Smoothing Consumption Definition

adminse

Mar 25, 2025 · 10 min read

Table of Contents

Smoothing Consumption: A Deep Dive into Stable Spending

What if economic stability hinges on our ability to smooth consumption? This critical concept underpins economic resilience and offers valuable insights into individual and societal well-being.

Editor’s Note: This article on smoothing consumption was published today, offering a comprehensive overview of its definition, applications, and implications for economic stability. We delve into both theoretical frameworks and real-world examples to provide a current and insightful understanding of this crucial topic.

Why Smoothing Consumption Matters: Relevance, Practical Applications, and Industry Significance

Smoothing consumption refers to the practice of maintaining a relatively stable level of spending over time, despite fluctuations in income or other economic factors. It's a fundamental concept in economics that impacts individual financial health, business planning, and macroeconomic stability. Understanding how individuals and societies manage consumption smoothing is crucial for predicting economic trends, designing effective policies, and fostering sustainable growth. The ability to smooth consumption reduces the vulnerability of individuals and economies to economic shocks, such as job loss, unexpected medical expenses, or recessions. This resilience has broad implications across various industries, including finance, insurance, and even healthcare.

Overview: What This Article Covers

This article provides a deep dive into smoothing consumption, encompassing its definition, the mechanisms facilitating it, its impact on various economic agents, the challenges involved, and the policy implications. We will explore theoretical frameworks like the permanent income hypothesis and delve into real-world applications and examples, addressing the challenges and suggesting strategies to enhance consumption smoothing.

The Research and Effort Behind the Insights

This article draws upon extensive research from leading economists, relying on established theoretical models and empirical studies. It integrates insights from diverse sources, including academic journals, government reports, and industry analyses, to provide a comprehensive and well-supported perspective on smoothing consumption. The structured approach ensures that the information presented is accurate, reliable, and readily understandable.

Key Takeaways:

- Definition and Core Concepts: A precise definition of consumption smoothing and its underlying principles.

- Mechanisms of Consumption Smoothing: Exploration of various methods individuals and households employ to achieve stable spending.

- Role of Financial Markets: The importance of access to credit, savings, and insurance in facilitating consumption smoothing.

- Impact on Economic Stability: The macroeconomic consequences of varying levels of consumption smoothing across a population.

- Challenges and Policy Implications: Obstacles to consumption smoothing and potential policy interventions to address these issues.

Smooth Transition to the Core Discussion

Having established the importance of understanding consumption smoothing, let's delve into its core components, examining the mechanisms, impacts, and challenges associated with this crucial economic behavior.

Exploring the Key Aspects of Smoothing Consumption

1. Definition and Core Concepts:

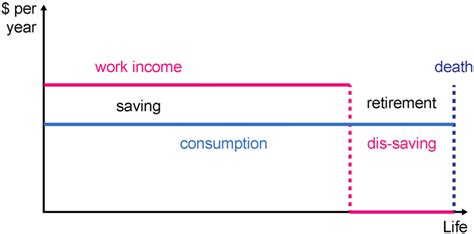

Smoothing consumption, at its heart, is about minimizing the variability of spending patterns over time. It's the attempt to maintain a consistent level of consumption, even when income fluctuates. This doesn't necessarily mean spending remains perfectly constant; rather, it implies that significant, abrupt changes in expenditure are avoided. The underlying principle is that individuals prefer a stable level of consumption to one subject to wide swings, reflecting a preference for predictable utility over time.

2. Mechanisms of Consumption Smoothing:

Several mechanisms contribute to consumption smoothing. These mechanisms can be categorized as:

-

Saving and Borrowing: This is the most common mechanism. During periods of high income, individuals save a portion, building a buffer for times of lower income. Conversely, during periods of low income, they draw upon savings or borrow to maintain their consumption levels. Access to readily available and affordable credit is vital for effective consumption smoothing.

-

Precautionary Saving: This refers to saving undertaken to protect against unforeseen events, such as job loss, medical emergencies, or economic downturns. This proactive approach allows individuals to maintain consumption even when faced with unexpected negative shocks.

-

Human Capital Investment: Investing in education and skills development can be viewed as a form of consumption smoothing. Increased human capital typically leads to higher future income, allowing for more stable consumption over a lifetime.

-

Insurance: Insurance policies (health, unemployment, etc.) provide a safety net against unexpected events, thereby reducing the volatility of consumption. These policies transfer risk from individuals to insurance providers, contributing to consumption stability.

3. Role of Financial Markets:

Well-functioning financial markets are essential for consumption smoothing. These markets provide the mechanisms for saving, borrowing, and risk transfer that underpin consumption stability. Access to a variety of financial products, such as savings accounts, loans, and insurance policies, is critical. Efficient and transparent markets ensure fair pricing and reduce the cost of borrowing and risk management, thereby enhancing the effectiveness of consumption smoothing.

4. Impact on Economic Stability:

The aggregate level of consumption smoothing across an economy significantly impacts macroeconomic stability. When a large portion of the population effectively smooths consumption, the overall demand for goods and services remains relatively stable, even during periods of economic downturn. This reduces the severity of recessions and promotes more sustainable growth. Conversely, if consumption is highly volatile, the economy becomes more susceptible to boom-and-bust cycles.

5. Challenges and Policy Implications:

Several challenges hinder effective consumption smoothing:

- Liquidity Constraints: Individuals with limited access to credit or savings may struggle to smooth consumption, particularly during economic downturns. This is often exacerbated for low-income households.

- Information Asymmetry: Lack of information about available financial products or the risks associated with borrowing can prevent individuals from making optimal choices.

- Behavioral Biases: Psychological factors such as impatience, overconfidence, or mental accounting can lead to suboptimal saving and borrowing decisions, hindering consumption smoothing.

- High Interest Rates: High borrowing costs can make it expensive to borrow during periods of low income, limiting the effectiveness of consumption smoothing.

Policy interventions aimed at enhancing consumption smoothing could include:

- Expanding access to credit: Microfinance initiatives, government-backed loan programs, and regulations promoting financial inclusion can help low-income households access credit.

- Improving financial literacy: Educational programs aimed at enhancing financial literacy can empower individuals to make informed decisions about saving and borrowing.

- Providing social safety nets: Unemployment insurance, welfare programs, and affordable healthcare can protect individuals from unexpected shocks, thereby reducing the need for drastic consumption adjustments.

- Managing interest rates: Monetary policy can influence interest rates, making borrowing more affordable and facilitating consumption smoothing.

Closing Insights: Summarizing the Core Discussion

Smoothing consumption is not merely a theoretical concept; it's a crucial driver of economic stability and individual well-being. By understanding the mechanisms involved, the challenges faced, and the potential policy solutions, policymakers and individuals can strive to create a more resilient and equitable economic environment.

Exploring the Connection Between Credit Access and Smoothing Consumption

The relationship between credit access and smoothing consumption is pivotal. Credit access serves as a crucial mechanism enabling individuals and households to maintain stable consumption levels, even when faced with income fluctuations or unexpected expenses. However, it also presents potential risks if not managed responsibly.

Key Factors to Consider:

Roles and Real-World Examples:

- Facilitating Consumption During Income Shortfalls: When income drops, access to credit allows individuals to continue purchasing essential goods and services, preventing a drastic reduction in their standard of living. Examples include using credit cards to cover unexpected medical bills or taking out a personal loan to bridge a gap between jobs.

- Supporting Investment in Human Capital: Credit can finance education, training, or skill development, enabling individuals to increase their future earning potential and ultimately improve their long-term consumption possibilities. Student loans are a prime example.

- Enabling Large Purchases: Credit allows individuals to make larger purchases, such as houses or cars, that are otherwise unaffordable through immediate cash payment. This can improve their quality of life and contribute to long-term consumption stability.

Risks and Mitigations:

- Debt Accumulation: Overreliance on credit can lead to substantial debt accumulation, potentially exceeding an individual's ability to repay. This can have severe consequences, including bankruptcy and financial instability. Careful budgeting, responsible borrowing practices, and financial literacy are crucial mitigations.

- High Interest Rates: High interest rates can make borrowing expensive, reducing the effectiveness of credit as a consumption-smoothing tool. Governments can intervene through policies that promote lower interest rates or provide subsidies for specific types of loans.

- Predatory Lending Practices: Unfair or exploitative lending practices can trap individuals in a cycle of debt, preventing them from achieving consumption stability. Regulations and consumer protection laws are necessary to combat such practices.

Impact and Implications:

The impact of credit access on consumption smoothing extends beyond the individual level. A population with widespread access to affordable and responsible credit experiences greater macroeconomic stability due to more predictable aggregate demand. Conversely, limited credit access or high rates can amplify economic downturns, as consumers are forced to cut back on spending more drastically.

Conclusion: Reinforcing the Connection

The interplay between credit access and consumption smoothing highlights the critical role of financial markets in supporting economic stability and individual well-being. While credit offers invaluable tools for managing consumption, responsible lending practices, consumer education, and appropriate regulatory frameworks are essential to harness its positive impacts while mitigating potential risks.

Further Analysis: Examining Precautionary Saving in Greater Detail

Precautionary saving, the setting aside of funds to protect against unforeseen negative events, is a crucial component of consumption smoothing. It acts as a buffer against shocks to income or wealth, preventing sharp declines in consumption. The level of precautionary saving depends on several factors:

- Risk Aversion: Individuals with higher risk aversion tend to save more as a precaution against adverse events.

- Uncertainty: Higher levels of uncertainty about future income or expenses generally lead to increased precautionary saving.

- Access to Insurance: The availability and affordability of insurance reduce the need for precautionary saving, as individuals can transfer some of their risk to insurance providers.

- Income Level: Higher-income individuals typically have a greater capacity to save, leading to higher levels of precautionary saving.

Real-world examples include individuals saving for unexpected medical expenses, unemployment, or home repairs. Empirical studies have shown that precautionary saving can significantly mitigate the impact of economic shocks on consumption. The availability of accessible and affordable insurance products plays a vital role in reducing the necessity for high levels of precautionary saving.

FAQ Section: Answering Common Questions About Smoothing Consumption

Q: What is the difference between smoothing consumption and constant consumption?

A: Smoothing consumption aims for relatively stable consumption over time, allowing for some minor fluctuations. Constant consumption implies perfectly unchanging spending, which is rarely achievable in practice.

Q: How does inflation affect consumption smoothing?

A: Inflation erodes the real value of savings, making it more challenging to smooth consumption over long periods. Individuals need to adjust their saving and borrowing plans to account for inflation.

Q: Can businesses also benefit from smoothing consumption strategies?

A: Yes, businesses can benefit from smoothing their consumption of inputs and investment to manage their cash flow and mitigate risks related to fluctuating demand.

Q: What role does government policy play in facilitating consumption smoothing?

A: Government policies, such as unemployment insurance, welfare programs, and tax incentives for saving, can significantly influence individuals' ability to smooth consumption.

Practical Tips: Maximizing the Benefits of Smoothing Consumption

- Create a budget: Tracking income and expenses helps identify areas where spending can be adjusted and savings increased.

- Build an emergency fund: Aim for at least 3-6 months' worth of living expenses in a readily accessible savings account.

- Explore insurance options: Consider health, life, disability, and homeowner's insurance to protect against unforeseen events.

- Develop a long-term savings plan: Investing in retirement accounts and other long-term savings vehicles ensures financial security in later life.

- Manage debt responsibly: Avoid high-interest debt and prioritize paying down existing debt to reduce financial burden.

Final Conclusion: Wrapping Up with Lasting Insights

Smoothing consumption is a cornerstone of economic resilience, underpinning both individual financial stability and macroeconomic health. By understanding its mechanisms, challenges, and the crucial role of financial markets and policies, we can strive toward a more equitable and sustainable economic future where individuals and economies are better equipped to withstand economic shocks and maintain a consistent standard of living. The pursuit of consumption smoothing remains a vital area of ongoing research and policy development, shaping how we approach economic security in an ever-changing world.

Latest Posts

Related Post

Thank you for visiting our website which covers about Smoothing Consumption Definition . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.