What Is A Credit Card's Grace Period ( 1 Point

adminse

Apr 02, 2025 · 8 min read

Table of Contents

Understanding Your Credit Card's Grace Period: A Comprehensive Guide

What if maximizing your financial flexibility hinges on understanding your credit card's grace period? This often-overlooked feature can significantly impact your credit score and overall financial health.

Editor's Note: This article on credit card grace periods was published today, providing readers with up-to-date information and actionable insights to manage their credit effectively.

Why Your Credit Card's Grace Period Matters:

Understanding your credit card's grace period is crucial for responsible credit card management. It directly affects your interest payments, your credit score, and your overall financial well-being. Failing to understand this period can lead to unnecessary interest charges and potentially damage your creditworthiness. This period allows you a window to pay your balance in full without accruing interest, a significant benefit that can save you substantial amounts of money over time. Knowing how it works can empower you to make informed decisions about your spending and debt management strategies. The grace period is a key component of responsible credit card usage and is often a determining factor in choosing the right card for your individual financial needs.

Overview: What This Article Covers

This article provides a comprehensive overview of credit card grace periods. We will delve into the definition, calculation, factors that affect it, the consequences of missing the grace period, strategies for utilizing it effectively, and common misconceptions surrounding this crucial aspect of credit card usage. We will also discuss how the grace period interacts with different types of credit card transactions, such as purchases, balance transfers, and cash advances. Finally, we'll address frequently asked questions and provide practical tips to maximize the benefits of your grace period.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing upon information from leading financial institutions, consumer protection agencies, and reputable financial websites. The information presented is backed by credible sources and aims to provide readers with accurate and actionable advice. A structured approach was employed to ensure clarity and ease of understanding, focusing on delivering practical insights relevant to everyday credit card users.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of what constitutes a credit card grace period and its fundamental principles.

- Grace Period Calculation: Understanding how the grace period is calculated and the factors that influence its length.

- Impact of Late Payments: The consequences of failing to pay your balance within the grace period.

- Strategies for Maximizing the Grace Period: Practical tips for utilizing the grace period to your advantage.

- Common Misconceptions: Addressing common misunderstandings surrounding credit card grace periods.

Smooth Transition to the Core Discussion:

With a foundational understanding of the importance of the grace period, let's delve into the specifics of this critical element of credit card management.

Exploring the Key Aspects of a Credit Card Grace Period:

1. Definition and Core Concepts:

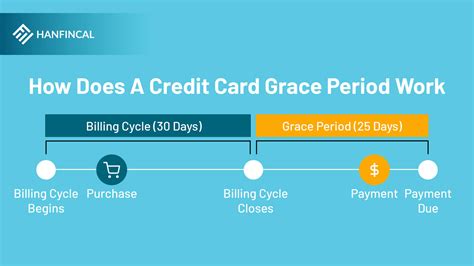

A credit card grace period is the time frame between the end of your billing cycle and the due date of your payment. During this period, you can pay your statement balance in full without incurring any interest charges on purchases made during the previous billing cycle. Crucially, this only applies to purchases; other transactions like cash advances or balance transfers typically accrue interest from the transaction date.

2. Grace Period Calculation:

The grace period isn't a fixed number of days; it varies depending on the card issuer and even your individual account. It's usually between 21 and 25 days, but it's essential to check your card's terms and conditions or your monthly statement to know your exact grace period length. The calculation starts from the end of your billing cycle, which is the date your statement is generated, summarizing the transactions from the previous month. The due date is then calculated by adding the length of your grace period to the end of your billing cycle.

3. Applications Across Industries:

The concept of a grace period is fairly standardized across the credit card industry, although the specific length might differ. There isn't significant variation in how this works across different financial institutions, with the core principle remaining consistent – a period to pay in full without accruing interest on purchases.

4. Challenges and Solutions:

The primary challenge lies in understanding the nuances of the grace period and its limitations. Many cardholders are unaware of the specific length of their grace period or that it doesn't apply to all transactions. The solution is simple: actively read your monthly statements and the terms and conditions of your card agreement to fully grasp how the grace period functions in your specific situation.

5. Impact on Credit Scores:

While paying your balance in full within the grace period doesn't directly impact your credit score, it indirectly benefits it immensely. By avoiding interest charges, you reduce your debt-to-credit ratio and maintain a better credit utilization rate – both critical factors in determining your creditworthiness. Consistent on-time payments, facilitated by utilizing the grace period effectively, positively influence your credit score over time.

Closing Insights: Summarizing the Core Discussion:

Understanding and utilizing your credit card's grace period is a foundational element of responsible credit card management. It allows cardholders to avoid accumulating debt and save significantly on interest charges. By staying informed about your billing cycle and due dates, you can harness the power of the grace period to maintain a healthy financial standing.

Exploring the Connection Between Credit Utilization and the Grace Period:

Credit utilization is the percentage of your available credit that you're currently using. It significantly impacts your credit score. While the grace period itself doesn't directly influence your credit utilization, how you utilize it significantly affects your credit utilization. Paying your balance in full before the due date, thereby utilizing the grace period, keeps your credit utilization low. Conversely, carrying a balance into the next billing cycle increases your credit utilization, potentially harming your credit score.

Key Factors to Consider:

-

Roles and Real-World Examples: A cardholder with a $1000 credit limit who spends $500 in a billing cycle and pays it off within the grace period maintains a 50% credit utilization rate. However, if they only pay $250, their credit utilization increases to 75%, negatively impacting their credit score.

-

Risks and Mitigations: The risk of neglecting your grace period is incurring interest charges, increasing your debt and potentially damaging your credit score. Mitigation involves setting reminders for your due dates and proactively managing your spending to ensure you can pay your balance in full within the grace period.

-

Impact and Implications: The long-term impact of consistently utilizing the grace period is a healthy credit score, lower debt burden, and enhanced financial flexibility. Conversely, ignoring the grace period leads to higher interest costs, greater debt, and a potential decline in creditworthiness.

Conclusion: Reinforcing the Connection:

The interplay between credit utilization and the grace period is clear. Effective use of the grace period, coupled with responsible spending, maintains a low credit utilization rate, leading to improved credit health. Ignoring it can have detrimental long-term effects on your financial well-being.

Further Analysis: Examining Interest Calculation in Greater Detail:

Interest is calculated on your outstanding balance after the grace period ends. If you carry a balance into the next billing cycle, interest is charged on that amount. The interest rate applied is your annual percentage rate (APR), which is typically stated in your cardholder agreement. The daily interest rate is calculated by dividing the APR by 365. The daily interest is then multiplied by your outstanding balance for each day the balance remains unpaid.

FAQ Section: Answering Common Questions About Credit Card Grace Periods:

-

Q: What happens if I miss my grace period? A: You'll start accruing interest on your purchases from the end of your billing cycle.

-

Q: Does the grace period apply to cash advances? A: No, cash advances typically accrue interest from the transaction date.

-

Q: Can my grace period change? A: Yes, it can change based on your account activity or the card issuer's policies. Always refer to your statement or terms and conditions.

-

Q: What if my payment is received after the due date, but still within the grace period? A: While some issuers may still waive interest if the payment is received close to the due date, this is not guaranteed. It's always best to pay on time.

Practical Tips: Maximizing the Benefits of Your Credit Card Grace Period:

-

Understand the Basics: Know your billing cycle end date and grace period length.

-

Track Your Spending: Monitor your spending closely to ensure you can pay your balance in full.

-

Set Reminders: Use calendar alerts or reminders to ensure timely payments.

-

Pay Online: Online payments typically offer confirmation and allow you to track your payment status.

-

Review Your Statement: Check your statement carefully to identify any errors or unexpected charges.

Final Conclusion: Wrapping Up with Lasting Insights:

The credit card grace period is a valuable tool for responsible credit card users. By understanding its mechanics and utilizing it effectively, cardholders can significantly reduce their debt burden, save money on interest, and improve their creditworthiness. Proactive management of spending habits and timely payments are key to maximizing the benefits of this often-overlooked feature. Prioritizing financial literacy and understanding your credit card terms and conditions remain vital for long-term financial health and stability.

Latest Posts

Latest Posts

-

What Is The Minimum Payment For A 1000 Credit Card

Apr 04, 2025

-

What Is The Minimum Payment For A Discover Credit Card

Apr 04, 2025

-

What Is The Minimum Salary For A Credit Card In Kuwait

Apr 04, 2025

-

What Is The Minimum Amount For A Credit Card

Apr 04, 2025

-

What Is The Minimum Salary For A Credit Card In Qatar

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about What Is A Credit Card's Grace Period ( 1 Point . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.