How To Get Lower Minimum Payment On Credit Card

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Negotiating a Lower Minimum Payment on Your Credit Card: A Comprehensive Guide

Is it possible to negotiate a lower minimum credit card payment? Yes, but it's not always easy and requires a strategic approach.

Editor's Note: This comprehensive guide on negotiating lower minimum credit card payments was published today. We understand the financial pressures many face and aim to equip you with the knowledge and strategies to navigate this complex situation.

Why a Lower Minimum Payment Matters:

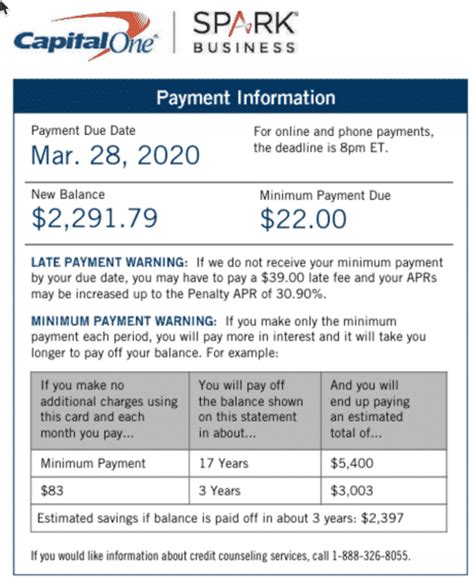

High minimum payments can trap individuals in a cycle of debt, hindering financial progress. A lower minimum payment offers temporary breathing room, enabling better budgeting and debt management strategies. While it doesn't reduce the total debt, it can alleviate immediate financial stress, allowing for more substantial payments down the line. However, it's crucial to remember that lowering your minimum payment doesn't reduce your interest charges; it simply makes the monthly payment smaller.

What This Article Covers:

This article will delve into the intricacies of negotiating a lower minimum payment, exploring various strategies, potential challenges, and the long-term implications. We'll examine the factors influencing a credit card issuer's decision, provide practical tips for successful negotiation, and discuss alternative debt management solutions.

The Research and Effort Behind the Insights:

This article is the culmination of extensive research, incorporating information from consumer finance experts, credit counseling agencies, and analysis of credit card agreements. We've reviewed numerous case studies and examined various credit card issuer policies to provide accurate and actionable advice.

Key Takeaways:

- Understanding Minimum Payment Calculation: Learn how minimum payments are determined and the factors that influence them.

- Negotiation Strategies: Explore effective strategies for communicating with your credit card issuer.

- Alternative Debt Management Options: Discover alternative solutions if negotiation fails.

- Long-Term Implications: Understand the consequences of lowering your minimum payment and how to avoid pitfalls.

Smooth Transition to the Core Discussion:

Now that we've established the importance of this topic, let's delve into the specific strategies and considerations for successfully negotiating a lower minimum payment on your credit card.

Exploring the Key Aspects of Negotiating a Lower Minimum Payment:

1. Understanding Minimum Payment Calculation:

Before attempting negotiation, it's essential to understand how your minimum payment is calculated. While the exact formula varies by issuer, it typically involves a percentage of your outstanding balance (often 1-3%), plus any accrued interest and fees. Higher balances generally result in higher minimum payments. Understanding this calculation allows you to better anticipate the issuer's response to your request.

2. Factors Influencing Issuer Decisions:

Credit card companies are businesses, and their primary goal is to maximize profits. Several factors influence their willingness to negotiate lower minimum payments:

- Your Credit Score: A high credit score demonstrates responsible financial behavior, increasing your negotiation leverage.

- Your Payment History: A consistent history of on-time payments strengthens your case. Conversely, a history of late or missed payments weakens it significantly.

- Your Account Age: Longer-standing accounts often receive more favorable treatment.

- Your Overall Debt: If your total debt burden is high, the issuer might be less inclined to negotiate.

- The Credit Card's APR: A high APR increases the issuer's revenue, making them less likely to compromise.

3. Strategies for Successful Negotiation:

- Gather Documentation: Compile all relevant documents, including your credit card statement, payment history, and any financial hardship documentation (if applicable).

- Contact Customer Service: Begin by contacting your credit card company's customer service department. Explain your situation calmly and professionally, emphasizing your intention to remain a loyal customer and your commitment to paying off your debt.

- Highlight Your Positive Payment History: Emphasize your history of on-time payments, even if you've missed a payment recently due to unforeseen circumstances.

- Propose a Realistic Plan: Instead of simply asking for a lower minimum payment, propose a specific, achievable plan for repayment. This demonstrates your commitment and increases your chances of success. For example, suggest increasing your payments gradually over time.

- Be Prepared for Rejection: Credit card companies are not obligated to negotiate. Be prepared to accept their response, even if it's not what you hoped for.

- Consider a Balance Transfer: If negotiation fails, consider transferring your balance to a card with a lower APR. This will reduce your interest charges, making it easier to manage your debt.

- Negotiate a hardship plan: Many credit card companies have hardship programs for consumers facing financial difficulties. These programs may offer temporary lower minimum payments, reduced interest rates, or other assistance.

- Document Everything: Keep detailed records of all communications, including dates, times, and the names of representatives you spoke with.

4. Alternative Debt Management Options:

If negotiating a lower minimum payment proves unsuccessful, several other debt management strategies can be explored:

- Debt Consolidation: Combining multiple debts into a single loan with a lower interest rate can simplify repayment.

- Credit Counseling: A non-profit credit counseling agency can provide guidance and develop a debt management plan (DMP). A DMP involves negotiating lower interest rates and fixed monthly payments with your creditors.

- Debt Settlement: This involves negotiating a lower lump-sum payment with your creditors to settle your debt. However, debt settlement can negatively impact your credit score.

- Bankruptcy: As a last resort, bankruptcy can eliminate or reduce your debt, but it has significant long-term consequences for your credit history.

5. Long-Term Implications:

Lowering your minimum payment provides temporary relief, but it doesn't eliminate the debt or interest charges. It simply extends the repayment period, resulting in paying more interest over time. To avoid this long-term trap, focus on:

- Budgeting and Expense Management: Create a detailed budget to identify areas where you can cut expenses and free up money for debt repayment.

- Increasing Payments: Once your financial situation stabilizes, strive to make payments significantly higher than the minimum to accelerate debt reduction.

- Avoiding Further Debt: Refrain from incurring new debts until your existing debt is under control.

Exploring the Connection Between Financial Hardship and Negotiating a Lower Minimum Payment:

Financial hardship, such as job loss, medical emergencies, or unexpected expenses, can severely impact your ability to meet your minimum credit card payments. In such situations, proactively communicating with your credit card issuer is crucial. Explain your circumstances honestly and request a hardship plan or a temporary reduction in your minimum payment. Providing supporting documentation, like medical bills or unemployment paperwork, can strengthen your case. Remember, most credit card companies are more willing to work with customers who demonstrate good faith and a commitment to repayment.

Key Factors to Consider When Claiming Financial Hardship:

- Documentation: Gather all necessary documentation to support your claim of financial hardship.

- Honesty and Transparency: Be honest and transparent with the credit card company about your situation.

- Proposed Repayment Plan: Provide a realistic plan for repaying your debt once your financial situation improves.

Risks and Mitigations of Lowering Minimum Payments:

While a lower minimum payment offers short-term relief, it's crucial to acknowledge the risks:

- Increased Interest Paid: Extending the repayment period leads to paying significantly more interest over time.

- Negative Impact on Credit Score: Consistent minimum payments, even if lower, can still help maintain a good credit score, but missing payments can seriously damage it.

- Prolonged Debt: A lower minimum payment may prolong your debt burden, hindering your financial progress.

Mitigation Strategies:

- Develop a Realistic Budget: Create a detailed budget to ensure you can comfortably make your payments, even if they are lower.

- Set a Higher Payment Goal: Aim to pay more than the minimum payment whenever possible to accelerate debt reduction.

- Monitor Your Credit Score: Regularly check your credit report to track your credit score's health.

Further Analysis: Examining Financial Literacy and Responsible Credit Card Use

Financial literacy plays a vital role in managing credit card debt effectively. Understanding interest rates, minimum payments, and the implications of missed payments is crucial for making informed decisions. Responsible credit card use involves spending within your means, paying bills on time, and maintaining a low credit utilization ratio.

FAQ Section:

Q: What happens if I can't make even the reduced minimum payment? A: Contact your credit card issuer immediately to discuss your options. They may offer further assistance, such as a hardship plan or temporary suspension of payments. However, continued missed payments will negatively impact your credit score.

Q: Can I negotiate a lower minimum payment on all my credit cards? A: You can try to negotiate with each credit card issuer individually. However, success depends on your credit score, payment history, and the specific terms of each card.

Q: Will negotiating a lower minimum payment hurt my credit score? A: Negotiating itself shouldn't directly hurt your credit score, but consistently making only the minimum payment – even a lower one – can signal financial instability and may negatively affect your score over time.

Practical Tips: Maximizing the Benefits of a Negotiated Lower Minimum Payment:

- Create a Detailed Budget: Track your income and expenses to ensure you can afford the reduced minimum payment consistently.

- Set Up Automatic Payments: Schedule automatic payments to avoid late fees and maintain a positive payment history.

- Explore Additional Income Sources: Consider part-time jobs or selling unused items to generate extra income for debt repayment.

Final Conclusion:

Negotiating a lower minimum payment on your credit card can provide short-term relief, but it requires careful planning and a strategic approach. It's crucial to understand the implications, explore all available options, and develop a realistic plan for paying off your debt. Prioritize financial literacy, responsible credit card use, and building a strong credit history to avoid future financial challenges. Remember that while a lower minimum payment may offer breathing room, the ultimate goal is to eliminate the debt completely.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On Home Depot Credit Card

Apr 05, 2025

-

What Is The Minimum Wage For Home Depot

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How To Get Lower Minimum Payment On Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.