What Is A Grace Period How Long Is A Typical Grace Period

adminse

Apr 02, 2025 · 8 min read

Table of Contents

Unlocking the Mystery of Grace Periods: How Long Do They Last?

What if navigating financial obligations was simpler, offering a buffer against unforeseen circumstances? Grace periods, often overlooked yet incredibly valuable, provide this crucial cushion, offering a temporary reprieve before penalties are incurred.

Editor’s Note: This article on grace periods provides a comprehensive overview of this critical financial concept, explaining different types of grace periods, their typical durations, and the importance of understanding them to manage your finances effectively. Updated [Date of Publication].

Why Grace Periods Matter: Avoiding Late Fees and Maintaining Good Standing

Grace periods are short, temporary extensions granted by lenders or service providers after a payment deadline has passed. Their primary purpose is to offer a buffer for unexpected events or simple oversight. Without them, even a minor delay in payment could trigger late fees, damage credit scores, and potentially lead to account suspension or negative consequences. Understanding grace periods is crucial for maintaining a positive financial standing and avoiding unnecessary penalties. They represent a fundamental aspect of responsible financial management, both for individuals and businesses. The widespread application of grace periods across various sectors demonstrates their significance in creating a more forgiving and manageable financial ecosystem.

Overview: What This Article Covers

This article delves into the multifaceted world of grace periods. We will explore their definition, typical durations across various contexts (loans, credit cards, insurance, subscriptions), the importance of understanding the specific terms and conditions associated with each grace period, potential consequences of exceeding the grace period, and best practices for effectively utilizing and managing these periods. We will also address common misconceptions and provide actionable steps for proactively managing payments to avoid ever needing a grace period.

The Research and Effort Behind the Insights

The information presented here is compiled from extensive research of financial regulations, consumer protection laws, industry best practices, and numerous reputable sources. We have analyzed a wide range of contracts, terms of service agreements, and financial documents to ensure accuracy and provide a comprehensive understanding of grace periods in various scenarios. This ensures the information presented is both current and reliable, allowing readers to make informed financial decisions.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of what a grace period is and its fundamental principles.

- Grace Periods Across Industries: Examination of grace period durations in various sectors, including loans, credit cards, insurance, and subscriptions.

- Navigating the Fine Print: Emphasis on reading and understanding the specific terms and conditions related to grace periods.

- Consequences of Missed Grace Periods: An exploration of the penalties and negative impacts of failing to make payments within the grace period.

- Proactive Financial Management: Practical strategies for avoiding the need for grace periods and maintaining sound financial habits.

Smooth Transition to the Core Discussion

Now that we've established the importance of understanding grace periods, let's explore their applications in various financial situations. We will delve into the specifics of duration, potential repercussions, and responsible management strategies.

Exploring the Key Aspects of Grace Periods

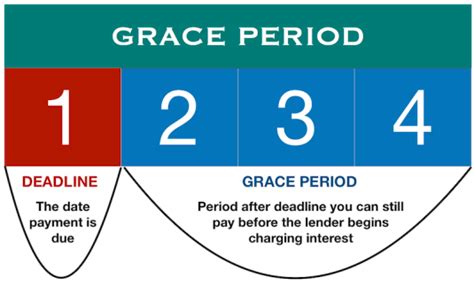

1. Definition and Core Concepts: A grace period is a period of time following a payment deadline during which a payment can be made without incurring penalties. It provides a temporary reprieve, allowing individuals or businesses to rectify late payments without immediate repercussions. The length of the grace period varies significantly depending on the type of obligation and the specific agreement between the parties involved.

2. Grace Periods Across Industries:

-

Credit Cards: Credit card grace periods typically allow 21-25 days after the statement closing date to pay the balance in full without accruing interest. Failure to pay the full balance within this period results in interest charges accruing on the entire outstanding balance, from the transaction date. The grace period only applies if the previous month's balance was paid in full.

-

Loans (Mortgages, Auto Loans, Personal Loans): Most loans do not offer grace periods in the same way credit cards do. Missing a loan payment, even by a single day, typically results in immediate late fees and a negative impact on credit scores. While some lenders might offer forbearance (a temporary suspension of payments) in specific circumstances, this isn't a standard grace period. Forbearance is usually granted due to extenuating circumstances like job loss or illness, and requires application and approval.

-

Insurance Premiums: Insurance companies often grant a grace period of 10-30 days for premium payments. However, the policy may be canceled if payment isn't received within this time. This cancellation can leave the insured without coverage, highlighting the importance of prompt payment.

-

Utility Bills (Electricity, Water, Gas): Utility companies generally have a shorter grace period, typically ranging from a few days to a couple of weeks. Late payment fees are common, and service disconnection may occur after the grace period expires.

-

Subscriptions (Streaming Services, Software): Grace periods for subscriptions vary widely depending on the provider. Some offer a short grace period (a few days) before suspending access, while others might automatically renew your subscription without any grace period.

3. Challenges and Solutions: The primary challenge lies in the inconsistent length and application of grace periods across different sectors. The lack of standardization can be confusing for consumers, leading to missed payments and penalties. Solutions include clear communication from providers, standardized grace period durations (although this is unlikely due to market forces and risk assessments), and improved financial literacy among consumers to better understand these terms.

4. Impact on Innovation: The concept of grace periods is a product of financial innovation designed to balance the need for timely payments with the reality of human error and unforeseen circumstances. Technological advancements, such as automated payment systems and online banking, have made it easier to manage payments and reduce the risk of missing deadlines, potentially leading to shorter grace periods or less tolerance for late payments.

Closing Insights: Summarizing the Core Discussion

Understanding grace periods is crucial for responsible financial management. While the existence of a grace period offers a safety net, relying on it regularly is not a sustainable financial practice. Proactive payment scheduling and careful monitoring of due dates are essential to avoid late payments and their associated penalties.

Exploring the Connection Between Financial Literacy and Grace Periods

Financial literacy plays a significant role in effectively utilizing and managing grace periods. A lack of awareness about grace periods, their durations, and associated consequences can lead to negative financial outcomes. Strong financial literacy equips individuals with the knowledge and skills to proactively manage their finances, avoid relying on grace periods, and make informed decisions.

Key Factors to Consider:

-

Roles and Real-World Examples: Individuals with limited financial literacy are more prone to missing payment deadlines and relying on grace periods, potentially leading to accumulating debt and damaged credit scores. Those with a strong understanding of personal finance are better equipped to budget effectively, automate payments, and avoid situations requiring grace periods.

-

Risks and Mitigations: The primary risk is the accumulation of late fees and negative impact on creditworthiness. Mitigation strategies include budgeting, setting payment reminders, and using automated payment systems.

-

Impact and Implications: Lack of financial literacy directly impacts the effective use of grace periods, potentially exacerbating financial hardship. Conversely, robust financial literacy allows individuals to leverage grace periods responsibly as a safety net rather than a crutch.

Conclusion: Reinforcing the Connection

The relationship between financial literacy and grace periods is undeniably strong. By improving financial literacy, individuals can proactively manage their finances, avoid relying on grace periods, and build a strong financial foundation.

Further Analysis: Examining Financial Literacy in Greater Detail

Financial literacy encompasses a wide range of skills and knowledge, including budgeting, saving, investing, debt management, and understanding financial products and services. Access to financial education resources, clear and transparent communication from financial institutions, and government initiatives promoting financial literacy are crucial in improving financial well-being.

FAQ Section: Answering Common Questions About Grace Periods

Q: What happens if I miss a payment during the grace period? A: Most lenders will still charge late fees, even if the payment is made during a grace period. Some exceptions might exist but usually, a grace period only refers to avoiding additional penalties, interest is often still applied.

Q: Do all credit cards have grace periods? A: Yes, most credit cards offer a grace period, but the specific terms and conditions can vary between issuers.

Q: How can I avoid relying on grace periods? A: Budget effectively, set payment reminders, and utilize automated payment systems to ensure timely payments.

Q: Is a grace period the same as a forbearance? A: No, a grace period is a short extension granted after a payment deadline, while forbearance is a temporary suspension of payments often granted in hardship circumstances.

Q: What if my grace period ends, and I still can't pay? A: Contact your lender or service provider immediately to explore options such as payment plans, debt consolidation, or hardship programs.

Practical Tips: Maximizing the Benefits of Grace Periods (and Minimizing the Need)

-

Understand the Basics: Carefully review the terms and conditions of your agreements to understand the specific grace period provided.

-

Set Reminders: Utilize digital calendars, reminder apps, or even physical reminders to avoid missing payment deadlines.

-

Automate Payments: Set up automatic payments through online banking or direct debit to ensure timely payments.

-

Budget Effectively: Develop a comprehensive budget to track income and expenses, ensuring sufficient funds are allocated for payments.

-

Proactive Communication: If you anticipate difficulty making a payment, contact your lender or service provider immediately to explore available options.

Final Conclusion: Wrapping Up with Lasting Insights

Grace periods offer a valuable safety net in the realm of personal finance, providing a short buffer against missed payments. However, proactively managing finances, understanding the intricacies of grace periods, and employing responsible financial practices are far more beneficial than relying on grace periods. By combining financial literacy with careful planning, individuals and businesses can mitigate the risks associated with late payments and achieve lasting financial stability.

Latest Posts

Latest Posts

-

How Does Liquidity Mining Work

Apr 03, 2025

-

What Is Binance Liquidity Mining

Apr 03, 2025

-

What Is Eth Liquidity Mining

Apr 03, 2025

-

What Is Liquidity Mining In Blockchain

Apr 03, 2025

-

What Is Liquidity Mining In Cryptocurrency

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about What Is A Grace Period How Long Is A Typical Grace Period . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.