What Does Grace Period Mean In Finance

adminse

Apr 02, 2025 · 8 min read

Table of Contents

Understanding Grace Periods in Finance: A Comprehensive Guide

What if navigating the complexities of personal and business finance was significantly easier, thanks to a clear understanding of grace periods? Grace periods, often overlooked yet incredibly impactful, offer crucial breathing room in various financial situations, influencing everything from loan repayments to insurance coverage.

Editor’s Note: This article on grace periods in finance was published today, providing readers with up-to-date information and actionable insights into this often-misunderstood aspect of financial management.

Why Grace Periods Matter: Relevance, Practical Applications, and Industry Significance

Grace periods are vital safety nets within the financial ecosystem. They provide a temporary reprieve from penalties or negative consequences for missed payments or deadlines. Their relevance spans various sectors, impacting individuals, businesses, and institutions. From avoiding late fees on credit card payments to maintaining insurance coverage despite a missed premium, understanding and utilizing grace periods can significantly improve financial well-being and mitigate potential risks. The implications extend to better credit scores, smoother business operations, and improved overall financial stability. This understanding is crucial for informed decision-making across personal finance, business operations, and risk management.

Overview: What This Article Covers

This article will comprehensively explore grace periods in finance, examining their definitions, applications across different financial products, associated benefits and drawbacks, and potential implications for both individuals and businesses. We will analyze various scenarios, including credit cards, loans, insurance policies, and subscription services, clarifying the specific terms and conditions related to each. Finally, the article will provide actionable strategies for leveraging grace periods effectively and mitigating potential risks associated with relying on them.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon various financial resources, regulatory documents, and industry best practices. Information has been compiled from reputable sources, including consumer financial protection bureaus, industry reports, and financial institution websites. Each point is supported by evidence, ensuring that readers receive accurate and trustworthy information for informed financial decision-making.

Key Takeaways:

- Definition and Core Concepts: A precise definition of grace periods and their fundamental principles.

- Applications Across Industries: Exploring the various financial products that offer grace periods.

- Benefits and Drawbacks: Analyzing the advantages and disadvantages of relying on grace periods.

- Practical Strategies: Providing actionable steps to effectively utilize and manage grace periods.

- Legal and Regulatory Aspects: Highlighting the legal frameworks governing grace periods.

Smooth Transition to the Core Discussion:

With a clear understanding of the importance of grace periods, let's delve deeper into their nuances, exploring their applications across diverse financial sectors and strategies for effective management.

Exploring the Key Aspects of Grace Periods

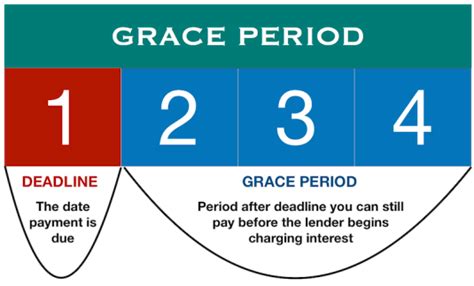

1. Definition and Core Concepts:

A grace period, in the financial context, refers to a specified timeframe after a payment due date during which a payment can be made without incurring penalties. This period offers a buffer, allowing individuals or businesses to address unforeseen circumstances or simply overcome temporary cash flow issues. The duration of the grace period varies significantly depending on the type of financial product and the terms and conditions set by the provider.

2. Applications Across Industries:

-

Credit Cards: Most credit card companies offer a grace period, typically 21-25 days, during which you can pay your statement balance in full without incurring interest charges. However, this grace period only applies if the previous balance was paid in full by the due date. Any outstanding balance from the previous month will accrue interest from the transaction date.

-

Loans: Some loan types, like personal loans or student loans, might offer grace periods, particularly during periods of study or immediately following graduation. These grace periods usually postpone the commencement of repayment for a defined period. However, interest might still accrue during the grace period, meaning borrowers will owe a larger amount once repayments begin.

-

Insurance Policies: Grace periods are common in insurance policies, providing a short window to pay overdue premiums without causing the policy to lapse. The length of this period varies by insurer and policy type. Missing the grace period often leads to policy cancellation and potential loss of coverage.

-

Subscription Services: Many subscription services offer a grace period after cancellation, allowing continued access for a short time. This gives subscribers time to download data, transfer files, or access content before complete service termination.

3. Challenges and Solutions:

-

Over-Reliance: Over-reliance on grace periods can become a dangerous habit, delaying necessary financial responsibility. It's crucial to manage finances proactively to avoid repeatedly relying on grace periods.

-

Interest Accrual: During grace periods, interest might still accrue on outstanding balances for loans and credit cards, increasing the overall cost. This needs careful consideration.

-

Inconsistent Policies: Grace period policies differ greatly between financial institutions and product types. Thoroughly understanding the specifics of each agreement is vital to avoid unexpected penalties.

4. Impact on Financial Well-being:

Grace periods positively influence credit scores by allowing timely payments, preventing late payment marks that negatively impact credit ratings. They also contribute to better financial management by providing flexibility and time to address unexpected expenses. However, consistent reliance on grace periods can mask underlying financial instability.

Closing Insights: Summarizing the Core Discussion

Grace periods represent an essential aspect of modern financial systems, offering a critical buffer against unexpected circumstances. However, a clear understanding of their limitations and a proactive approach to financial management are crucial to avoid over-reliance and its potential consequences.

Exploring the Connection Between Credit Scores and Grace Periods

The relationship between credit scores and grace periods is significant. Effectively utilizing grace periods contributes to a positive credit history. Paying balances within the grace period prevents late payment marks, improving the credit score and maintaining financial credibility. Conversely, consistent reliance on grace periods, particularly when coupled with consistently high credit utilization, might indicate poor financial management, potentially lowering the credit score.

Key Factors to Consider:

-

Roles and Real-World Examples: Consistent on-time payments within grace periods demonstrate responsible financial behavior, leading to better credit scores and improved access to financial products. Conversely, exceeding grace periods consistently negatively affects credit history.

-

Risks and Mitigations: Over-reliance on grace periods masks potential financial problems. Proactive budgeting and financial planning are crucial to avoid consistent late payments.

-

Impact and Implications: A good credit score unlocks better interest rates on loans, easier access to credit, and favorable insurance premiums. Conversely, a damaged credit score limits these opportunities.

Conclusion: Reinforcing the Connection

The interplay between credit scores and grace periods underscores the importance of understanding and using these periods responsibly. By understanding the implications of each decision, individuals can build and maintain a healthy credit profile.

Further Analysis: Examining Late Payment Fees in Greater Detail

Late payment fees are a direct consequence of missing the grace period for various financial products. These fees vary significantly based on the type of financial product, the provider, and the amount overdue. Understanding these fees is crucial for budgeting and responsible financial management. These fees can significantly add to the overall cost, potentially escalating financial difficulties.

FAQ Section: Answering Common Questions About Grace Periods

Q: What happens if I miss the grace period on my credit card?

A: If you miss the grace period on your credit card, interest will be charged on your outstanding balance from the transaction date, increasing your total cost. Late payment fees might also apply.

Q: Are grace periods the same for all types of loans?

A: No, grace periods vary significantly depending on the loan type, lender, and the terms of the loan agreement. Some loans might not offer grace periods at all.

Q: Can I rely on grace periods to manage my finances?

A: While grace periods offer a temporary buffer, relying on them consistently is not a sustainable financial strategy. Proactive budgeting and financial planning are crucial for long-term financial stability.

Q: What happens if I miss the grace period on my insurance policy?

A: Missing the grace period on your insurance policy usually leads to policy cancellation, leaving you without coverage.

Practical Tips: Maximizing the Benefits of Grace Periods

- Set up automatic payments: Automate payments to avoid missing due dates.

- Understand the terms: Carefully review the terms and conditions of each financial product to understand the specific grace period offered.

- Budget effectively: Create a realistic budget to ensure timely payments and avoid relying on grace periods excessively.

- Track due dates: Use calendars or reminders to track important payment due dates.

- Communicate with lenders: If facing financial difficulties, contact your lender immediately to discuss payment options.

Final Conclusion: Wrapping Up with Lasting Insights

Grace periods provide a vital safety net within the complex world of finance. Understanding their intricacies, applications, and potential impacts is essential for responsible financial management. By leveraging grace periods strategically and practicing proactive financial planning, individuals and businesses can navigate financial challenges more effectively and build a strong financial foundation. The key lies in responsible utilization and a commitment to long-term financial health rather than relying on grace periods as a primary financial management strategy.

Latest Posts

Latest Posts

-

How To Calculate Late Fees On Taxes

Apr 03, 2025

-

How To Calculate Late Fee Interest

Apr 03, 2025

-

How To See Late Fee In Gst Portal

Apr 03, 2025

-

How To Check Late Fees On Registration

Apr 03, 2025

-

How To Calculate Late Fee In Lic Premium

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about What Does Grace Period Mean In Finance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.