How To Dispute A Late Fee On Credit Card

adminse

Apr 03, 2025 · 9 min read

Table of Contents

How to Dispute a Late Fee on Your Credit Card: A Comprehensive Guide

What if a simple mistake could cost you significantly more than it should? Disputing late fees on your credit card is often possible, saving you money and protecting your credit score.

Editor's Note: This article provides up-to-date information on disputing late credit card fees. While the steps are generally consistent, specific procedures may vary slightly depending on your card issuer. Always refer to your cardholder agreement and contact your issuer directly for the most accurate and current information.

Why Disputing Late Fees Matters:

Late fees are a significant source of revenue for credit card companies. While they serve as a deterrent for late payments, the fees can be substantial, ranging from $25 to $40 or more, depending on the issuer and your card type. Accumulating these fees can quickly impact your finances and negatively affect your credit score. Disputing a late fee, when justified, can save you considerable money and prevent unnecessary damage to your credit report. Moreover, successfully disputing a fee can potentially highlight systemic issues with your credit card provider’s billing practices, leading to improvements for all consumers.

Overview: What This Article Covers

This article will guide you through the entire process of disputing a late fee on your credit card. We will explore:

- Understanding late payment policies and the reasons for late fees.

- Identifying valid reasons to dispute a late fee.

- Gathering the necessary documentation to support your dispute.

- The steps involved in formally disputing the fee with your credit card issuer.

- Understanding your rights and what to expect during the dispute process.

- Alternative dispute resolution options if your initial dispute is unsuccessful.

- Preventing future late fees.

The Research and Effort Behind the Insights

This article draws upon extensive research, including analysis of credit card agreements from various major issuers, consumer protection laws, and advice from financial experts. The information presented is designed to empower consumers with the knowledge and tools needed to navigate the process effectively.

Key Takeaways:

- Understand your cardholder agreement: This is the crucial document outlining your rights and obligations regarding late fees.

- Act quickly: Most issuers have deadlines for disputing fees.

- Document everything: Keep records of all communication, payments, and relevant dates.

- Be polite and persistent: A professional and courteous approach can significantly improve your chances of a successful dispute.

- Consider alternative dispute resolution: If the issuer refuses your claim, there are other avenues to pursue.

Smooth Transition to the Core Discussion:

Now that we understand the importance of disputing unjust late fees, let's delve into the specifics of how to do so effectively.

Exploring the Key Aspects of Disputing Late Fees

1. Understanding Late Payment Policies:

Before disputing a fee, thoroughly review your credit card agreement. This document clearly outlines your card issuer's late payment policy, including the grace period (the time between the statement closing date and the due date), the calculation of late fees, and the process for disputing them. Pay close attention to the specific language used and the deadlines for submitting a dispute.

2. Valid Reasons to Dispute a Late Fee:

Several legitimate reasons may justify disputing a late fee. These include:

- Technical glitches: A payment made on time may not have been processed due to technical issues on the issuer's end. You need proof of attempted payment, such as a bank statement showing the transaction was initiated before the due date.

- Billing errors: Incorrect due dates, inaccurate balances, or processing delays by the credit card company can lead to unintentional late payments.

- Natural disasters or unforeseen circumstances: In cases of extreme circumstances like severe weather events or personal emergencies that prevented timely payment, the issuer may be more lenient. However, this requires strong supporting documentation.

- Mail delays: If you mailed your payment and can prove it was sent before the due date (certified mail with return receipt requested is highly recommended), a delay in postal service might be considered.

- Incorrect address on file: If your payment was returned due to an incorrect address on file with the credit card company and you have proof of providing the correct address, you can dispute the fee.

3. Gathering Necessary Documentation:

Before initiating a dispute, gather all relevant documentation, including:

- Your credit card statement: This shows the date of the late payment and the amount of the fee.

- Proof of payment: This could be a bank statement, canceled check, money order receipt, or online payment confirmation. If you paid by mail, retain proof of mailing with tracking information if possible.

- Communication records: Keep copies of all emails, letters, or phone call notes related to your payment.

- Supporting documentation: If your reason for dispute involves exceptional circumstances, gather supporting documentation like a police report (for theft), medical bills (for illness), or a natural disaster declaration.

4. Steps to Dispute a Late Fee:

Most credit card issuers have a formal dispute process. Typically, this involves:

- Contacting customer service: Call the number on the back of your credit card and explain your situation clearly and politely. Request that the late fee be removed. Keep detailed notes of this conversation, including the date, time, representative’s name, and any promises made.

- Submitting a written dispute: Many issuers prefer or require a written dispute. Send a formal letter (certified mail with return receipt requested is recommended) explaining the situation, providing all relevant documentation, and clearly stating your request for fee removal.

- Following up: After submitting your written dispute, follow up with a phone call after a reasonable timeframe (e.g., 1-2 weeks) to check on the status of your request.

5. Understanding Your Rights and Expectations:

The Fair Credit Billing Act (FCBA) protects consumers from inaccurate or unfair billing practices. Under the FCBA, you have the right to dispute billing errors, including late fees. However, the FCBA doesn't guarantee that your dispute will be successful. The issuer will investigate and make a decision based on the information you provide. Be prepared for the process to take several weeks.

6. Alternative Dispute Resolution Options:

If your initial dispute is unsuccessful, consider these alternative options:

- Escalating your complaint: Contact a higher-level representative within the credit card company.

- Filing a complaint with the CFPB: The Consumer Financial Protection Bureau (CFPB) handles consumer complaints against financial institutions. Filing a complaint with the CFPB can pressure the credit card issuer to reconsider your dispute.

- Seeking legal counsel: If the amount is significant, or you have a strong case, consulting with a consumer rights attorney might be beneficial.

7. Preventing Future Late Fees:

The best way to avoid late fees is to pay your credit card bills on time, every time. Consider these strategies:

- Set up automatic payments: This ensures your payment is made promptly each month.

- Use online bill pay: Many banks offer online bill pay services that allow you to schedule payments in advance.

- Set reminders: Use calendar reminders or smartphone apps to alert you about upcoming due dates.

- Pay early: Paying a few days early provides a buffer against potential delays.

- Track your spending: Monitor your spending throughout the month to avoid exceeding your credit limit and incurring potential late fees.

Exploring the Connection Between Timely Payment and Credit Score

Timely payments significantly impact your credit score. Missing payments and incurring late fees can severely damage your creditworthiness. A good credit score is essential for securing loans, mortgages, and even obtaining favorable insurance rates. The connection between timely payment and a strong credit score underscores the importance of preventing late payments and successfully disputing unjustified fees.

Key Factors to Consider:

- Roles: Timely payments are crucial for maintaining a high credit score and avoiding the financial burden of late fees. Conversely, consistent late payments have detrimental effects.

- Real-World Examples: Individuals with consistently excellent payment histories enjoy lower interest rates on loans and better financial opportunities, while those with poor payment histories face higher interest rates and limited access to credit.

- Risks and Mitigations: The risk of late payments is the negative impact on your credit score. Mitigations involve setting up automatic payments, using online bill pay, setting payment reminders and paying early.

- Impact and Implications: A strong credit score opens doors to numerous financial advantages, while a poor credit score limits financial opportunities.

Conclusion: Reinforcing the Connection:

The relationship between timely payments and a healthy credit score is undeniable. Preventing late payments through diligent financial management and successfully disputing unwarranted fees are essential for maintaining strong credit.

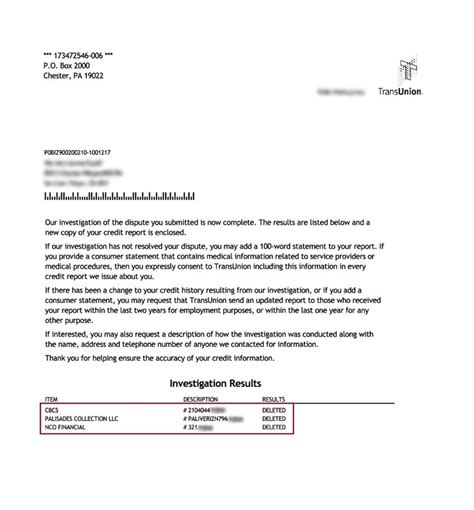

Further Analysis: Examining Credit Reporting Agencies in Greater Detail

Credit reporting agencies (like Equifax, Experian, and TransUnion) maintain records of your credit history. Late payments and associated late fees are reported to these agencies, impacting your credit score. Understanding how these agencies operate and how your payment history is reflected in your credit report is essential for managing your credit effectively.

FAQ Section: Answering Common Questions About Disputing Late Fees

- Q: What if my dispute is denied? A: Review the reason for denial and consider escalating your complaint or seeking alternative dispute resolution.

- Q: How long does the dispute process take? A: It typically takes several weeks.

- Q: Can I dispute a late fee after several months? A: Most issuers have deadlines; check your cardholder agreement.

- Q: What if I never received my statement? A: You should notify your credit card issuer immediately and explain the situation, providing evidence of attempted communication.

Practical Tips: Maximizing the Benefits of a Successful Dispute

- Keep meticulous records: This is your strongest defense.

- Act promptly: Don't delay in contacting your issuer.

- Be polite but firm: A professional approach is crucial.

- Use certified mail: This provides proof of delivery.

- Understand your rights: Familiarize yourself with the FCBA.

Final Conclusion: Wrapping Up with Lasting Insights

Disputing a late fee can be a daunting process, but knowing your rights and following the steps outlined in this article can significantly improve your chances of success. By understanding your cardholder agreement, acting promptly, and documenting everything meticulously, you can protect your finances and your credit score. Remember, prevention is key, so proactive payment strategies are crucial to avoid future late fees. Armed with this knowledge, you can navigate the complexities of credit card billing with confidence and protect yourself from unnecessary charges.

Latest Posts

Latest Posts

-

What Is The Penalty For Late Payment Of Electricity Bill In Up

Apr 04, 2025

-

What Is The Penalty For Late Electricity Bill Payment

Apr 04, 2025

-

What Is The Grace Period For Electric Bill

Apr 04, 2025

-

Apa Itu Liquidity Pool

Apr 04, 2025

-

What Is Liquidity Pool

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about How To Dispute A Late Fee On Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.