How To Figure Minimum Payment On Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Unveiling the Mystery: How to Calculate Your Credit Card Minimum Payment

What if understanding your credit card minimum payment could save you thousands of dollars in interest? Mastering this seemingly simple calculation is key to responsible credit card management and financial freedom.

Editor’s Note: This comprehensive guide to calculating your credit card minimum payment was published today, providing you with the most up-to-date information and strategies for effective debt management.

Why Understanding Your Minimum Payment Matters

Understanding your credit card minimum payment isn't just about meeting a monthly obligation; it's about navigating the complex world of credit responsibly. Failing to grasp this fundamental concept can lead to spiraling debt, significant interest accrual, and damage to your credit score. This knowledge empowers you to make informed decisions, budget effectively, and ultimately, take control of your finances. Understanding your minimum payment allows for better financial planning, proactive debt reduction strategies, and a clearer picture of your overall financial health. This knowledge is vital for both those with low balances and those struggling with high-interest debt.

Overview: What This Article Covers

This article provides a detailed breakdown of how minimum credit card payments are calculated, exploring various methods used by different issuers. We'll delve into the factors influencing the minimum payment, the potential pitfalls of only paying the minimum, and strategies for effectively managing your credit card debt. We'll also address frequently asked questions and offer practical tips to help you optimize your payment strategy.

The Research and Effort Behind the Insights

This article is the result of extensive research, drawing upon information from major credit card companies' terms and conditions, financial regulatory websites, and consumer finance experts. The information presented here is intended to provide an accurate and comprehensive understanding of minimum payment calculations and their implications.

Key Takeaways:

- Definition of Minimum Payment: Understanding the different components that comprise a minimum payment.

- Calculation Methods: Exploring the various methods used by credit card issuers to determine the minimum amount due.

- Factors Affecting Minimum Payment: Identifying the variables that influence the minimum payment calculation.

- Consequences of Only Paying the Minimum: Highlighting the long-term financial implications of minimal payments.

- Strategies for Effective Debt Management: Providing actionable steps to manage credit card debt effectively.

Smooth Transition to the Core Discussion

Now that we understand the importance of comprehending your minimum payment, let's dive into the mechanics of its calculation and explore effective strategies for managing credit card debt.

Exploring the Key Aspects of Minimum Payment Calculation

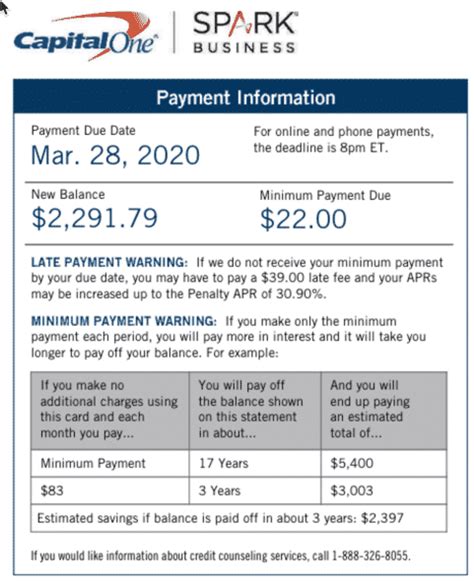

The minimum payment on a credit card is the smallest amount you can pay each month without incurring late fees or negatively impacting your credit score. However, the calculation isn't standardized across all credit card issuers. Several methods are employed, and understanding these methods is crucial for responsible credit card management.

1. Definition and Core Concepts:

The minimum payment typically consists of a combination of factors, which might include:

- Interest Accrued: The interest charged on your outstanding balance. This is calculated based on your Annual Percentage Rate (APR) and the average daily balance.

- Principal Payment: A portion of your outstanding balance (the actual amount you borrowed). This is the part that reduces your overall debt.

- Fees: Any fees charged during the billing cycle (e.g., late fees, annual fees, over-limit fees).

2. Applications Across Industries:

While the fundamental principle remains consistent, the specific calculation methods may vary slightly depending on the credit card issuer. Some common approaches include:

- Percentage of Balance: A common method is to set the minimum payment as a fixed percentage of your outstanding balance (typically 1% to 3%). For example, if your balance is $1,000 and the minimum payment percentage is 2%, your minimum payment would be $20.

- Fixed Minimum Payment: Some credit card companies may have a fixed minimum payment amount, regardless of your balance. This is less common, particularly for balances above a certain threshold.

- Combination Method: Many issuers use a combination of the percentage of balance and a fixed minimum payment. For example, the minimum payment might be the greater of 2% of the balance or a fixed amount like $25.

3. Challenges and Solutions:

One of the primary challenges with understanding the minimum payment is the lack of transparency from some credit card issuers. The calculation method may not be explicitly stated, making it difficult to independently verify the minimum payment amount. Furthermore, a low minimum payment can lull cardholders into a false sense of security, leading to prolonged debt and significant interest charges.

4. Impact on Innovation:

The increasing reliance on digital banking and online portals is leading to greater transparency in minimum payment calculations. Many credit card companies now provide detailed breakdowns of the minimum payment components online, empowering consumers to better understand their monthly obligations.

Closing Insights: Summarizing the Core Discussion

Understanding your minimum payment isn't just about avoiding late fees; it's about making informed decisions about your debt management. By comprehending the different calculation methods and the factors involved, you can develop a more effective repayment strategy.

Exploring the Connection Between APR and Minimum Payment

The Annual Percentage Rate (APR) plays a pivotal role in determining your minimum payment, especially the interest component. A higher APR leads to higher interest charges, which in turn influences the minimum payment. This connection is critical for understanding the long-term financial implications of only making minimum payments.

Key Factors to Consider:

- Roles and Real-World Examples: A higher APR results in a larger interest component of your minimum payment, leaving less money to pay down the principal balance. For instance, if you have a $1,000 balance and a 20% APR, a significant portion of your minimum payment will go towards interest, potentially delaying debt payoff significantly.

- Risks and Mitigations: Relying solely on minimum payments with a high APR can lead to a debt trap, where interest charges continuously outweigh the principal repayment, lengthening the repayment period and increasing the total cost of borrowing. Mitigation strategies include paying more than the minimum payment each month, seeking balance transfer options with lower APRs, or debt consolidation.

- Impact and Implications: The cumulative impact of high APRs and minimum payments can have severe long-term financial consequences, potentially delaying major financial goals like homeownership or retirement savings.

Conclusion: Reinforcing the Connection

The interplay between APR and minimum payment highlights the importance of carefully examining your credit card terms and conditions and actively seeking ways to reduce your APR whenever possible.

Further Analysis: Examining APR in Greater Detail

APR isn't a static figure; it's influenced by several factors, including your credit score, the type of credit card, and the issuer's current lending practices. Understanding these factors can empower you to negotiate a lower APR, reducing your interest charges and ultimately lowering your minimum payment.

FAQ Section: Answering Common Questions About Minimum Payments

Q: What happens if I only pay the minimum payment? A: While you avoid late fees, you'll pay significantly more in interest over time, lengthening the repayment period and increasing your total cost.

Q: Can my minimum payment change each month? A: Yes, your minimum payment can fluctuate depending on your outstanding balance, interest charges, and any fees accrued.

Q: What if I can't afford even the minimum payment? A: Contact your credit card issuer immediately to discuss options, such as hardship programs or payment plans. Failing to make payments can severely damage your credit score.

Q: How can I calculate my minimum payment independently? A: While not always possible due to varying calculation methods, understanding the components (interest, principal, fees) and checking your statement for detailed breakdowns will help you estimate it.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payments

- Review your statement carefully: Analyze the breakdown of your minimum payment to understand the interest and principal components.

- Pay more than the minimum: Aim to pay at least the interest charged each month to avoid increasing your debt.

- Explore debt reduction strategies: Consider debt consolidation, balance transfers, or negotiating a lower APR with your issuer.

- Monitor your credit report: Regular checks ensure you catch any errors or inconsistencies in your credit card account.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding your credit card minimum payment is a cornerstone of responsible financial management. By actively engaging with your credit card statements, understanding the calculation methods, and actively pursuing strategies to pay down your debt, you can avoid the debt trap and achieve better financial health. The seemingly simple act of understanding your minimum payment can unlock significant long-term financial benefits.

Latest Posts

Latest Posts

-

Why Do Capital One Payments Take So Long

Apr 06, 2025

-

How Long Does Capital One Take To Process A Payment

Apr 06, 2025

-

How Long Do Capital One Payments Take

Apr 06, 2025

-

How Long Do Capital One Payments Take To Post

Apr 06, 2025

-

How Long Do Capital One Payments Take To Process

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about How To Figure Minimum Payment On Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.