Minimum Payment On 200 Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Payment on a $200 Credit Card Balance: A Comprehensive Guide

What if a seemingly small minimum payment on a $200 credit card balance could lead to a debt trap? Understanding the nuances of minimum payments is crucial for responsible credit card management.

Editor’s Note: This article provides a comprehensive overview of minimum payments on credit cards, specifically focusing on a $200 balance. It offers insights into calculation methods, the long-term financial implications of only making minimum payments, and strategies for effective debt management. This information is current as of October 26, 2023.

Why Minimum Payments Matter: The Hidden Costs of Convenience

Many credit card holders find the convenience of minimum payments appealing. The seemingly small amount can seem manageable, especially with a balance as low as $200. However, relying solely on minimum payments can lead to significant long-term financial consequences. Understanding the interest calculations, the snowball effect of accumulating debt, and the impact on your credit score are essential for making informed financial decisions. This knowledge empowers you to avoid the hidden costs associated with this seemingly innocuous practice. The seemingly insignificant $200 balance can quickly escalate into a much larger financial burden if not managed effectively.

Overview: What This Article Covers

This article will dissect the intricacies of minimum payments, specifically focusing on a $200 credit card balance. We will explore how minimum payments are calculated, the dangers of relying solely on them, the impact on your credit score, strategies for paying off the debt faster, and answer frequently asked questions. Readers will gain practical insights and actionable steps to manage their credit card debt effectively.

The Research and Effort Behind the Insights

This article draws upon extensive research from reputable financial institutions, consumer protection agencies, and scholarly articles on personal finance. The information presented is supported by data and examples to ensure accuracy and provide readers with reliable guidance. The analysis incorporates various scenarios to highlight the potential consequences of different payment strategies.

Key Takeaways:

- Understanding Minimum Payment Calculations: Learn how credit card companies determine your minimum payment amount.

- The High Cost of Interest: Discover the significant impact of compounding interest when only making minimum payments.

- Impact on Credit Score: Explore how consistently making only minimum payments affects your creditworthiness.

- Strategies for Accelerated Debt Repayment: Learn effective methods for paying off your $200 balance faster.

- Preventing Future Debt Accumulation: Develop strategies for responsible credit card usage to avoid similar situations.

Smooth Transition to the Core Discussion:

With a foundational understanding of why understanding minimum payments is crucial, let's delve into the specifics of calculating minimum payments and the implications of different repayment strategies.

Exploring the Key Aspects of Minimum Payments on a $200 Balance

1. Definition and Core Concepts:

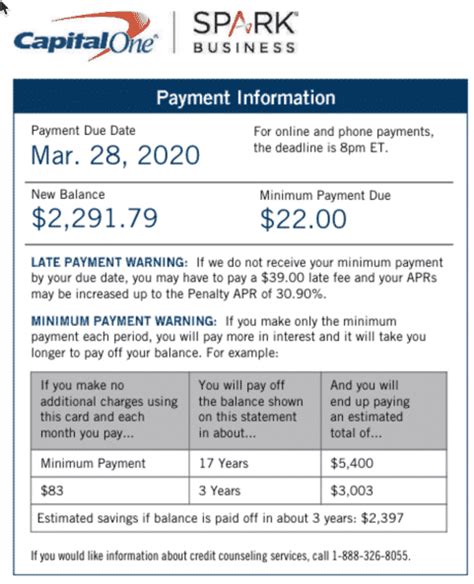

The minimum payment is the smallest amount a credit card company requires you to pay each month to avoid late payment fees and keep your account in good standing. This amount typically includes a portion of the principal balance and the accrued interest. The percentage of the principal covered by the minimum payment varies depending on the card issuer and your credit history. It's important to note that this amount is often a very small percentage of your total outstanding balance, particularly for smaller balances. For a $200 balance, the minimum payment might be as low as $10 or even less, depending on the card's terms and conditions.

2. Applications Across Industries:

The concept of minimum payments is consistent across most credit card issuers. However, the specific calculation method and the minimum payment percentage might slightly vary. Some cards might have a fixed minimum payment amount (e.g., $25), while others calculate it as a percentage of the outstanding balance (e.g., 1-3%). It’s crucial to understand your specific credit card agreement to accurately determine your minimum payment.

3. Challenges and Solutions:

The primary challenge with minimum payments is the high cost of interest. Because such a small portion of the principal is paid each month, a significant portion of your payment goes towards interest, which prolongs the repayment period and increases the total amount you pay over time. The solution is to make payments larger than the minimum payment whenever possible, thus accelerating the debt repayment process and reducing the overall interest charges.

4. Impact on Innovation:

The concept of minimum payments hasn't changed significantly over time, but the ease of accessing credit and the prevalence of digital banking have made managing credit card debt, and therefore minimum payments, more accessible but not necessarily easier. Innovations in personal finance apps and budgeting tools now provide more transparency and assist in managing debt more effectively.

Closing Insights: Summarizing the Core Discussion

Minimum payments, while seemingly convenient, can be a significant obstacle to responsible debt management. The combination of high interest rates and slow repayment can lead to substantial increases in the total amount owed. Understanding the calculations and implications is the first step towards avoiding this trap.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is crucial. High interest rates significantly increase the proportion of your payment allocated to interest, leaving a smaller amount to reduce the principal balance. This creates a vicious cycle where the debt takes longer to repay, and you end up paying substantially more in interest.

Key Factors to Consider:

-

Roles and Real-World Examples: Let's consider a $200 balance with a 20% APR (Annual Percentage Rate). If your minimum payment is $10, a large portion of that will go towards interest, leaving only a small amount to reduce the principal. Over time, the interest will accumulate, making the debt harder to manage.

-

Risks and Mitigations: The primary risk is prolonged debt and significant interest charges. Mitigation strategies include paying more than the minimum payment, exploring debt consolidation options, or contacting your credit card company to discuss potential payment plans.

-

Impact and Implications: The long-term impact can be substantial, affecting your credit score, hindering your ability to borrow money, and potentially leading to financial hardship.

Conclusion: Reinforcing the Connection

The connection between interest rates and minimum payments is undeniable. Higher interest rates, coupled with minimum payments, create a debt trap that can be difficult to escape. Understanding this dynamic and implementing strategies to accelerate repayment is crucial for maintaining good financial health.

Further Analysis: Examining APR in Greater Detail

The Annual Percentage Rate (APR) is a crucial factor influencing minimum payment effectiveness. A higher APR means a larger portion of your payment goes towards interest. This necessitates aggressive repayment strategies to minimize the overall cost of borrowing.

FAQ Section: Answering Common Questions About Minimum Payments

-

Q: What happens if I only make minimum payments? A: You will pay off your debt much slower, accruing significant interest charges over time. This can significantly increase the total amount you repay.

-

Q: How are minimum payments calculated? A: The calculation varies between credit card companies. Some use a fixed minimum amount, while others calculate it as a percentage of the outstanding balance (often 1-3%).

-

Q: Can I negotiate a lower minimum payment? A: It's possible to contact your credit card company and request a hardship plan or alternative payment arrangement, but this isn't always guaranteed.

-

Q: Will making only minimum payments affect my credit score? A: While not immediately impacting your credit score, consistently making only minimum payments can negatively affect your credit utilization ratio (the amount of credit used compared to the total available credit), leading to a lower credit score over time.

-

Q: How can I pay off my debt faster? A: Increase your payments beyond the minimum, explore debt consolidation options, and create a robust budget to allocate more funds towards debt repayment.

Practical Tips: Maximizing the Benefits of Responsible Credit Card Use

-

Understand the Basics: Know your credit card agreement, APR, and minimum payment calculation.

-

Track Your Spending: Monitor your credit card usage meticulously to avoid accumulating excessive debt.

-

Budget Effectively: Allocate funds towards debt repayment strategically, prioritizing higher-interest debt.

-

Pay More Than the Minimum: Even small extra payments significantly reduce the overall interest paid and shorten the repayment period.

-

Explore Debt Consolidation: If you have multiple high-interest debts, consider debt consolidation to simplify repayment and potentially lower interest rates.

Final Conclusion: Wrapping Up with Lasting Insights

While the convenience of minimum payments is appealing, especially for a seemingly small balance like $200, relying on them can lead to long-term financial burdens. Understanding the mechanics of minimum payments, interest rates, and the impact on your credit score is crucial for responsible credit card management. By taking proactive steps to pay more than the minimum, create a budget, and explore alternative repayment strategies, you can avoid the pitfalls of minimum payments and achieve financial stability. Remember, responsible credit card usage is key to maintaining good financial health.

Latest Posts

Latest Posts

-

What Are The 5 Principles Of Financial Management

Apr 06, 2025

-

What Degree Do Financial Managers Need

Apr 06, 2025

-

Money Management Adalah

Apr 06, 2025

-

Best Degree For Money

Apr 06, 2025

-

Degrees Dealing With Money

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Minimum Payment On 200 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.