What Is A Grace Period In Credit Card Terms

adminse

Apr 02, 2025 · 9 min read

Table of Contents

Understanding Grace Periods: Your Credit Card's Gift of Time

What if missing a single payment could dramatically alter your financial health? Understanding your credit card's grace period is crucial for maintaining a healthy credit score and avoiding unnecessary fees.

Editor’s Note: This article on credit card grace periods was published today, providing you with up-to-date information to help you manage your finances effectively.

Why Grace Periods Matter: Relevance, Practical Applications, and Industry Significance

A grace period, in the context of credit cards, is a crucial window of opportunity. It's the time between the end of your billing cycle and the due date of your payment. During this period, you can avoid paying interest on new purchases. This seemingly small detail can significantly impact your overall credit card costs, potentially saving you hundreds or even thousands of dollars over time. Understanding and utilizing your grace period is a fundamental aspect of responsible credit card management, impacting your credit score and financial well-being. The widespread use of credit cards across various income levels underlines the importance of comprehending this financial tool's nuances.

Overview: What This Article Covers

This article provides a comprehensive overview of credit card grace periods. We will explore the definition, how they work, factors affecting their length, the consequences of missing payments during the grace period, strategies to manage them effectively, and frequently asked questions. Readers will gain valuable insights into managing their credit card accounts responsibly and minimizing interest charges.

The Research and Effort Behind the Insights

This article is based on extensive research, including analysis of credit card agreements from major issuers, relevant financial regulations, and insights from consumer finance experts. We've examined various scenarios and case studies to illustrate the practical implications of grace periods and provide readers with actionable advice. Every claim is supported by verifiable information, ensuring accuracy and reliability.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of grace periods and their fundamental principles.

- Grace Period Mechanics: A detailed breakdown of how grace periods work in practice.

- Factors Influencing Grace Period Length: An exploration of variables that can affect the duration of your grace period.

- Consequences of Missing Payments: Understanding the penalties for late or missed payments during the grace period.

- Strategies for Effective Grace Period Management: Practical tips for maximizing the benefits of your grace period.

- Common Misconceptions: Addressing prevalent misunderstandings about grace periods.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding grace periods, let's delve into the specifics. We will examine how grace periods are calculated, the factors influencing their length, and the repercussions of failing to utilize them effectively.

Exploring the Key Aspects of Grace Periods

1. Definition and Core Concepts:

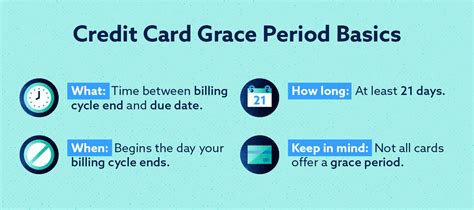

A grace period is the time you have after your billing cycle ends to pay your credit card balance in full without incurring interest charges on new purchases made during that cycle. It's essentially a "free" period offered by credit card issuers to encourage timely payments. Crucially, this grace period only applies to new purchases, not to existing balances carried over from previous months (which will continue to accrue interest).

2. How Grace Periods Work:

Each month, your credit card issuer generates a statement detailing your transactions, payments, and outstanding balance. The billing cycle ends on the statement closing date. The grace period begins the day after the statement closing date and ends on the payment due date. If you pay your entire statement balance (excluding any previous balances) by the due date, you avoid interest charges on the new purchases made during that billing cycle.

3. Factors Influencing Grace Period Length:

The length of your grace period isn't universally fixed. While most credit card issuers offer a grace period of 21 to 25 days, it can vary based on several factors:

- Issuer Policies: Different credit card companies have different policies regarding grace periods. Some may offer longer grace periods as an incentive, while others may have shorter ones.

- Account Type: The type of credit card you hold (e.g., rewards card, secured card) might influence the grace period offered.

- Payment History: Consistent on-time payments can sometimes influence the issuer's willingness to extend grace periods (though this is not always guaranteed and is rarely explicitly stated).

- Promotional Offers: Some promotional offers might temporarily alter your grace period, but this is typically temporary.

4. Consequences of Missing Payments:

Failing to pay your statement balance in full by the due date negates the grace period. This means that interest will be applied not only to your previous balance but also to the new purchases made during that billing cycle. Furthermore, late payment fees might be added to your account. Repeated late payments can severely damage your credit score, making it harder to obtain loans, rent an apartment, or even secure favorable insurance rates in the future.

5. Strategies for Effective Grace Period Management:

- Set Payment Reminders: Use online banking features, calendar reminders, or budgeting apps to set timely reminders for your credit card payment due date.

- Automate Payments: Consider setting up automatic payments to ensure on-time payments every month. This eliminates the risk of forgetting and helps maintain a positive payment history.

- Track Spending: Monitor your spending closely to avoid exceeding your credit limit and ensure you can comfortably pay your balance in full by the due date.

- Review Statements Carefully: Regularly review your credit card statements to verify the accuracy of charges and ensure you understand your balance and payment due date.

- Communicate with Your Issuer: If unforeseen circumstances prevent you from paying your balance on time, contact your credit card issuer immediately to discuss possible options, such as hardship programs or temporary payment extensions. Proactive communication is crucial.

Exploring the Connection Between Late Payments and Grace Periods

Late payments are the antithesis of effectively utilizing a grace period. A late payment completely nullifies the benefits of the grace period, resulting in accumulated interest on both existing and new balances. This seemingly small lapse can trigger a cascade of negative consequences.

Key Factors to Consider:

- Roles and Real-World Examples: A single late payment, even by a few days, can trigger late fees, negatively impacting your credit score. This can lead to higher interest rates on future loans and other financial products. Consider the example of someone relying on a good credit score to secure a mortgage; a series of missed credit card payments could jeopardize this crucial financial goal.

- Risks and Mitigations: The risk of late payments includes increased debt due to compounding interest, damaged credit score, and potential collection agency involvement. Mitigation strategies involve setting up automated payments, diligent tracking of spending, and proactive communication with the credit card issuer.

- Impact and Implications: The long-term impact of consistently missed payments can be substantial. It can lead to a vicious cycle of debt, higher interest rates, and difficulty accessing credit in the future. This can severely impact major life decisions like buying a house or a car.

Conclusion: Reinforcing the Connection

The relationship between timely payments and grace periods is paramount. Failing to meet the payment due date renders the grace period ineffective and sets in motion a chain reaction of negative consequences. By consistently paying on time, individuals harness the full potential of the grace period, saving money on interest and maintaining a healthy credit profile.

Further Analysis: Examining Late Payment Consequences in Greater Detail

The consequences of late payments extend beyond simple interest charges. Credit bureaus track late payments, and these are reflected in your credit report. A low credit score due to late payments can lead to:

- Higher Interest Rates: Lenders perceive individuals with poor credit scores as higher risk, leading to increased interest rates on loans, mortgages, and auto financing.

- Denied Credit Applications: Obtaining new credit cards or loans becomes significantly more difficult, if not impossible.

- Increased Insurance Premiums: Insurance companies often consider credit scores when setting premiums, so a low score can lead to higher costs for car, home, and other types of insurance.

- Difficulty Renting an Apartment: Landlords often use credit reports to assess the creditworthiness of prospective tenants. A poor credit history can make it challenging to secure rental housing.

FAQ Section: Answering Common Questions About Grace Periods

Q: What happens if I make a partial payment during the grace period? A: Making a partial payment will not preserve your grace period. To avoid interest charges on new purchases, you must pay your entire statement balance (excluding previous balances) by the due date.

Q: Does the grace period apply to cash advances? A: No, grace periods generally do not apply to cash advances. Interest accrues immediately on cash advances.

Q: What if my statement closing date and due date are close together? A: Even with a short grace period, you still need to pay the balance in full by the due date to avoid interest on new purchases.

Q: Can I lose my grace period permanently? A: While not permanently lost in most cases, repeatedly missing payments will effectively negate the benefit of your grace period as interest will accrue on new purchases until the balance is paid in full.

Practical Tips: Maximizing the Benefits of Grace Periods

- Understand Your Billing Cycle: Know when your billing cycle ends and your payment due date.

- Pay Attention to Due Dates: Make a note of these dates and set reminders to avoid late payments.

- Pay in Full: Always aim to pay your statement balance in full by the due date to benefit from the grace period.

- Budget Wisely: Track your spending and ensure you can afford to pay your balance in full each month.

- Utilize Autopay: Automate your payments to eliminate the risk of forgetting.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding and effectively managing your credit card grace period is a cornerstone of responsible financial management. By paying attention to due dates, budgeting carefully, and utilizing available payment tools, you can leverage the grace period to your advantage, saving money on interest and maintaining a healthy credit score. The seemingly small detail of a grace period holds significant long-term financial implications. Prioritize understanding its mechanics and utilizing it effectively to navigate the complexities of credit card management successfully.

Latest Posts

Latest Posts

-

What Is The Penalty For Late Payment Of Electricity Bill In Ap

Apr 04, 2025

-

What Is The Penalty For Late Payment Of Electricity Bill In Up

Apr 04, 2025

-

What Is The Penalty For Late Electricity Bill Payment

Apr 04, 2025

-

What Is The Grace Period For Electric Bill

Apr 04, 2025

-

Apa Itu Liquidity Pool

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about What Is A Grace Period In Credit Card Terms . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.