What Credit Score Do I Need To Get A Mobile Home

adminse

Apr 07, 2025 · 8 min read

Table of Contents

What Credit Score Do I Need to Get a Mobile Home? Unlocking Your Dream Home

What if securing your dream mobile home hinges on a number you might not even know? Your credit score is a powerful key that can unlock or lock the door to homeownership, and understanding its role in mobile home financing is crucial.

Editor’s Note: This article on securing mobile home financing based on credit score was published today, providing you with the most up-to-date information and insights into the process.

Why Your Credit Score Matters in Mobile Home Financing:

Securing financing for a mobile home, whether new or pre-owned, involves a similar process to traditional home mortgages. Lenders assess your creditworthiness to determine the risk involved in lending you money. Your credit score acts as a primary indicator of that risk. A higher credit score generally translates to more favorable loan terms, including lower interest rates and better chances of approval. Conversely, a low credit score can result in loan denials, higher interest rates, and potentially, more stringent loan conditions. Understanding the specifics of credit score requirements and the different types of financing available is essential for navigating this process successfully. This knowledge empowers you to improve your credit standing if necessary, ultimately increasing your chances of achieving homeownership.

Overview: What This Article Covers:

This article delves into the intricacies of mobile home financing, focusing on the crucial role of your credit score. We will explore the typical credit score requirements for various loan types, the impact of different scoring models, strategies for improving your credit, and resources available to guide you through the process. By the end, you'll have a comprehensive understanding of how to maximize your chances of securing a mobile home loan.

The Research and Effort Behind the Insights:

This article is the result of extensive research, drawing upon data from leading credit bureaus, financial institutions specializing in mobile home financing, and expert analyses from consumer finance professionals. The information presented is based on industry standards and current practices, aiming to provide accurate and reliable insights for potential mobile home buyers.

Key Takeaways:

- Credit Score Ranges and Loan Approval: Understanding the general credit score ranges lenders consider for mobile home loans.

- Types of Mobile Home Financing: Exploring different financing options and their credit score requirements.

- Factors Beyond Credit Score: Identifying other factors lenders consider during the approval process.

- Improving Your Credit Score: Strategies to improve your credit standing before applying for a loan.

- Alternative Financing Options: Exploring options for those with less-than-perfect credit.

Smooth Transition to the Core Discussion:

Now that we've established the importance of credit scores in mobile home financing, let's delve into the specifics. We'll explore the typical credit score ranges, the various types of loans available, and other factors influencing loan approval.

Exploring the Key Aspects of Mobile Home Financing and Credit Scores:

1. Definition and Core Concepts:

A credit score is a three-digit numerical representation of your creditworthiness, based on your credit history. Several scoring models exist, the most common being FICO and VantageScore. These models consider factors like payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders use these scores to assess the likelihood of you repaying a loan. For mobile home financing, a higher credit score generally translates to better loan terms.

2. Applications Across Industries (Focus on Mobile Home Financing):

The application of credit scores in mobile home financing mirrors its use in other types of loans. Lenders use your credit score to determine your eligibility for a loan, the interest rate you’ll be offered, and the loan terms (e.g., down payment requirements, loan length). The higher your credit score, the better the terms you are likely to receive.

3. Challenges and Solutions:

One major challenge is obtaining financing with a low credit score. This might lead to loan denials, high interest rates, or stringent loan conditions. Solutions involve improving your credit score (discussed later) or exploring alternative financing options like loans with higher interest rates or those secured by co-signers.

4. Impact on Innovation (Focus on Technological Advancements in Lending):

Technological advancements have streamlined the mobile home lending process. Online lenders and improved credit reporting systems make it easier for borrowers to access financing and for lenders to assess risk more efficiently.

Closing Insights: Summarizing the Core Discussion:

Your credit score significantly impacts your ability to secure mobile home financing. A higher score opens doors to better loan terms and a smoother application process. Conversely, a lower score can present challenges but doesn't necessarily preclude homeownership. Understanding this relationship empowers you to take proactive steps toward achieving your goal.

Exploring the Connection Between Down Payment and Credit Score:

The relationship between your down payment and credit score is intricate. While a substantial down payment can compensate for a slightly lower credit score, a higher credit score often results in better financing options, potentially reducing the required down payment. Lenders typically prefer larger down payments for borrowers with lower credit scores to mitigate risk.

Key Factors to Consider:

- Roles and Real-World Examples: A borrower with a 700+ credit score might qualify for a loan with a 10% down payment, while a borrower with a 620 score may need a 20% or even higher down payment to get approved.

- Risks and Mitigations: A lower down payment increases the lender's risk, which is why lenders often offset this risk by requiring a higher credit score or charging a higher interest rate.

- Impact and Implications: A larger down payment can improve your chances of approval, even with a less-than-perfect credit score. However, a higher credit score is always advantageous as it leads to better loan terms and reduces the overall cost of borrowing.

Conclusion: Reinforcing the Connection:

The interplay between down payment and credit score is crucial in mobile home financing. While a larger down payment can help offset a lower credit score, a high credit score significantly improves your access to favorable loan terms and reduces the financial burden of homeownership.

Further Analysis: Examining Credit Repair in Greater Detail:

Improving your credit score is a proactive step towards securing favorable mobile home financing. This involves diligently paying bills on time, keeping credit utilization low (the amount of credit you use compared to your total available credit), maintaining a healthy mix of credit accounts (credit cards, loans), and avoiding opening too many new credit accounts within a short period. Dispute any inaccuracies in your credit report, and consider seeking professional credit counseling if needed.

FAQ Section: Answering Common Questions About Mobile Home Financing and Credit Scores:

Q: What is the minimum credit score required to get a mobile home loan?

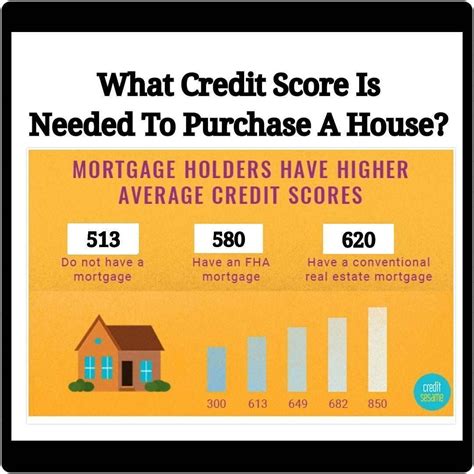

A: There's no single minimum credit score. Requirements vary widely among lenders, depending on loan type, down payment, and other factors. However, a score above 620 is generally considered favorable, while scores below 600 often face significant challenges.

Q: How does my credit score affect my interest rate?

A: A higher credit score typically results in a lower interest rate, reducing the overall cost of your loan. Conversely, a lower score leads to higher interest rates, making the loan more expensive.

Q: What are alternative financing options if I have bad credit?

A: Options include loans with higher interest rates, loans secured by a co-signer, or government-backed loans (depending on eligibility).

Q: How long does it take to improve my credit score?

A: The time required varies depending on the starting point and the steps taken. Consistent positive credit behavior typically shows results within several months to a year.

Practical Tips: Maximizing the Benefits of a Strong Credit Score for Mobile Home Financing:

- Check Your Credit Report: Obtain and review your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) to identify and address any errors.

- Pay Bills On Time: Consistent on-time payments are crucial for building and maintaining a good credit score.

- Reduce Credit Utilization: Keep your credit card balances low, ideally below 30% of your credit limit.

- Maintain a Healthy Credit Mix: A mix of credit accounts (credit cards and installment loans) demonstrates responsible credit management.

- Avoid Opening Many New Accounts: Opening numerous new credit accounts in a short period can negatively impact your score.

- Explore Pre-Approval Options: Get pre-approved for a loan to understand your eligibility and potential loan terms before committing to a specific mobile home.

Final Conclusion: Wrapping Up with Lasting Insights:

Your credit score is a critical factor in securing mobile home financing. By understanding the relationship between your credit score and loan approval, proactively managing your credit, and exploring various financing options, you can significantly increase your chances of achieving your dream of mobile home ownership. Remember, a good credit score is not just about getting a loan—it's about establishing financial stability and securing better terms for the long term.

Latest Posts

Latest Posts

-

Advance Refunding Definition

Apr 30, 2025

-

Advance Premium Fund Definition

Apr 30, 2025

-

Advance Premium Definition

Apr 30, 2025

-

Advance Funded Pension Plan Definition

Apr 30, 2025

-

Advance Commitment Definition

Apr 30, 2025

Related Post

Thank you for visiting our website which covers about What Credit Score Do I Need To Get A Mobile Home . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.