your Credit Limits: If you have a good payment history, you can request a credit limit increase from your credit card issuer. This will lower your utilization percentage without reducing your spending power. However, it’s crucial to maintain responsible spending habits even with a higher limit.

- Open a New Credit Card: Applying for a new credit card with a higher credit limit can also reduce your overall utilization rate. This is particularly effective if you have maxed out or near-maxed out existing cards. However, ensure you can manage the additional credit responsibly.

- Monitor Your Spending: Regularly track your spending and credit card balances. Set budgets and stick to them to avoid exceeding your credit limits.

- Avoid Closing Old Credit Cards: Closing old credit cards, even if you don't use them, can negatively impact your credit utilization ratio by reducing your total available credit.

5. Addressing Specific Scenarios:

- Unexpected Expenses: If unforeseen circumstances necessitate increased credit card usage, aim to pay down the balance as quickly as possible to minimize the impact on your credit score.

- Multiple Credit Cards: Managing multiple credit cards requires careful monitoring of each card's utilization. Strive to keep the utilization on each card low to avoid negatively impacting your overall score.

- Low Credit Limits: If you have low credit limits, work towards increasing them responsibly or explore options like secured credit cards to build your credit history and increase your available credit.

Closing Insights: Summarizing the Core Discussion

Maintaining a low credit utilization ratio is crucial for a healthy credit score. By understanding its impact and implementing the strategies outlined, you can significantly improve your financial standing and access better credit opportunities in the future.

Exploring the Connection Between Payment History and Credit Utilization

Payment history is another critical factor influencing your credit score. While credit utilization directly reflects your current debt management, your payment history reveals your long-term financial responsibility. The connection between these two is synergistic: consistent on-time payments, coupled with low credit utilization, paint a picture of a responsible borrower.

Key Factors to Consider:

- Roles and Real-World Examples: A consistent history of on-time payments mitigates the negative impact of slightly higher utilization. Conversely, even low utilization can be detrimental if accompanied by a history of late or missed payments.

- Risks and Mitigations: High utilization combined with late payments significantly damages your credit score. The solution lies in proactive debt management, budgeting, and prioritizing on-time payments.

- Impact and Implications: The combined effect of good payment history and low credit utilization significantly increases your chances of securing loans with favorable interest rates, better insurance premiums, and overall enhanced financial opportunities.

Conclusion: Reinforcing the Connection

The interplay between payment history and credit utilization is vital. They are intertwined aspects of responsible credit management. Prioritizing both aspects is essential for cultivating a strong credit profile.

Further Analysis: Examining Payment History in Greater Detail

Payment history encompasses all your past credit transactions, including loan repayments, credit card payments, and other forms of credit. Every on-time payment contributes positively to your score, while late or missed payments significantly detract. Lenders heavily weigh payment history because it directly demonstrates your ability to repay debts as agreed.

FAQ Section: Answering Common Questions About Credit Utilization

Q: What is the single most important factor affecting my credit score?

A: While several factors contribute, credit utilization is frequently cited as one of the most impactful.

Q: Can I improve my credit utilization quickly?

A: Yes, paying down existing debts and requesting credit limit increases are effective ways to quickly improve your utilization rate.

Q: Should I close unused credit cards?

A: Generally, it's better to keep unused cards open, as closing them can reduce your available credit and negatively affect your utilization ratio.

Q: What happens if my credit utilization is consistently high?

A: Consistently high credit utilization can severely damage your credit score, leading to higher interest rates and difficulty securing loans.

Practical Tips: Maximizing the Benefits of Credit Utilization Management

- Set a Budget: Carefully plan your spending to avoid accumulating excessive debt.

- Automate Payments: Set up automatic payments to ensure on-time payments consistently.

- Check Your Credit Report Regularly: Monitor your credit report for errors and track your credit utilization.

- Use Credit Cards Wisely: Utilize credit cards responsibly, paying off balances promptly.

- Seek Professional Advice: If you're struggling with debt management, consult a financial advisor.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding and managing credit utilization is fundamental to achieving optimal credit health. By diligently following the strategies outlined in this article, you can cultivate a strong credit profile, access better financial opportunities, and achieve your financial goals. Remember that credit utilization is just one piece of the puzzle. Consistent responsible financial behavior is the key to long-term credit success.

Latest Posts

Latest Posts

-

Advance Refunding Definition

Apr 30, 2025

-

Advance Premium Fund Definition

Apr 30, 2025

-

Advance Premium Definition

Apr 30, 2025

-

Advance Funded Pension Plan Definition

Apr 30, 2025

-

Advance Commitment Definition

Apr 30, 2025

Related Post

Thank you for visiting our website which covers about What Is An Ideal Credit Utilization Percentage . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.