How To Dispute A Late Payment On Equifax

adminse

Apr 03, 2025 · 7 min read

Table of Contents

How to Dispute a Late Payment on Equifax: A Comprehensive Guide

What if a simple error on your credit report could cost you thousands of dollars in higher interest rates? Disputing inaccurate late payment information on your Equifax report is crucial for protecting your financial future.

Editor’s Note: This article on disputing late payments on your Equifax credit report was published today and provides up-to-date information and strategies for effectively resolving credit reporting inaccuracies.

Why Disputing a Late Payment on Equifax Matters:

A single late payment can significantly impact your credit score, potentially leading to higher interest rates on loans, credit card applications denials, and difficulty securing favorable terms on rental agreements or insurance policies. Equifax, one of the three major credit bureaus, plays a vital role in compiling and disseminating your credit information to lenders and other businesses. An inaccurate late payment listing on your Equifax report can negatively affect your financial life for years to come. Therefore, understanding how to effectively dispute such inaccuracies is paramount. The process is not always straightforward, but with the right approach and documentation, you can significantly increase your chances of a successful resolution.

Overview: What This Article Covers:

This article provides a step-by-step guide to disputing a late payment reported on your Equifax credit report. It will cover understanding the dispute process, gathering necessary documentation, crafting a compelling dispute letter, and navigating the potential outcomes. Readers will gain actionable insights, supported by practical examples and expert advice.

The Research and Effort Behind the Insights:

This article is the result of extensive research, incorporating best practices from consumer advocacy groups, legal resources, and analysis of Equifax's dispute process. The information presented is intended to be comprehensive and accurate, helping readers navigate the complexities of credit reporting disputes.

Key Takeaways:

- Understanding the Dispute Process: Familiarize yourself with Equifax’s procedures and timelines.

- Gathering Supporting Documentation: Compile evidence to support your claim of inaccuracy.

- Crafting a Strong Dispute Letter: Write a clear, concise, and persuasive letter.

- Following Up and Monitoring Progress: Track your dispute and ensure timely resolution.

- Understanding Your Rights: Know your legal rights under the Fair Credit Reporting Act (FCRA).

Smooth Transition to the Core Discussion:

Now that we understand the importance of disputing inaccurate late payments, let's delve into the specifics of how to effectively navigate the Equifax dispute process.

Exploring the Key Aspects of Disputing a Late Payment on Equifax:

1. Verification of the Inaccuracy:

Before initiating a dispute, carefully review your Equifax credit report. Identify the specific late payment you wish to challenge. Verify the details: the creditor, the date of the late payment, and the amount. Compare this information to your own records – bank statements, payment confirmations, or credit card statements. Any discrepancies are potential grounds for a dispute.

2. Gathering Necessary Documentation:

Strong documentation is crucial for a successful dispute. Gather evidence supporting your claim. This might include:

- Proof of Payment: Bank statements, canceled checks, money order receipts, online payment confirmations, or credit card statements showing timely payments.

- Correspondence with the Creditor: Letters, emails, or other communications demonstrating your attempts to resolve the issue with the creditor directly.

- Debt Agreement Documents: If you have a debt settlement agreement, include this to demonstrate a resolution.

- Copies of your Credit Report: Include a copy of the Equifax report showing the inaccurate late payment.

3. Crafting a Compelling Dispute Letter:

Your dispute letter should be formal, clear, concise, and persuasive. Include the following information:

- Your Personal Information: Full name, address, phone number, Social Security number, and Equifax account number (if applicable).

- The Inaccurate Information: Specifically identify the late payment you are disputing, including the creditor's name, the date of the alleged late payment, and the amount.

- Supporting Evidence: Clearly explain why the information is incorrect and provide detailed supporting evidence. Reference the documents you are including.

- Your Request: Clearly state your request – that Equifax remove the inaccurate late payment from your credit report.

- Your Contact Information: Provide updated contact information where Equifax can reach you.

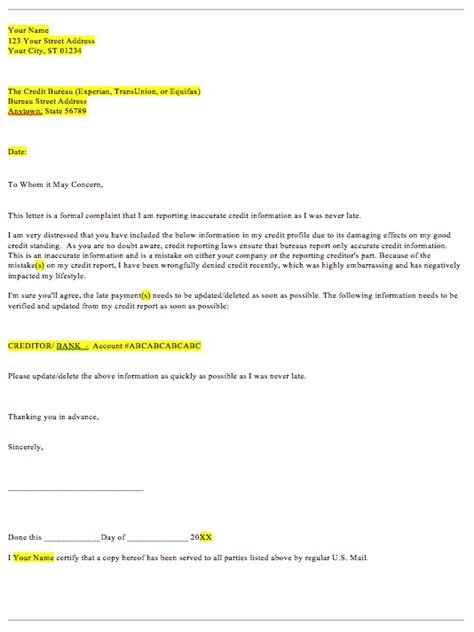

Example Dispute Letter:

[Your Name] [Your Address] [Your Phone Number] [Your Email Address]

[Date]

Equifax Dispute Department [Equifax Address]

Subject: Dispute of Inaccurate Late Payment – Account [Account Number]

Dear Equifax Dispute Department,

This letter is to formally dispute an inaccurate late payment reported on my Equifax credit report. The inaccurate information pertains to an account with [Creditor Name], account number [Account Number]. The report indicates a late payment of $[Amount] on [Date].

I am enclosing copies of [List Supporting Documents: e.g., bank statement showing on-time payment, payment confirmation email]. These documents clearly demonstrate that the payment was made on [Date of Payment], well within the due date.

I request that you investigate this matter thoroughly and remove the inaccurate late payment from my credit report. I look forward to your prompt response and resolution.

Sincerely,

[Your Signature] [Your Typed Name]

4. Submitting Your Dispute:

Equifax offers several ways to submit your dispute:

- Online: Through their website's dispute portal.

- Mail: By mailing a letter to their designated address (found on their website).

- Phone: While less common, some circumstances might allow for a phone dispute.

5. Following Up and Monitoring Progress:

After submitting your dispute, keep a record of the date and method of submission. Equifax has a timeframe (usually 30 days) to investigate. Follow up if you don't hear back within this timeframe. You can also monitor your Equifax report regularly to see if the inaccurate information has been removed.

Exploring the Connection Between Credit Repair Services and Disputing Late Payments:

Credit repair services can assist with the dispute process, but proceed with caution. Some services may charge exorbitant fees, and you can often handle the dispute yourself. Understanding the FCRA and following the steps outlined above can save you money and empower you to directly manage your credit report's accuracy.

Key Factors to Consider:

-

Roles and Real-World Examples: Credit repair companies may streamline the process, but they don't guarantee success, and DIY methods can often be effective with proper documentation. A real-world example is someone successfully disputing a late payment using bank statements as evidence.

-

Risks and Mitigations: The risk is a delayed or unsuccessful dispute. Mitigation involves meticulous documentation, a well-written letter, and consistent follow-up.

-

Impact and Implications: A successful dispute can significantly improve your credit score, while an unsuccessful one might necessitate additional steps, such as contacting the creditor directly or pursuing legal action.

Conclusion: Reinforcing the Connection:

The connection between understanding the dispute process and successfully removing an inaccurate late payment is vital. By proactively gathering evidence, crafting a compelling letter, and diligently following up, individuals can positively impact their credit score and overall financial well-being.

Further Analysis: Examining the Fair Credit Reporting Act (FCRA) in Greater Detail:

The FCRA protects consumers' rights regarding credit reports. It mandates that credit bureaus investigate disputes and correct inaccurate information. Understanding your rights under the FCRA empowers you to effectively navigate the dispute process.

FAQ Section: Answering Common Questions About Disputing Late Payments on Equifax:

Q: How long does it take Equifax to resolve a dispute?

A: Equifax typically has 30 days to investigate and respond.

Q: What if Equifax doesn't remove the late payment?

A: You can file a complaint with the Consumer Financial Protection Bureau (CFPB) or consider legal action.

Q: Can I dispute multiple late payments simultaneously?

A: Yes, you can submit separate disputes for each inaccurate late payment.

Q: Is there a fee to dispute a late payment?

A: No, Equifax is required by the FCRA to investigate disputes without charging a fee.

Practical Tips: Maximizing the Benefits of Disputing Inaccurate Late Payments:

- Act Quickly: Address inaccuracies promptly.

- Keep Detailed Records: Maintain thorough documentation.

- Follow Up Consistently: Track your dispute's progress.

- Understand Your Rights: Familiarize yourself with the FCRA.

Final Conclusion: Wrapping Up with Lasting Insights:

Disputing inaccurate late payments on your Equifax report is a critical step in protecting your creditworthiness. By understanding the process, gathering appropriate documentation, and crafting a persuasive dispute letter, you can significantly improve your chances of a successful outcome and safeguard your financial future. Don't let an inaccurate late payment negatively impact your credit score – take control and fight for your financial well-being.

Latest Posts

Latest Posts

-

What Is The Penalty For Late Payment Of Electricity Bill In Up

Apr 04, 2025

-

What Is The Penalty For Late Electricity Bill Payment

Apr 04, 2025

-

What Is The Grace Period For Electric Bill

Apr 04, 2025

-

Apa Itu Liquidity Pool

Apr 04, 2025

-

What Is Liquidity Pool

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about How To Dispute A Late Payment On Equifax . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.