Letter Of Complaint About Credit Card

adminse

Apr 03, 2025 · 7 min read

Table of Contents

Crafting the Perfect Credit Card Complaint Letter: A Guide to Reclaiming Your Rights

What if a simple letter could resolve frustrating credit card issues and restore your financial peace of mind? A well-written complaint letter is your powerful tool to navigate disputes and potentially recoup significant losses.

Editor’s Note: This article provides a comprehensive guide on writing effective credit card complaint letters. The information is current and based on established consumer protection laws and best practices. We encourage you to consult with a financial advisor or legal professional if you have complex or unresolved issues.

Why a Credit Card Complaint Letter Matters:

Credit card disputes are common. Whether it's unauthorized charges, billing errors, inaccurate interest calculations, poor customer service, or identity theft, a formal complaint is your first step towards resolution. A well-written letter not only documents your grievance but also demonstrates your commitment to resolving the issue professionally. It can significantly impact the outcome, potentially saving you time, money, and stress. Ignoring problems can lead to escalating debt, damaged credit scores, and further financial hardship.

Overview: What This Article Covers:

This article provides a step-by-step guide to drafting a compelling credit card complaint letter. We will cover: essential elements to include, effective writing techniques, strategies for addressing various types of credit card disputes, and resources available to assist you. You will learn how to articulate your concerns clearly, present evidence persuasively, and navigate the complaint process effectively.

The Research and Effort Behind the Insights:

This article draws on extensive research encompassing consumer protection laws, credit card industry regulations, and best practices for dispute resolution. We have reviewed numerous case studies and consulted legal and financial resources to ensure accuracy and provide readers with valuable, actionable advice.

Key Takeaways:

- Understanding Your Rights: Knowing your consumer rights under the Fair Credit Billing Act (FCBA) and other relevant regulations is crucial.

- Gathering Evidence: Collecting and organizing supporting documentation strengthens your case significantly.

- Effective Communication: Crafting a clear, concise, and professional letter is vital for a positive outcome.

- Escalation Strategies: Knowing how to escalate your complaint if necessary is essential.

- Alternative Dispute Resolution: Understanding alternative dispute resolution methods can provide additional recourse.

Smooth Transition to the Core Discussion:

Now that we've established the importance of effective credit card complaint letters, let’s delve into the specifics of crafting one that gets results.

Exploring the Key Aspects of Credit Card Complaint Letters:

1. Identifying the Problem and Gathering Evidence:

Before writing your letter, precisely define the issue. Is it an unauthorized transaction, a billing error, incorrect interest charges, or poor customer service? Gather all relevant evidence:

- Statements: Copies of your credit card statements showing the disputed transaction or error.

- Receipts: Receipts for purchases you believe were incorrectly charged.

- Documentation: Any other relevant documentation, such as emails, phone records, or correspondence with the credit card company.

- Identity Theft Report: If you suspect identity theft, include a copy of the police report.

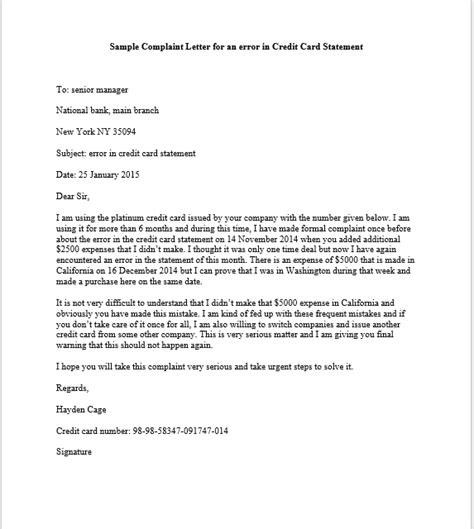

2. Formatting Your Complaint Letter:

Your letter should be professional, concise, and easy to read. Use a clear and straightforward writing style. Follow this format:

- Your Contact Information: Your full name, address, phone number, and email address.

- Date: The date you are writing the letter.

- Credit Card Company's Contact Information: The name and address of the credit card company's customer service department or dispute resolution department. Avoid addressing it to an individual unless you have a specific contact person.

- Account Number: Your credit card account number.

- Subject Line: Clearly state the subject of your complaint (e.g., "Dispute of Unauthorized Transaction," "Billing Error," "Complaint Regarding Poor Customer Service").

- Body Paragraphs: This is where you clearly and concisely describe the problem. Use specific dates, amounts, and transaction details. Refer to the evidence you've gathered. Avoid emotional language; stick to the facts.

- Requested Action: Clearly state what you want the credit card company to do (e.g., refund, credit to your account, removal of charges, etc.).

- Closing: Politely restate your request and thank them for their time and consideration.

- Signature: Sign and print your name.

3. Addressing Specific Types of Credit Card Disputes:

- Unauthorized Transactions: Clearly state that the transaction was unauthorized and provide evidence to support your claim. Mention when you reported the issue.

- Billing Errors: Detail the specific billing error, citing the incorrect amount, transaction date, and merchant. Provide supporting documentation such as receipts.

- Incorrect Interest Charges: Specify the dates and amounts of the interest charges you believe are inaccurate. Explain why you believe they are incorrect, referencing your statement and the cardholder agreement.

- Poor Customer Service: Describe the specific instances of poor customer service you experienced, providing dates, times, and names of customer service representatives if possible.

4. Following Up and Escalating Your Complaint:

Keep a copy of your letter and any supporting documentation. Send your letter via certified mail with return receipt requested to ensure proof of delivery. Follow up after a reasonable timeframe (usually 30 days) if you haven't received a response. If your initial complaint is unsuccessful, escalate the complaint to a higher authority within the credit card company. You may contact their executive offices or customer relations department.

Exploring the Connection Between Consumer Protection Laws and Credit Card Complaints:

The Fair Credit Billing Act (FCBA) is a crucial piece of legislation protecting consumers against inaccurate or unfair credit card billing practices. Understanding your rights under the FCBA is paramount when writing a complaint letter. The FCBA provides a framework for disputing billing errors and unauthorized charges. It mandates a specific process for credit card companies to respond to your complaints.

Key Factors to Consider:

-

Roles and Real-World Examples: The FCBA plays a vital role in protecting consumers against inaccurate billing. For instance, a consumer can dispute a charge under the FCBA if they believe it's erroneous or unauthorized. The credit card company must investigate the dispute and respond within a specific timeframe.

-

Risks and Mitigations: Failing to follow the proper procedures outlined in the FCBA might weaken your case. Thorough documentation and a well-written complaint letter are crucial to mitigate this risk.

-

Impact and Implications: Successfully resolving a credit card dispute under the FCBA can prevent negative impacts on credit scores and avoid unnecessary debt.

Conclusion: Reinforcing the Connection:

The FCBA provides a powerful legal framework for resolving credit card disputes. A well-crafted complaint letter, grounded in the principles of the FCBA, is a crucial tool in exercising your consumer rights and protecting your financial well-being.

Further Analysis: Examining the Fair Credit Billing Act in Greater Detail:

The FCBA outlines specific procedures for consumers to follow when disputing credit card charges. It requires creditors to investigate and respond to complaints within a specified timeframe. The Act also outlines the remedies available to consumers if their dispute is resolved in their favor.

FAQ Section: Answering Common Questions About Credit Card Complaints:

-

What is the Fair Credit Billing Act (FCBA)? The FCBA is a federal law that protects consumers from inaccurate or unfair billing practices by credit card companies.

-

How long do I have to file a dispute under the FCBA? You generally have 60 days from the date the billing error appeared on your statement to dispute it.

-

What should I do if the credit card company refuses to resolve my complaint? You can escalate your complaint to a higher authority within the company, contact your state's attorney general's office, or consider filing a lawsuit.

-

Can I dispute a charge if I used the credit card but disagree with the amount? Yes, if you believe the amount is incorrect, you can dispute it under the FCBA. Provide supporting evidence such as receipts.

-

What if I suspect identity theft? Report it to the police immediately and include a copy of the police report in your complaint letter. Contact the credit bureaus and place fraud alerts on your credit reports.

Practical Tips: Maximizing the Benefits of a Credit Card Complaint Letter:

- Be Specific: Provide precise details, dates, amounts, and supporting documentation.

- Maintain a Professional Tone: Avoid emotional language and keep your letter courteous but firm.

- Keep Records: Maintain copies of all correspondence, statements, and supporting documents.

- Know Your Rights: Familiarize yourself with the FCBA and other relevant consumer protection laws.

- Follow Up: If you don't receive a response within a reasonable timeframe, follow up with the credit card company.

Final Conclusion: Wrapping Up with Lasting Insights:

A well-crafted credit card complaint letter is an essential tool for resolving billing disputes and protecting your financial interests. By understanding your rights, gathering sufficient evidence, and following the steps outlined in this article, you can significantly increase your chances of a successful resolution. Remember, proactive communication and a clear, concise letter are your strongest allies in reclaiming your financial peace of mind.

Latest Posts

Latest Posts

-

What Is Liquidity In Crypto Coin

Apr 03, 2025

-

What Is Liquidity In Cryptocurrency In Urdu

Apr 03, 2025

-

What Is Liquidity In Crypto Reddit

Apr 03, 2025

-

What Is Liquidity In Crypto Exchange

Apr 03, 2025

-

What Is Liquidity In Crypto Market

Apr 03, 2025

Related Post

Thank you for visiting our website which covers about Letter Of Complaint About Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.