How To Reduce Student Loan Interest

adminse

Mar 28, 2025 · 8 min read

Table of Contents

Slashing Student Loan Interest: Strategies for Debt Reduction

What if the key to financial freedom after graduation lies in strategically managing student loan interest? Understanding and implementing effective interest reduction strategies is crucial for navigating the complexities of student loan repayment and achieving long-term financial stability.

Editor’s Note: This article on reducing student loan interest was published today, offering current and practical strategies for borrowers looking to minimize their debt burden and accelerate their repayment journey.

Why Reducing Student Loan Interest Matters:

Student loan debt is a significant financial burden for many graduates. High interest rates can exponentially increase the total amount owed, delaying financial goals like homeownership, starting a family, or investing for retirement. Reducing interest, even by a small percentage, can lead to substantial savings over the life of the loan. This translates to lower monthly payments, faster debt payoff, and improved overall financial health. The strategies discussed in this article are designed to empower borrowers with the knowledge and tools to navigate the complexities of student loan repayment and make informed decisions to minimize their interest costs.

Overview: What This Article Covers

This article provides a comprehensive guide to reducing student loan interest. We'll explore different loan repayment plans, refinancing options, and strategies for minimizing interest accrual. We will also delve into the importance of understanding your loan terms, exploring income-driven repayment plans, and the potential benefits of making extra payments. The article concludes with a frequently asked questions section and actionable tips to help readers effectively manage their student loan debt.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing on information from the U.S. Department of Education, reputable financial institutions, and expert analysis from personal finance professionals. Data on interest rates, repayment plans, and refinancing options are referenced to ensure accuracy and provide readers with reliable information.

Key Takeaways:

- Understanding Loan Types and Terms: Different loan types (federal vs. private) have different interest rates and repayment options.

- Income-Driven Repayment Plans: These plans adjust monthly payments based on income and family size, potentially leading to lower monthly payments and reduced interest accrual in the long run.

- Refinancing: Refinancing student loans can secure a lower interest rate, especially for borrowers with strong credit scores.

- Making Extra Payments: Even small extra payments can significantly reduce the total interest paid over the life of the loan.

- Consolidation: Combining multiple loans can simplify repayment and potentially lower interest rates.

Smooth Transition to the Core Discussion:

Now that we've established the importance of reducing student loan interest, let's explore the key strategies borrowers can utilize to achieve this goal.

Exploring the Key Aspects of Student Loan Interest Reduction

1. Understanding Your Loans:

Before exploring reduction strategies, it's crucial to understand the details of your student loans. This includes:

- Loan Type: Federal student loans offer various repayment plans and protections, unlike private loans.

- Interest Rate: The interest rate determines the cost of borrowing. Lower rates translate to lower interest payments.

- Loan Balance: The principal amount owed directly impacts the total interest paid.

- Repayment Terms: The loan's length (e.g., 10 years, 20 years) significantly influences the total interest accrued.

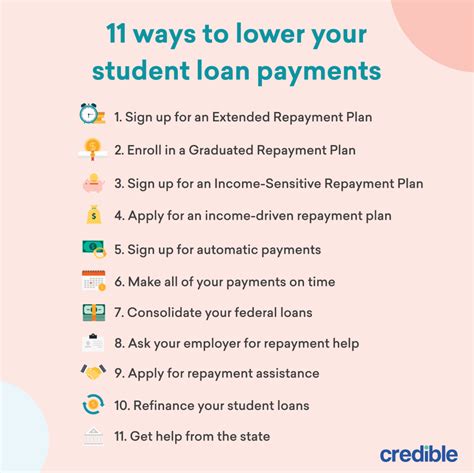

2. Federal Loan Repayment Plans:

The federal government offers several repayment plans designed to make student loan repayment more manageable:

- Standard Repayment Plan: Fixed monthly payments over 10 years.

- Graduated Repayment Plan: Payments start low and increase over time.

- Extended Repayment Plan: Payments spread over a longer period (up to 25 years).

- Income-Driven Repayment (IDR) Plans: These plans (IBR, PAYE, REPAYE, ICR) link monthly payments to your income and family size. They often result in lower monthly payments, but may extend the repayment period and increase the total interest paid over time. This trade-off must be carefully considered.

3. Refinancing Student Loans:

Refinancing involves replacing your existing student loans with a new loan from a private lender. This can be advantageous if:

- You have a good credit score: Lenders often offer lower interest rates to borrowers with strong credit.

- Your interest rate is high: Refinancing can significantly reduce your interest rate.

- You want to simplify repayment: Consolidating multiple loans into one can streamline the process.

However, refinancing federal loans means losing access to federal benefits like income-driven repayment plans and deferment options. Carefully weigh the pros and cons before refinancing.

4. Making Extra Payments:

Even small extra payments toward your principal balance can significantly reduce the total interest paid over the life of the loan. Consider these strategies:

- Bi-weekly payments: Making half your monthly payment every two weeks effectively makes an extra monthly payment each year.

- Annual lump-sum payments: If possible, make a larger payment once a year.

- Windfalls: Direct any unexpected income (tax refunds, bonuses) towards your loan principal.

5. Student Loan Consolidation:

Consolidating multiple federal loans into a single loan can simplify repayment and potentially lower your monthly payment. However, the interest rate on the consolidated loan is typically a weighted average of your existing loans' rates. This might not always result in a lower rate, so careful consideration is needed.

Closing Insights: Summarizing the Core Discussion

Reducing student loan interest is a multifaceted process requiring a strategic approach. Understanding your loan terms, exploring available repayment plans, and considering refinancing options are crucial steps. Making extra payments, even small ones, can make a significant difference over time. The ultimate strategy will depend on individual circumstances, but the key is proactive management and informed decision-making.

Exploring the Connection Between Credit Score and Student Loan Interest

A strong credit score is a powerful tool in reducing student loan interest. Lenders use credit scores to assess risk, and borrowers with higher scores are considered less risky, qualifying them for lower interest rates. Therefore, improving your credit score before refinancing is a crucial step.

Key Factors to Consider:

- Roles and Real-World Examples: A borrower with a 750 credit score is significantly more likely to secure a lower interest rate compared to someone with a 600 score. Real-world examples from reputable financial institutions can demonstrate the impact of credit scores on interest rates.

- Risks and Mitigations: Failing to improve credit scores before refinancing can lead to higher interest rates, negating the intended benefits. Mitigation involves proactively addressing any negative items on credit reports and establishing responsible financial habits.

- Impact and Implications: A higher credit score translates to lower monthly payments, reduced total interest paid, and faster debt payoff. The long-term impact on financial health is considerable.

Conclusion: Reinforcing the Connection

The connection between credit score and student loan interest is undeniable. By prioritizing credit score improvement, borrowers can leverage this powerful tool to significantly reduce their interest costs. This proactive approach is essential for achieving long-term financial well-being.

Further Analysis: Examining Credit Score Improvement in Greater Detail

Improving credit scores requires consistent effort and attention to detail. Key strategies include:

- Paying bills on time: This is the most crucial factor affecting credit scores.

- Keeping credit utilization low: Maintaining a low credit utilization ratio (the amount of credit used compared to the total available) is important.

- Maintaining a diverse credit history: Having a mix of credit accounts (credit cards, loans) demonstrates responsible credit management.

- Monitoring credit reports: Regularly reviewing credit reports helps identify and address any errors.

FAQ Section: Answering Common Questions About Reducing Student Loan Interest

- What is the best way to reduce student loan interest? There's no single "best" way, as the optimal strategy depends on individual circumstances. A combination of strategies (IDR plans, refinancing, extra payments) may be most effective.

- Can I refinance federal student loans? Yes, but this involves losing federal benefits, so carefully weigh the pros and cons.

- How much can I save by refinancing? The potential savings depend on your current interest rate, credit score, and the new rate offered by the lender.

- What are income-driven repayment plans? These plans adjust monthly payments based on your income and family size.

- What if I can't make my student loan payments? Contact your lender immediately to discuss options like forbearance or deferment.

Practical Tips: Maximizing the Benefits of Interest Reduction Strategies

- Understand Your Loans: Gather all loan documents and thoroughly review the terms and conditions.

- Explore Repayment Options: Compare different repayment plans to identify the most suitable option.

- Improve Your Credit Score: Focus on responsible financial habits to increase your creditworthiness.

- Automate Extra Payments: Set up automatic transfers to make extra payments regularly.

- Monitor Your Progress: Track your payments and remaining balance to stay on track.

Final Conclusion: Wrapping Up with Lasting Insights

Reducing student loan interest is a crucial step toward achieving financial freedom. By understanding the available strategies, actively managing your loans, and prioritizing responsible financial habits, you can significantly minimize your debt burden and accelerate your journey to financial well-being. The information provided in this article serves as a valuable resource for navigating the complexities of student loan repayment and making informed decisions to secure your financial future.

Latest Posts

Latest Posts

-

Inflationary Risk Definition Ways To Counteract It

Apr 24, 2025

-

Inflation Protected Security Ips Definition

Apr 24, 2025

-

Inflation Adjusted Return Definition Formula And Example

Apr 24, 2025

-

Inflation Swap Definition How It Works Benefits Example

Apr 24, 2025

-

Inflation Accounting Definition Methods Pros Cons

Apr 24, 2025

Related Post

Thank you for visiting our website which covers about How To Reduce Student Loan Interest . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.