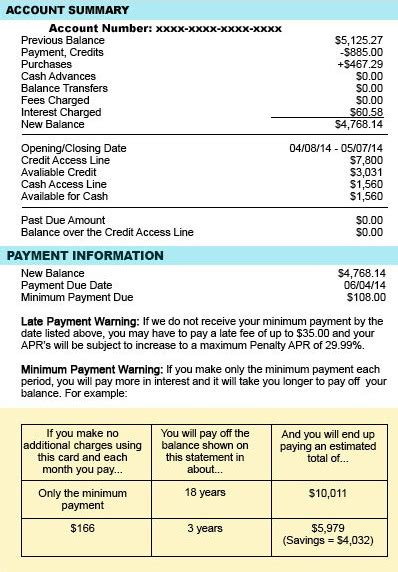

Minimum Monthly Payment Example

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Decoding the Minimum Monthly Payment: Examples, Implications, and Strategies

What if the seemingly innocuous minimum monthly payment is silently sabotaging your financial future? Understanding its mechanics and implications is crucial for achieving long-term financial freedom.

Editor’s Note: This article on minimum monthly payments provides a comprehensive overview of this crucial aspect of personal finance, offering practical examples and actionable strategies. It's been updated to reflect current best practices and industry trends.

Why Minimum Monthly Payments Matter: Relevance, Practical Applications, and Industry Significance

Minimum monthly payments are the bedrock of revolving credit accounts like credit cards and some personal loans. While seemingly convenient, relying solely on them can have significant long-term consequences, impacting credit scores, increasing overall interest paid, and potentially hindering financial goals. Understanding how these payments work and their implications is vital for responsible debt management. This knowledge empowers individuals to make informed decisions, optimize their finances, and avoid the pitfalls of prolonged indebtedness. The information presented here is relevant to anyone with revolving credit, emphasizing the importance of financial literacy and strategic debt repayment.

Overview: What This Article Covers

This article will delve into the intricacies of minimum monthly payments, exploring their calculation, the implications of using them exclusively, and strategies for more effective debt repayment. We'll examine real-world examples, analyze the impact on credit scores, and provide actionable steps for readers to gain control of their finances. We will also explore the connection between minimum payments and the overall cost of credit.

The Research and Effort Behind the Insights

This article draws upon extensive research, incorporating data from consumer finance reports, credit scoring models, and industry best practices. Calculations and examples are based on commonly available interest rates and minimum payment structures. The aim is to provide readers with accurate and actionable information based on verifiable sources.

Key Takeaways:

- Definition and Core Concepts: A clear explanation of minimum monthly payments and how they are calculated.

- Practical Applications: Real-world examples demonstrating the effects of different payment strategies.

- Challenges and Solutions: Identifying the pitfalls of relying on minimum payments and offering effective alternatives.

- Future Implications: The long-term impact of minimum payment strategies on financial well-being.

Smooth Transition to the Core Discussion

Now that we understand the significance of minimum monthly payments, let's dive into the details, exploring how they are calculated, the hidden costs involved, and effective strategies for managing debt more efficiently.

Exploring the Key Aspects of Minimum Monthly Payments

1. Definition and Core Concepts:

The minimum monthly payment is the smallest amount a borrower is required to pay on a revolving credit account each month. It's typically a percentage of the outstanding balance (often 1-3%), plus any accrued interest. The exact calculation varies depending on the lender and the terms of the credit agreement. Crucially, this payment is often designed to merely cover the accrued interest, leaving the principal balance largely untouched.

2. Applications Across Industries:

Minimum monthly payments are common across various revolving credit products:

- Credit Cards: The most prevalent application, where the minimum payment is usually prominently displayed on the monthly statement.

- Personal Lines of Credit: Similar to credit cards, these offer revolving credit with minimum payment requirements.

- Certain Installment Loans: Some installment loans, particularly those with variable interest rates, may require a minimum payment. However, these are less common than with revolving credit.

3. Challenges and Solutions:

The primary challenge with relying on minimum payments is the slow pace of debt reduction. Because the payment often covers only the interest, the principal balance remains largely unchanged, leading to:

- Prolonged Debt: The debt can persist for years, even decades, costing significantly more in interest over time.

- Increased Interest Charges: Paying only the minimum means paying far more interest than if a higher payment was made.

- Damaged Credit Score: High credit utilization (the percentage of available credit used) negatively impacts credit scores, making it harder to obtain loans or secure favorable interest rates in the future.

Solutions:

- Increase Payments: The most effective solution is to increase the monthly payments significantly. Even a small increase can drastically shorten the repayment period and reduce the total interest paid.

- Debt Consolidation: Combining multiple debts into a single loan with a lower interest rate can make repayments more manageable and reduce the overall cost of borrowing.

- Debt Management Plans: Working with a credit counseling agency can help create a structured plan to manage and repay debt.

- Balance Transfers: Transferring high-interest balances to a lower-interest credit card can temporarily reduce monthly payments and accelerate debt repayment.

4. Impact on Innovation:

The rise of fintech apps and personal finance tools has improved access to information and tools that aid in debt management. These technologies often offer features like debt repayment calculators, budgeting tools, and automated savings plans, fostering better financial literacy and informed decision-making.

Exploring the Connection Between Interest Rates and Minimum Monthly Payments

The relationship between interest rates and minimum monthly payments is significant. A higher interest rate on a credit card or loan will generally result in a larger minimum payment (because a greater portion of the payment is allocated to interest). Conversely, a lower interest rate might lead to a smaller minimum payment, but this doesn't necessarily mean the debt will be repaid faster, especially if the principal balance remains high.

Key Factors to Consider:

-

Roles and Real-World Examples: Consider a $10,000 credit card balance with a 20% interest rate. The minimum payment might be only $200 a month. However, a large portion of this goes towards interest, meaning the principal reduces slowly. In contrast, a $10,000 loan with a 5% interest rate might have a higher minimum payment that significantly reduces the principal each month.

-

Risks and Mitigations: The primary risk is getting trapped in a cycle of minimum payments, which can lead to overwhelming debt. Mitigation strategies include budgeting, creating a realistic repayment plan, and seeking professional financial advice when needed.

-

Impact and Implications: The long-term impact of higher interest rates and minimum payments is a significantly increased total cost of borrowing. This can have profound implications for long-term financial goals, such as saving for retirement or buying a home.

Conclusion: Reinforcing the Connection

The connection between interest rates and minimum monthly payments highlights the importance of understanding the terms of any credit agreement before signing. Higher interest rates and minimum payments significantly increase the total cost of borrowing, emphasizing the need for strategic debt management.

Further Analysis: Examining Interest Rates in Greater Detail

Understanding how interest rates are calculated is crucial. Most credit card interest is calculated using the average daily balance method. This means that interest is calculated daily on the outstanding balance and added to the account. The interest rate is an annual percentage rate (APR), which is then divided by 365 to determine the daily interest rate. This daily interest accrues even if only the minimum payment is made, perpetuating the debt cycle.

FAQ Section: Answering Common Questions About Minimum Monthly Payments

-

What is a minimum monthly payment? It's the smallest payment required on a revolving credit account each month, usually a percentage of the balance plus interest.

-

How are minimum monthly payments calculated? The calculation varies by lender, but typically includes a percentage of the outstanding balance and accrued interest.

-

What happens if I only pay the minimum monthly payment? Your debt will take much longer to repay, and you will pay significantly more in interest overall.

-

How can I reduce my minimum monthly payment? You can’t directly reduce it, but you can reduce the underlying debt by making larger payments.

-

Is it always best to pay more than the minimum? Yes, almost always. Paying more than the minimum will drastically reduce the total interest paid and shorten the repayment period.

-

What if I can't afford to pay more than the minimum? Seek professional financial advice to explore options like debt consolidation or debt management plans.

Practical Tips: Maximizing the Benefits of Strategic Debt Repayment

- Understand the Basics: Learn how minimum payments are calculated and their implications.

- Create a Budget: Track income and expenses to identify areas where you can free up extra cash for debt repayment.

- Prioritize High-Interest Debt: Focus on paying down debts with the highest interest rates first.

- Set Realistic Goals: Develop a debt repayment plan with achievable milestones.

- Automate Payments: Set up automatic payments to ensure consistent repayments.

- Seek Professional Help: If you are struggling to manage debt, consult a credit counselor or financial advisor.

Final Conclusion: Wrapping Up with Lasting Insights

Minimum monthly payments, while seemingly convenient, can be a financial trap if not understood and managed effectively. By understanding their mechanics, the associated risks, and implementing strategic repayment strategies, individuals can take control of their finances and avoid the long-term pitfalls of prolonged indebtedness. Financial literacy and proactive debt management are essential for achieving long-term financial success. Don't let the minimum payment deceive you – take charge of your financial future today.

Latest Posts

Latest Posts

-

What If Nfc Mobile Payments

Apr 06, 2025

-

What Does Nfc Mobile Payments

Apr 06, 2025

-

What Is Nfc Mobile Payments Mean

Apr 06, 2025

-

How Do Mobile Home Payments Work

Apr 06, 2025

-

How Do Mobile Device Payments Work

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Minimum Monthly Payment Example . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.