What Banks Offer No Doc Mortgage Loans

adminse

Mar 31, 2025 · 7 min read

Table of Contents

Unmasking the Mystery: Which Banks Offer No-Doc Mortgage Loans?

What if securing a mortgage didn't require mountains of paperwork? No-documentation loans, while less common than traditional mortgages, offer a lifeline to borrowers with unique financial situations.

Editor’s Note: This article on no-doc mortgage loans was published today and provides up-to-date insights into lenders, eligibility criteria, and the associated risks. This information is for general knowledge and does not constitute financial advice. Always consult with a qualified mortgage professional before making any financial decisions.

Why No-Doc Mortgages Matter: Relevance, Practical Applications, and Industry Significance

No-documentation mortgages, often referred to as "low-doc" or "stated-income" loans, cater to a specific segment of borrowers who may struggle to meet the stringent documentation requirements of traditional mortgages. These borrowers might include self-employed individuals with fluctuating income, business owners with complex financial records, or those experiencing temporary financial disruptions. While riskier for lenders, these loans provide access to homeownership for those otherwise excluded. The industry significance lies in its ability to expand the pool of eligible borrowers and stimulate the housing market.

Overview: What This Article Covers

This article explores the landscape of no-doc mortgages, identifying lenders (where available), examining eligibility criteria, highlighting the inherent risks, and comparing them to traditional mortgages. We'll delve into the current state of the market, the types of no-doc loans available, and what borrowers should consider before applying. Readers will gain a comprehensive understanding of this niche lending sector and its implications.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon data from the Mortgage Bankers Association, financial news sources, and analysis of lender websites and public statements. While specific lenders offering no-doc loans can change rapidly, the insights presented reflect current market trends and best practices. The focus is on providing a clear and factual overview of this complex financial product.

Key Takeaways:

- Definition and Core Concepts: A clear understanding of what constitutes a no-doc mortgage and its underlying principles.

- Lenders and Availability: An overview of banks and lenders (where available) that historically have offered or may offer such loans (note: availability is subject to change).

- Eligibility Criteria: A detailed exploration of the requirements and qualifications borrowers need to meet.

- Risks and Rewards: A balanced assessment of the potential benefits and drawbacks of no-doc mortgages.

- Alternatives to No-Doc Mortgages: Exploring other lending options for borrowers with less-than-perfect documentation.

Smooth Transition to the Core Discussion

Having established the relevance and importance of no-doc mortgages, let's now delve into the specifics, examining the challenges and opportunities associated with this specialized lending option.

Exploring the Key Aspects of No-Doc Mortgage Loans

Definition and Core Concepts:

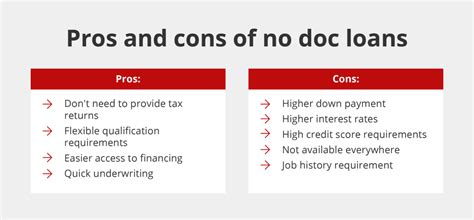

A no-doc mortgage is a loan where borrowers provide minimal documentation to verify their income and assets. This differs significantly from traditional mortgages, which require extensive documentation, including tax returns, pay stubs, bank statements, and proof of assets. The reduced documentation requirement simplifies the application process for certain borrowers, but it also carries increased risk for lenders, resulting in higher interest rates and stricter eligibility criteria. The term "no-doc" can be misleading; while some lenders may use the term, it is more accurate to refer to them as "low-documentation" mortgages because some verification will usually still be required.

Lenders and Availability (Historical and Current Trends):

The availability of no-doc mortgages has fluctuated significantly over the years. Following the 2008 financial crisis, regulatory changes and increased scrutiny made these loans far less common. Many banks and mortgage lenders largely ceased offering them due to the increased risk of default. While some smaller lenders or specialized mortgage brokers might still offer variations of low-doc loans, finding them requires extensive research and likely involves higher interest rates. It is crucial to understand that the availability of these loans changes constantly due to market conditions and lender policies. Therefore, it's impossible to provide a definitive list of banks currently offering them.

Eligibility Criteria:

Even with reduced documentation, borrowers applying for low-doc mortgages will generally need to meet certain criteria, which may include:

- Credit Score: A strong credit score is typically required, usually above 680, to compensate for the lack of extensive income verification.

- Down Payment: A larger down payment (often 20% or more) is frequently demanded to mitigate lender risk.

- Debt-to-Income Ratio (DTI): A low DTI is essential to demonstrate the borrower's ability to repay the loan, despite limited income verification.

- Assets: Proof of sufficient assets might still be required, even without detailed income documentation.

- Property Appraisal: A property appraisal is always necessary to determine the loan-to-value (LTV) ratio.

Risks and Rewards:

Rewards:

- Faster Application Process: Reduced paperwork can streamline the application process.

- Access to Homeownership: Provides opportunities for borrowers who struggle to meet traditional mortgage requirements.

Risks:

- Higher Interest Rates: The higher risk for lenders translates to significantly higher interest rates compared to traditional mortgages.

- Stricter Eligibility Criteria: Borrowers need exceptional credit and a substantial down payment to qualify.

- Potential for Default: The lack of thorough income verification increases the risk of loan default.

- Limited Availability: Finding lenders that offer these types of loans can be challenging.

Alternatives to No-Doc Mortgages:

Borrowers who cannot meet the requirements for a traditional mortgage but find no-doc loans unavailable or unsuitable should explore alternative options:

- Government-backed loans (FHA, VA, USDA): These loans often have more lenient requirements than conventional mortgages.

- Private Mortgage Insurance (PMI): Paying for PMI can allow borrowers with lower down payments to qualify for a traditional mortgage.

- Working with a mortgage broker: Brokers can help find lenders with more flexible lending programs.

Exploring the Connection Between Credit Score and No-Doc Mortgage Loans

The relationship between a credit score and the ability to secure a no-doc mortgage is paramount. A high credit score serves as a crucial indicator of creditworthiness, compensating for the limited income documentation.

Key Factors to Consider:

- Roles and Real-World Examples: A borrower with an excellent credit score (750+) and a 30% down payment might be eligible for a low-doc loan, even with a less-than-perfect income history.

- Risks and Mitigations: A low credit score drastically reduces the chances of approval, regardless of the down payment.

- Impact and Implications: A strong credit score is the primary mitigating factor against the inherent risks associated with reduced documentation.

Conclusion: Reinforcing the Connection

The interplay between a strong credit score and a successful no-doc mortgage application cannot be overstated. It's a critical factor lenders rely on to assess risk in the absence of comprehensive income verification.

Further Analysis: Examining Credit Score in Greater Detail

A deeper dive into credit score reveals its multifaceted role in financial decisions. It's a numerical representation of a borrower's credit history, factoring in payment history, debt levels, and credit utilization. Lenders use it to predict the likelihood of timely repayment, making it a vital element in mortgage approvals.

FAQ Section: Answering Common Questions About No-Doc Mortgage Loans

- What is a no-doc mortgage? A no-doc mortgage is a loan requiring minimal documentation to verify income, though some verification usually remains.

- Who qualifies for a no-doc mortgage? Typically, borrowers with excellent credit scores, substantial down payments, and low debt-to-income ratios.

- Are no-doc mortgages risky? Yes, both for borrowers (high interest rates) and lenders (increased default risk).

- Where can I find a no-doc mortgage? Finding lenders offering these loans can be challenging; working with a mortgage broker may be beneficial.

- What are the alternatives to no-doc mortgages? Government-backed loans, PMI, and working with a mortgage broker to find more flexible lending programs.

Practical Tips: Maximizing the Benefits of Considering No-Doc Mortgage Options

- Assess Your Financial Situation: Honestly evaluate your credit score, down payment capacity, and debt-to-income ratio.

- Research Lenders: Explore lenders who historically have offered, or may still offer, low-doc loans. Expect higher interest rates.

- Consult a Mortgage Professional: Seek advice from a qualified professional to understand your options and the potential risks.

Final Conclusion: Wrapping Up with Lasting Insights

No-doc mortgages represent a niche segment of the mortgage market, offering potential access to homeownership for borrowers who struggle with traditional loan requirements. However, the risks associated with reduced documentation, namely higher interest rates and limited availability, must be carefully weighed against the benefits. Thorough research, careful planning, and professional guidance are essential before pursuing this less-common lending option. The information provided here should serve as a starting point for further investigation and discussion with financial professionals.

Latest Posts

Latest Posts

-

How To Include Federal Pension In Retirement Planning

Apr 29, 2025

-

How To Use Annuities In Retirement Planning

Apr 29, 2025

-

What Rate Of Return To Use For Retirement Planning

Apr 29, 2025

-

What Is A Roll Rate Definition Calculation Methods Example

Apr 29, 2025

-

Roll In Definition

Apr 29, 2025

Related Post

Thank you for visiting our website which covers about What Banks Offer No Doc Mortgage Loans . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.