How To Dispute A Late Payment On Experian

adminse

Apr 03, 2025 · 9 min read

Table of Contents

How to Dispute a Late Payment on Experian: A Comprehensive Guide

What if a single late payment unfairly impacts your credit score for years to come? Dispute it effectively and reclaim your financial standing.

Editor's Note: This article provides up-to-date information on disputing late payments reported to Experian. Credit reporting is a complex process, and while this guide offers comprehensive advice, individual situations may require additional support from credit counseling services or legal professionals.

Why Disputing a Late Payment on Experian Matters:

A single late payment can significantly lower your credit score, impacting your ability to secure loans, rent an apartment, or even get a job. Experian, one of the three major credit bureaus, plays a crucial role in compiling your credit report. Therefore, disputing an inaccurate or unjustly reported late payment on your Experian report is vital for protecting your financial health. Understanding the process and employing the right strategies can help you correct errors and improve your credit score. The consequences of inaction can be far-reaching, potentially costing you thousands of dollars in higher interest rates over time.

Overview: What This Article Covers:

This article will guide you through the entire process of disputing a late payment on your Experian credit report. We’ll cover understanding your credit report, identifying inaccuracies, crafting an effective dispute letter, submitting your dispute, monitoring the process, and understanding your rights. We'll also explore the nuances of different types of late payments and potential obstacles you might encounter.

The Research and Effort Behind the Insights:

This article is the product of extensive research, incorporating information from the Fair Credit Reporting Act (FCRA), Experian's official website, and reputable consumer finance sources. We have analyzed various dispute strategies and success stories to provide you with the most effective and up-to-date information available.

Key Takeaways:

- Understanding Your Credit Report: Knowing what information is on your report is the first step.

- Identifying Inaccuracies: Pinpoint the specific late payment you need to dispute.

- Crafting a Strong Dispute Letter: A well-written letter significantly increases your chances of success.

- Submitting Your Dispute: Follow Experian’s official procedures for submitting your dispute.

- Monitoring the Process: Track the progress of your dispute and follow up as needed.

- Understanding Your Rights: Know your rights under the FCRA and how to protect them.

Smooth Transition to the Core Discussion:

Now that we've established the importance of disputing inaccurate late payments, let's delve into the step-by-step process of successfully challenging a late payment on your Experian report.

Exploring the Key Aspects of Disputing a Late Payment on Experian:

1. Understanding Your Experian Credit Report:

Before initiating a dispute, obtain a copy of your Experian credit report. You can obtain this for free annually through AnnualCreditReport.com (this website is the only authorized source for free credit reports; beware of scams). Carefully review the report, paying close attention to the section detailing your payment history. Note the date of the late payment, the creditor who reported it, and the amount. Any discrepancies between your records and the report should be investigated.

2. Identifying Inaccuracies:

There are several reasons why a late payment might be inaccurate:

- The payment was made on time: You have proof (bank statements, canceled checks, online payment confirmations) showing timely payment.

- The account is incorrect: The account number or creditor name is wrong.

- The amount is incorrect: The reported amount differs from your records.

- The date is incorrect: The date of the late payment is wrong.

- The account was settled or paid in full: The account should not be reflecting a late payment after settlement.

- The account was never yours: The account was opened fraudulently in your name.

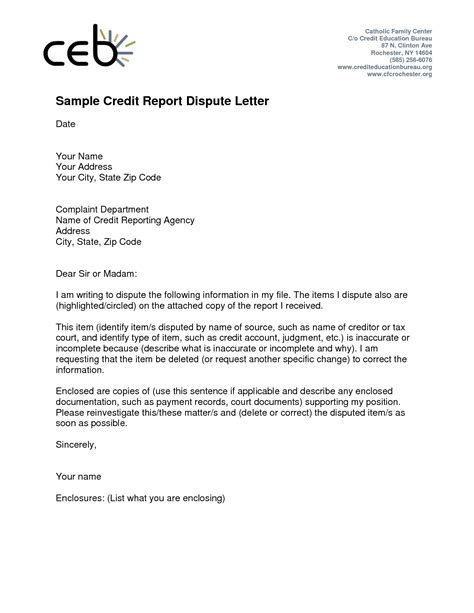

3. Crafting a Strong Dispute Letter:

Your dispute letter is your primary tool. Keep it concise, professional, and factual. Include the following:

- Your personal information: Full name, address, phone number, and Social Security number.

- Account information: The creditor's name, account number, and the specific late payment you're disputing.

- Specific details of the inaccuracy: Clearly explain why the late payment is inaccurate and provide supporting documentation.

- Your request: Clearly state that you are requesting the removal of the inaccurate late payment from your Experian report.

- Supporting documentation: Include copies of bank statements, canceled checks, payment confirmations, or any other evidence supporting your claim. Send certified mail with a return receipt requested for proof of delivery.

Example Dispute Letter:

[Your Name] [Your Address] [Your Phone Number] [Your Email Address]

[Date]

Experian P.O. Box 9554 Allen, TX 75013

Subject: Dispute of Inaccurate Late Payment – Account [Account Number]

Dear Experian Dispute Department,

This letter is to formally dispute a late payment reported on my Experian credit report for account number [Account Number] with [Creditor Name]. The reported late payment is dated [Date of Late Payment], and the amount is [Amount].

I am disputing this late payment because [Clearly explain the reason, e.g., "I made a payment on [Date of Payment] as evidenced by the attached bank statement," or "This account is not mine," etc.]. I have attached supporting documentation to prove my claim.

I request that you investigate this matter thoroughly and remove the inaccurate late payment from my credit report. I look forward to your prompt response and resolution to this issue.

Sincerely, [Your Signature] [Your Typed Name]

4. Submitting Your Dispute:

Experian offers multiple ways to submit your dispute:

- Mail: Send your dispute letter and supporting documentation via certified mail with a return receipt requested to the address specified on their website.

- Online: Some methods of dispute may be available online through your Experian account. Check their website for the most up-to-date options.

- Phone: While less reliable for complex disputes, you may be able to initiate a dispute over the phone.

5. Monitoring the Process:

After submitting your dispute, Experian has 30 days to investigate. You should receive a written response within this timeframe, outlining their findings. If the late payment is removed, your credit score should reflect this change within a few weeks. If the dispute is denied, you can re-submit your dispute with additional evidence, or consider further action (see below).

6. Understanding Your Rights under the Fair Credit Reporting Act (FCRA):

The FCRA protects consumers' rights regarding their credit reports. Under the FCRA, you have the right to dispute inaccurate information, and credit bureaus are obligated to investigate your claims. If Experian fails to properly investigate your dispute or if they fail to correct an inaccuracy, you may have legal recourse.

Exploring the Connection Between Account Types and Disputing Late Payments:

The process of disputing a late payment varies slightly depending on the type of account. For example, disputing a late payment on a credit card account involves providing evidence of timely payments, while disputing a late payment on a medical bill might require proof of payment arrangements or financial hardship. Similarly, disputing a late payment on a student loan requires different documentation and understanding of the loan's terms.

Key Factors to Consider:

Roles and Real-World Examples:

- Credit card late payment: A consumer paid their credit card bill a few days late due to an oversight. They dispute this late payment with their bank statement showing the payment, eventually getting the late payment removed from Experian.

- Medical bill late payment: A consumer had difficulty affording a medical bill and worked out a payment plan with the provider. They dispute a late payment reflecting before the payment plan was established and successfully removed it after providing documentation of the agreement.

- Student loan late payment: A consumer experienced an unforeseen financial hardship that led to a late payment on their student loan. They provide evidence of the hardship to successfully remove the late payment.

Risks and Mitigations:

- Insufficient evidence: Gathering and presenting robust evidence is crucial. Lack of documentation can lead to a denied dispute. Mitigation: Maintain thorough financial records.

- Incorrect procedures: Failing to follow Experian's dispute procedures can result in delays or rejection. Mitigation: Carefully review Experian's instructions and guidelines.

- Time constraints: Missing deadlines can hinder your dispute. Mitigation: Stay organized and keep track of deadlines.

Impact and Implications:

Successfully disputing an inaccurate late payment can significantly improve your credit score, unlocking opportunities for better loan terms, lower interest rates, and improved financial standing. Failure to dispute inaccurate information can lead to persistent negative marks on your credit report, hindering your financial future.

Conclusion: Reinforcing the Connection:

Dispute a late payment on Experian efficiently and effectively by following the detailed steps laid out in this guide. Remember, the key to success lies in preparing a meticulously detailed dispute letter and gathering strong supporting evidence. By understanding your rights under the FCRA and diligently following up, you significantly improve your chances of a successful outcome, reclaiming your creditworthiness and financial well-being.

Further Analysis: Examining the Role of Documentation in Greater Detail:

Thorough documentation is the cornerstone of a successful dispute. This includes not only bank statements and payment confirmations but also any communication with the creditor regarding the payment, including emails, letters, or phone call records. The more detailed and comprehensive your documentation, the stronger your case.

FAQ Section: Answering Common Questions About Disputing Late Payments on Experian:

Q: How long does it take for Experian to resolve a dispute? A: Experian typically has 30 days to investigate and respond to your dispute.

Q: What if Experian denies my dispute? A: You can re-submit your dispute with additional evidence or consider seeking assistance from a credit repair company or a legal professional.

Q: Can I dispute multiple late payments at once? A: Yes, you can, but it's often better to address each late payment individually for clarity and organization.

Q: What if the late payment is accurate? A: If the late payment is accurate, disputing it is unlikely to be successful. Focus on improving your payment habits going forward.

Practical Tips: Maximizing the Benefits of Disputing Late Payments:

- Act promptly: The sooner you dispute the late payment, the better.

- Keep meticulous records: Maintain organized financial records, including bank statements, payment confirmations, and communication with creditors.

- Be persistent: If your initial dispute is denied, don't give up. Re-submit your dispute with additional evidence.

- Consider professional help: If you're struggling to resolve the dispute yourself, consider seeking assistance from a credit repair company or a legal professional.

Final Conclusion: Wrapping Up with Lasting Insights:

Successfully disputing inaccurate late payments on your Experian credit report can have a profound and positive impact on your financial life. By understanding the process, gathering strong evidence, and following the advice outlined in this article, you can proactively protect your credit score and secure a brighter financial future. Remember, proactive credit management and accurate reporting are key to maintaining a strong financial profile.

Latest Posts

Latest Posts

-

What Is The Penalty For Late Electricity Bill Payment

Apr 04, 2025

-

What Is The Grace Period For Electric Bill

Apr 04, 2025

-

Apa Itu Liquidity Pool

Apr 04, 2025

-

What Is Liquidity Pool

Apr 04, 2025

-

Liquidity Pool Crypto Adalah

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about How To Dispute A Late Payment On Experian . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.