What Credit Score Do You Need To Cosign For A Student Loan

adminse

Mar 28, 2025 · 7 min read

Table of Contents

What Credit Score Do You Need to Cosign for a Student Loan? Unlocking Financial Aid Through Co-signing

What if securing a student loan for a loved one hinged on understanding the intricacies of co-signing? Co-signing significantly impacts loan approval, offering crucial support but demanding careful consideration of credit implications.

Editor’s Note: This article on the credit score requirements for co-signing a student loan was published today, providing up-to-the-minute information and insights for prospective co-signers. We've compiled essential information to help you navigate this significant financial decision.

Why Co-signing a Student Loan Matters: Relevance, Practical Applications, and Financial Implications

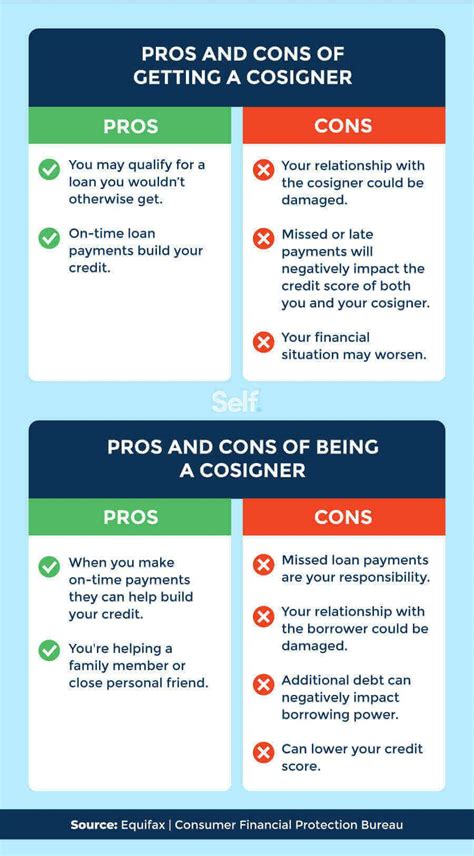

Co-signing a student loan is a significant financial undertaking. It carries substantial responsibility and directly impacts the co-signer's creditworthiness. Understanding the credit score implications and the process itself is crucial for both the student borrower and the co-signer. This act of support provides access to funding for education, a critical stepping stone for many students who might otherwise be ineligible for loans due to limited or no credit history. However, a co-signer assumes full responsibility for the loan's repayment should the student borrower default.

Overview: What This Article Covers

This article provides a comprehensive guide to understanding the credit score requirements for co-signing a student loan. We will delve into the lender's perspective, explore the various types of student loans, examine the impact on credit scores, and offer practical advice for both potential co-signers and student borrowers. We will also discuss alternative strategies and highlight potential pitfalls to avoid.

The Research and Effort Behind the Insights

This article draws upon extensive research, including analysis of lending practices from various financial institutions, reviews of numerous credit reporting agencies' guidelines, and examination of consumer financial protection regulations. We have synthesized this information to provide a clear, accurate, and actionable understanding of the topic.

Key Takeaways:

- Lender Variability: There's no single magic number for a co-signer's credit score. Requirements vary significantly across lenders.

- Credit Score Importance: A higher credit score substantially increases the chances of loan approval.

- Credit History Length: The length of established credit history is often as important as the score itself.

- Debt-to-Income Ratio: A low debt-to-income ratio enhances approval prospects.

- Co-signer Release: Some loans offer options for co-signer release after a period of on-time payments.

Smooth Transition to the Core Discussion

Now that we understand the importance of co-signing and the scope of this article, let's explore the key aspects of credit scores and their influence on student loan co-signership.

Exploring the Key Aspects of Co-signing a Student Loan

1. Definition and Core Concepts:

Co-signing a student loan means agreeing to be legally responsible for repaying the loan if the primary borrower (the student) fails to do so. This involves signing the loan documents alongside the student, essentially becoming a guarantor. Lenders view co-signers as mitigating the risk associated with lending to someone with a limited or poor credit history.

2. Applications Across Industries:

Co-signing applies primarily to private student loans, not federal student loans. Federal loans have different eligibility requirements and do not typically involve co-signers. Private lenders, however, often require a co-signer to reduce their risk. The application process involves both the student and co-signer submitting their financial information.

3. Challenges and Solutions:

The primary challenge is the potential financial burden on the co-signer if the student defaults. Solutions include careful consideration of the student's repayment ability, choosing a loan with favorable terms, and exploring co-signer release options.

4. Impact on Innovation:

While not directly related to technological innovation, the co-signing process has adapted to online applications and streamlined processes. However, the core principles of risk assessment and financial responsibility remain unchanged.

Closing Insights: Summarizing the Core Discussion

Co-signing a student loan is a significant decision. It offers a pathway to education but necessitates a thorough understanding of the associated financial responsibilities. The lack of a universally applicable credit score threshold highlights the nuanced nature of lender assessment.

Exploring the Connection Between Credit Score and Student Loan Co-signing

The relationship between a co-signer's credit score and student loan approval is crucial. Lenders use credit scores as a primary indicator of creditworthiness and repayment ability. A higher credit score significantly improves the chances of the loan application being approved. This is because a strong credit history suggests a lower risk of default for the lender.

Key Factors to Consider:

Roles and Real-World Examples: A co-signer with a credit score above 700 generally has a much higher chance of approval than one with a score below 600. For example, a parent with an excellent credit history may co-sign for their child's loan, significantly improving the chances of approval and potentially securing better interest rates.

Risks and Mitigations: The primary risk is the co-signer’s financial liability if the borrower defaults. Mitigating this risk involves careful evaluation of the student’s academic progress, financial situation, and future employment prospects. Thoroughly reviewing the loan terms and understanding the repayment schedule is also vital.

Impact and Implications: A co-signer’s credit score can impact not only the loan's approval but also the interest rate offered. A higher credit score may lead to a lower interest rate, saving the borrower significant money over the life of the loan. Conversely, a poor credit score may lead to rejection or higher interest rates.

Conclusion: Reinforcing the Connection

The connection between credit score and co-signing is undeniable. A strong credit score acts as a powerful endorsement of the borrower's creditworthiness, influencing loan approval and potentially securing more favorable terms.

Further Analysis: Examining Credit Reporting Agencies in Greater Detail

Three major credit reporting agencies—Equifax, Experian, and TransUnion—compile credit reports used by lenders. These reports contain various factors that influence credit scores, including payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders use these scores to assess risk and make lending decisions. Each agency has its own scoring model, but all consider similar factors.

FAQ Section: Answering Common Questions About Co-signing Student Loans

What is the minimum credit score needed to co-sign a student loan? There is no minimum credit score universally required. Requirements vary greatly among lenders.

How does a co-signer's credit score impact the interest rate? A higher credit score usually results in a lower interest rate. A lower score may result in a higher rate or even rejection.

What happens if the student borrower defaults? The co-signer becomes fully responsible for repaying the loan. This can significantly damage the co-signer's credit history.

Can I get my name removed from the loan after a certain period? Some lenders offer co-signer release options after a set period of on-time payments from the student borrower. This requires meeting specific criteria, such as maintaining a good repayment history.

Practical Tips: Maximizing the Benefits of Co-signing (While Minimizing Risks)

-

Understand the Basics: Thoroughly research the loan terms, repayment schedules, and implications of co-signing.

-

Evaluate the Borrower: Assess the student's financial situation, academic progress, and future employment prospects.

-

Shop Around: Compare offers from multiple lenders to find the most favorable terms.

-

Consider Co-signer Release: Look for loans that offer co-signer release options.

-

Maintain Open Communication: Stay in regular contact with the student borrower to monitor repayment progress.

Final Conclusion: Wrapping Up with Lasting Insights

Co-signing a student loan is a significant financial commitment requiring careful consideration. While it can open doors to educational opportunities, it also carries substantial responsibility. Understanding the role of credit score, lender variability, and potential risks is crucial for both the co-signer and the student borrower. By carefully weighing the pros and cons and employing sound financial strategies, both parties can navigate this process effectively and minimize potential pitfalls.

Latest Posts

Latest Posts

-

International Bond Investing Definition Examples And Risks

Apr 24, 2025

-

International Association Of Financial Engineers Iafe Definition

Apr 24, 2025

-

Internalization Definition In Business And Investing And Example

Apr 24, 2025

-

Internal Rate Of Return Irr Rule Definition And Example 2

Apr 24, 2025

-

Internal Revenue Code Irc Definition What It Covers History

Apr 24, 2025

Related Post

Thank you for visiting our website which covers about What Credit Score Do You Need To Cosign For A Student Loan . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.