What Credit Score Do You Need To Refinance Student Loans

adminse

Mar 28, 2025 · 8 min read

Table of Contents

What Credit Score Do You Need to Refinance Student Loans? Unlocking Lower Rates and Better Terms

What if securing a lower interest rate on your student loans was easier than you think? A strategic approach to refinancing, focused on building and maintaining a strong credit score, can significantly improve your chances of securing favorable terms.

Editor’s Note: This article on student loan refinancing and credit scores was published today, providing readers with the most up-to-date information and insights available. The information provided here is for general guidance only and does not constitute financial advice. Consult with a financial advisor before making any decisions regarding your student loans.

Why Your Credit Score Matters for Student Loan Refinancing

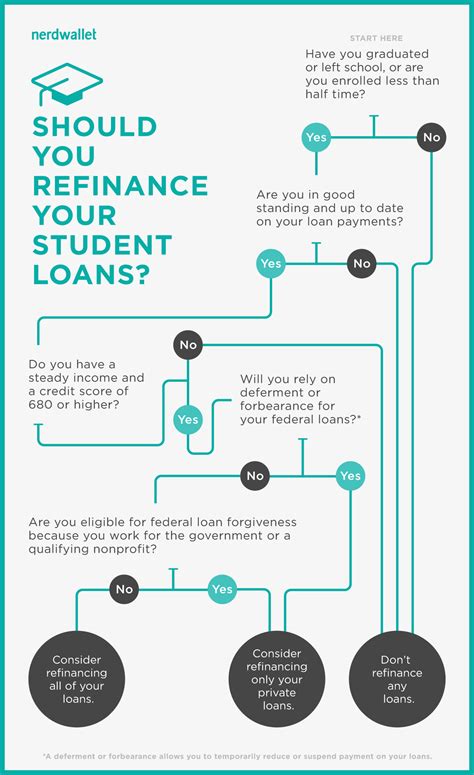

Student loan refinancing allows borrowers to consolidate multiple loans into a single loan with potentially better terms, such as a lower interest rate, a shorter repayment period, or a different repayment plan. Lenders assess applicants based on several factors, but your credit score plays a pivotal role in determining your eligibility and the interest rate you'll receive. A higher credit score signifies lower risk to the lender, making you a more attractive candidate for favorable loan terms. Conversely, a low credit score can lead to rejection or significantly higher interest rates, negating the potential benefits of refinancing.

Overview: What This Article Covers

This article provides a comprehensive guide to understanding the relationship between your credit score and student loan refinancing. We'll explore the importance of credit scores, the typical credit score requirements of various lenders, strategies to improve your credit score, and additional factors lenders consider beyond your credit score. Readers will gain actionable insights to increase their chances of securing a successful student loan refinance.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon data from reputable sources like Experian, Equifax, and TransUnion, as well as analyzing terms and conditions from leading student loan refinance lenders. We have also reviewed numerous financial articles and publications to ensure the information is accurate, current, and reflective of industry best practices. Every claim and suggestion is supported by evidence, aiming to provide readers with trustworthy and actionable information.

Key Takeaways:

- Credit Score Requirements Vary: There's no single magic number. Lenders have different minimum credit score requirements, ranging from the mid-600s to the mid-700s or even higher.

- Higher Score = Better Rates: Generally, a higher credit score translates to a lower interest rate and more favorable loan terms.

- Other Factors Matter: While credit score is crucial, lenders also consider income, debt-to-income ratio, and loan amount.

- Improving Your Score is Possible: Even with a lower credit score, proactive steps can improve your financial standing and increase your chances of approval.

Smooth Transition to the Core Discussion:

Now that we've established the importance of credit scores in student loan refinancing, let's delve into the specifics. We will examine the credit score requirements of different lenders, explore strategies for improving your creditworthiness, and discuss other crucial factors lenders consider.

Exploring the Key Aspects of Student Loan Refinancing and Credit Scores

1. Definition and Core Concepts:

A credit score is a numerical representation of your creditworthiness, based on your credit history. It's calculated by credit bureaus using various factors, including payment history, amounts owed, length of credit history, credit mix, and new credit. Student loan refinancing involves obtaining a new loan to pay off existing student loans, typically at a lower interest rate or with more favorable repayment terms. The lower interest rate is contingent on your creditworthiness, represented largely by your credit score.

2. Credit Score Requirements Across Lenders:

There's no universal credit score requirement for student loan refinancing. Different lenders have different criteria, often ranging from a minimum score of 660 to 700 or even higher. Some lenders may be more lenient with borrowers who have other strong financial indicators, while others might prioritize a higher credit score. It's crucial to check the specific requirements of each lender before applying. Here's a general guideline (remember, this is a generalization and can change):

- 660-699: May qualify for refinancing, but likely with a higher interest rate.

- 700-759: Generally qualifies for refinancing with competitive interest rates.

- 760 and above: Often qualifies for the best interest rates and loan terms.

3. Challenges and Solutions:

A low credit score presents a significant challenge for student loan refinancing. However, it's not insurmountable. Solutions include:

- Improving Credit Score: Addressing issues contributing to a low score, such as late payments or high credit utilization, can improve your chances.

- Finding Lenders with Lower Requirements: Some lenders may be more willing to work with borrowers who have lower credit scores.

- Co-signer: A co-signer with a strong credit history can significantly increase your approval chances.

4. Impact on Interest Rates and Loan Terms:

Your credit score directly impacts the interest rate you'll receive on a refinanced student loan. A higher credit score generally translates to a lower interest rate, resulting in significant savings over the life of the loan. It can also influence the loan terms, such as the repayment period and the availability of different repayment options.

Closing Insights: Summarizing the Core Discussion

A strong credit score is undeniably vital for securing favorable terms when refinancing student loans. While lenders consider other factors, your creditworthiness is a cornerstone of their assessment. Understanding the credit score requirements of different lenders and taking proactive steps to improve your credit score can significantly increase your chances of success.

Exploring the Connection Between Debt-to-Income Ratio and Student Loan Refinancing

The relationship between your debt-to-income ratio (DTI) and your ability to refinance student loans is significant. DTI is the percentage of your gross monthly income that goes towards paying your debts. Lenders use DTI to gauge your ability to manage additional debt. A high DTI can indicate that you're already struggling to manage your existing debts, making you a higher risk for lenders. A low DTI, on the other hand, suggests that you have ample income available to handle additional debt obligations.

Key Factors to Consider:

Roles and Real-World Examples:

A borrower with a high DTI might find it challenging to refinance their student loans, even with a good credit score. Lenders might perceive them as a higher risk, potentially leading to rejection or offering less favorable terms. For example, someone with a DTI of 50% might struggle to refinance, while someone with a DTI of 30% might have a much higher chance of approval.

Risks and Mitigations:

High DTI can lead to loan rejection or higher interest rates. To mitigate this, borrowers can try to lower their DTI by paying down high-interest debts, increasing their income, or consolidating debts with a lower interest rate.

Impact and Implications:

A lower DTI strengthens the application significantly. This improves the likelihood of approval and the possibility of securing a better interest rate. Ignoring DTI can lead to missed opportunities for substantial savings through refinancing.

Conclusion: Reinforcing the Connection

The DTI, alongside credit score, forms a critical evaluation point for lenders. Reducing your DTI through responsible debt management can significantly improve your chances of successfully refinancing your student loans and securing better loan terms.

Further Analysis: Examining Income in Greater Detail

Income is another critical factor lenders evaluate when reviewing student loan refinance applications. Your income demonstrates your ability to make consistent monthly payments on the refinanced loan. A stable and sufficient income significantly enhances your chances of approval.

FAQ Section: Answering Common Questions About Student Loan Refinancing

Q: What is a good credit score for refinancing student loans?

A: While lenders vary, a credit score of 700 or higher is generally considered favorable for obtaining competitive interest rates. Scores in the 660-699 range might qualify, but likely at higher rates.

Q: What if my credit score is below 660?

A: If your score is below 660, consider working on improving it before applying. You could also explore options like finding a co-signer or looking for lenders with more lenient requirements.

Q: What other factors besides credit score do lenders consider?

A: Lenders also assess income, debt-to-income ratio, loan amount, and the type of student loans you're refinancing.

Q: How long does the refinancing process typically take?

A: The timeframe varies by lender, but generally ranges from a few weeks to a few months.

Q: Are there any fees associated with refinancing student loans?

A: Some lenders charge origination fees or other processing fees. Be sure to review the terms and conditions carefully.

Practical Tips: Maximizing the Benefits of Student Loan Refinancing

- Check Your Credit Report: Review your credit reports for errors and address any negative marks.

- Improve Your Credit Score: Pay down debt, make timely payments, and keep credit utilization low.

- Shop Around: Compare offers from different lenders to find the best rates and terms.

- Understand the Terms: Carefully review the loan agreement before signing.

- Consider a Co-signer: If your credit score is low, a co-signer with a good credit history can help.

Final Conclusion: Wrapping Up with Lasting Insights

Refinancing student loans can offer significant financial benefits, but success hinges on understanding the lender’s requirements, particularly your credit score and DTI. By proactively addressing these factors and employing sound financial strategies, borrowers can position themselves for approval and secure better terms, leading to substantial long-term savings. Remember, a well-planned approach, focusing on credit improvement and responsible debt management, can open doors to more favorable refinancing opportunities.

Latest Posts

Latest Posts

-

Interest Rate Risk Definition And Impact On Bond Prices

Apr 24, 2025

-

Interest Rate Reduction Refinance Loan Irrrl Definition

Apr 24, 2025

-

Interest Rate Parity Irp Definition Formula And Example

Apr 24, 2025

-

Interest Rate Options Definition How They Work And Example

Apr 24, 2025

-

Interest Rate Gap Definition What It Measures And Calculation

Apr 24, 2025

Related Post

Thank you for visiting our website which covers about What Credit Score Do You Need To Refinance Student Loans . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.