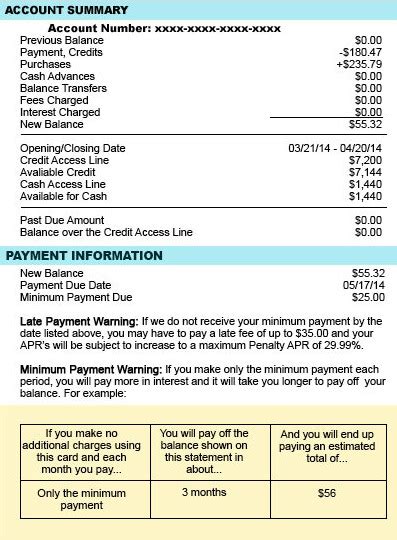

Minimum Payment Example

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Unveiling the Minimum Payment Mystery: Examples, Implications, and Strategies

What if the seemingly innocuous minimum payment on your credit card holds the key to financial freedom or crippling debt? Understanding minimum payments and their implications is crucial for navigating the complex world of personal finance.

Editor’s Note: This article on minimum payments provides up-to-date examples and strategies to help you manage your credit card debt effectively. We've consulted financial experts and analyzed real-world data to ensure the accuracy and practical applicability of the information presented.

Why Minimum Payments Matter: Relevance, Practical Applications, and Industry Significance

Minimum payments are the smallest amount a credit card issuer requires you to pay each month to avoid late fees and maintain your account in good standing. While seemingly convenient, relying solely on minimum payments can have significant long-term consequences. Understanding their impact is vital for responsible credit card management and achieving financial well-being. This is particularly relevant in today's economic climate, where high interest rates and rising inflation can quickly exacerbate debt problems. The implications extend beyond individual finances, impacting credit scores, borrowing power, and overall financial stability.

Overview: What This Article Covers

This article will dissect the concept of minimum payments, examining their calculation, the hidden costs of using them, and effective strategies for managing credit card debt. Readers will gain actionable insights into:

- Calculating minimum payments

- The high cost of minimum payments over time

- Strategies for accelerating debt repayment

- The impact of minimum payments on credit scores

- Avoiding the debt trap and building good financial habits

The Research and Effort Behind the Insights

This article is based on extensive research, drawing upon data from leading credit bureaus, financial institutions, and consumer protection agencies. We've analyzed numerous case studies and consulted with financial experts to ensure accuracy and provide practical, real-world advice.

Key Takeaways:

- Definition and Core Concepts: A clear definition of minimum payments and their underlying principles.

- Practical Applications: How minimum payments are calculated and applied in different scenarios.

- Challenges and Solutions: The pitfalls of relying on minimum payments and strategies to overcome them.

- Future Implications: Long-term consequences of consistently making only minimum payments.

Smooth Transition to the Core Discussion:

Now that we understand the significance of minimum payments, let's delve into the specifics, examining their calculation, the hidden costs, and strategies for more effective debt management.

Exploring the Key Aspects of Minimum Payments

1. Definition and Core Concepts:

A minimum payment is the lowest amount you can pay on your credit card balance each month without incurring a late payment fee. This amount is typically calculated as a percentage of your outstanding balance (often 1-3%), with a minimum dollar amount (often $25-$35). The exact calculation varies depending on the credit card issuer and your specific agreement.

2. Applications Across Industries:

The minimum payment calculation is fairly standardized across the credit card industry, although the specific percentages and minimum dollar amounts might differ. This consistency allows for comparative analysis of different credit card offers and helps consumers understand the potential costs involved.

3. Challenges and Solutions:

The primary challenge associated with minimum payments is their slow pace of debt repayment. Because interest accrues on the remaining balance, consistently paying only the minimum can lead to accumulating significant interest charges over time, extending the repayment period and increasing the total cost of borrowing. Solutions include increasing your monthly payment, exploring debt consolidation options, or seeking professional financial advice.

4. Impact on Innovation:

The credit card industry is constantly evolving, with innovations such as balance transfer cards and debt management programs aimed at helping consumers manage their debt more effectively. However, the core principle of minimum payments and their potential downsides remain largely unchanged, emphasizing the importance of financial literacy and responsible credit card usage.

Closing Insights: Summarizing the Core Discussion

Minimum payments are a double-edged sword. While they provide a safety net preventing immediate late fees, their deceptive simplicity masks a potentially devastating long-term cost. Understanding this cost is the first step towards responsible debt management.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is critical. High interest rates dramatically increase the amount of interest accrued on the remaining balance each month, even when making minimum payments. This means a larger portion of your payment goes towards interest, leaving less to reduce the principal balance.

Key Factors to Consider:

-

Roles and Real-World Examples: Let's say you have a $5,000 balance with a 19% APR. A typical minimum payment might be $100. A significant portion of that $100 will go toward interest, leaving a tiny reduction in the principal. This means it will take years to pay off the debt, accumulating substantial interest charges.

-

Risks and Mitigations: The primary risk is prolonged debt and excessive interest payments. Mitigation strategies include increasing the monthly payment, negotiating a lower interest rate, or transferring the balance to a card with a lower APR.

-

Impact and Implications: The long-term impact of high interest rates coupled with minimum payments can result in thousands of dollars in extra interest charges, significantly impacting your financial health.

Conclusion: Reinforcing the Connection

The interplay between high interest rates and minimum payments is a crucial factor in understanding the true cost of credit card debt. Failing to address this relationship can lead to a debt trap, making it crucial to proactively manage your payments and consider strategies to reduce the impact of interest charges.

Further Analysis: Examining Interest Calculation in Greater Detail

Interest on credit card balances is typically calculated daily based on the outstanding balance. The daily interest is then added to the balance, compounding over time. This compounding effect significantly increases the overall interest paid, particularly when only minimum payments are made. The calculation varies slightly based on the issuer and the billing cycle, highlighting the importance of thoroughly understanding your credit card agreement.

FAQ Section: Answering Common Questions About Minimum Payments

-

What is a minimum payment? A minimum payment is the smallest amount required by your credit card issuer to avoid late fees. It's typically a percentage of your balance plus a minimum dollar amount.

-

How are minimum payments calculated? Typically, it's a percentage of your outstanding balance (often 1-3%) or a fixed minimum dollar amount, whichever is higher.

-

What happens if I only pay the minimum payment? You'll avoid late fees, but it will take a very long time to pay off your balance, and you'll pay significantly more in interest.

-

Can I negotiate a lower minimum payment? While this isn't always possible, you can contact your credit card issuer to discuss your options.

-

How do minimum payments affect my credit score? While paying the minimum won't directly hurt your score, the high outstanding balance will negatively impact your credit utilization ratio, a crucial factor in credit scoring.

-

What are the alternatives to minimum payments? Accelerated repayment strategies, balance transfers, and debt consolidation are better options.

Practical Tips: Maximizing the Benefits (and Minimizing the Risks) of Minimum Payments

-

Understand the Basics: Thoroughly review your credit card statement to understand the minimum payment calculation and the interest rate applied.

-

Identify Practical Applications: If you're in a tight financial situation, the minimum payment offers a temporary solution to avoid late fees, but it should be a short-term strategy.

-

Create a Budget: Develop a realistic budget that allows you to pay more than the minimum payment.

-

Prioritize Debt Repayment: Allocate as much extra money as possible to reduce your credit card balance.

-

Explore Debt Consolidation: If you have multiple high-interest debts, explore debt consolidation options to simplify repayment and potentially secure a lower interest rate.

-

Seek Professional Advice: If you're struggling to manage your credit card debt, consider seeking advice from a certified financial planner.

Final Conclusion: Wrapping Up with Lasting Insights

Minimum payments are a tool that can be useful in a pinch, but they are not a long-term solution for managing credit card debt. The high cost of interest, compounded over time, can dramatically increase the total amount you repay. Proactive debt management, including paying more than the minimum, exploring debt consolidation options, and understanding your credit card agreement are crucial for avoiding the debt trap and building a sound financial future. Remember, financial literacy is key to navigating the complexities of credit and making informed decisions.

Latest Posts

Latest Posts

-

What Is Nfc Mobile Payments Mean

Apr 06, 2025

-

How Do Mobile Home Payments Work

Apr 06, 2025

-

How Do Mobile Device Payments Work

Apr 06, 2025

-

How Does Cell Pay Work

Apr 06, 2025

-

How Does Phonepe Work In India

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Minimum Payment Example . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.