How To Calculate Minimum Monthly Payment On A Line Of Credit

adminse

Apr 05, 2025 · 7 min read

Table of Contents

Decoding the Minimum Payment: A Comprehensive Guide to Line of Credit Calculations

What if understanding your line of credit minimum payment could save you thousands over the life of your loan? Mastering this calculation empowers you to manage debt effectively and avoid costly interest accrual.

Editor’s Note: This article provides a detailed explanation of how minimum monthly payments on lines of credit are calculated, including various scenarios and practical tips for responsible debt management. The information presented is for educational purposes and should not be considered financial advice. Always consult with a financial professional for personalized guidance.

Why Understanding Minimum Payments Matters:

Understanding your line of credit's minimum monthly payment is crucial for several reasons. First, it helps you avoid late payment fees, which can significantly increase your overall cost. Second, it allows you to budget effectively, ensuring you can comfortably meet your financial obligations each month. Third, understanding the calculation helps you strategize repayment, accelerating the debt payoff and minimizing interest charges. Finally, it provides transparency into your financial situation, enabling informed decision-making about borrowing and spending habits. Minimum payments are often presented as a percentage of your outstanding balance, but understanding the underlying mathematics is key to responsible financial management.

Overview: What This Article Covers:

This article will comprehensively explore the methods used to calculate minimum payments on lines of credit. It will cover:

- The different methods lenders employ for calculating minimum payments.

- The impact of interest rates and outstanding balances on minimum payments.

- Factors influencing minimum payment calculations beyond the basic formula.

- Strategies for minimizing interest charges and accelerating debt repayment.

- Common misconceptions about minimum payments and their consequences.

- Practical examples illustrating the calculations in different scenarios.

- Frequently asked questions concerning minimum payments and line of credit management.

- Tips for managing your line of credit responsibly and avoiding financial pitfalls.

The Research and Effort Behind the Insights:

This article draws upon extensive research encompassing industry best practices, regulatory guidelines, and financial modeling techniques. Numerous examples and scenarios are provided to illustrate the concepts clearly and practically. The information is presented in an accessible and straightforward manner, enabling readers with varying levels of financial literacy to understand the complex calculations involved.

Key Takeaways:

- Understanding the Basics: Learn the fundamental principles behind minimum payment calculations for lines of credit.

- Practical Applications: Understand how the calculation works in real-world scenarios.

- Strategies for Repayment: Discover effective strategies to minimize interest charges and pay off debt faster.

- Avoiding Pitfalls: Learn to avoid common mistakes that can lead to increased debt burden.

Smooth Transition to the Core Discussion:

Now that we understand the importance of comprehending minimum payment calculations, let’s delve into the specifics of how these calculations are performed.

Exploring the Key Aspects of Line of Credit Minimum Payment Calculations:

Several methods exist for calculating the minimum payment on a line of credit. While the specific approach varies depending on the lender, the most common methods include:

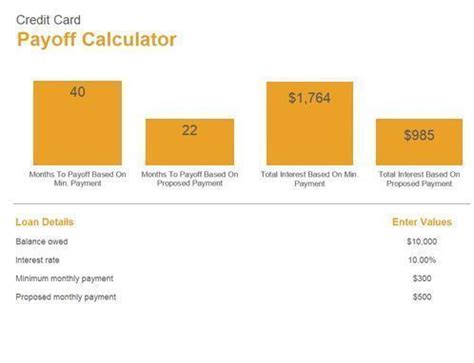

1. Percentage of Outstanding Balance: This is the most prevalent method. Lenders typically specify a minimum payment as a percentage of your outstanding balance (e.g., 1%, 2%, or even a higher percentage). For example, if your outstanding balance is $10,000 and the minimum payment is 2%, your minimum payment would be $200. This percentage can vary significantly, and it is crucial to review your credit agreement carefully. This method is straightforward but can lead to slow debt repayment if the interest rate is high.

2. Minimum Payment Plus Interest: Some lenders calculate the minimum payment as the accrued interest plus a small portion of the principal balance. This ensures that at least the interest accrued during the billing cycle is paid, preventing the debt from escalating rapidly. The percentage of the principal might be relatively low (e.g., 1%). If the interest accrued on a $10,000 balance is $50, and the minimum principal payment is 1% ($100), the minimum payment would be $150.

3. Fixed Minimum Payment: Some credit agreements may stipulate a fixed minimum payment regardless of the outstanding balance. This approach is less common for lines of credit but might be seen with some promotional offers or specific credit products. However, this fixed amount may not adequately cover the accrued interest, leading to a continuously increasing balance.

Exploring the Connection Between Interest Rates and Minimum Payments:

The interest rate applied to your line of credit significantly impacts your minimum payment, even if the minimum payment percentage remains constant. A higher interest rate means more interest accrues each month, potentially increasing your minimum payment (especially under the "Minimum Payment Plus Interest" method). This is because the interest component of the minimum payment will be larger. Conversely, a lower interest rate will lead to a smaller interest component, resulting in a lower minimum payment.

Key Factors to Consider:

Roles and Real-World Examples:

Imagine two individuals, both with a $10,000 line of credit. Individual A has a 10% interest rate and a 2% minimum payment requirement. Individual B has a 5% interest rate and the same 2% minimum payment requirement. While both have the same initial minimum payment ($200), Individual A's interest accrual will be significantly higher, potentially making it harder to reduce the principal balance despite making the minimum payment.

Risks and Mitigations:

Relying solely on minimum payments can lead to prolonged debt and substantial interest charges. This is known as "debt trap." To mitigate this, it's crucial to pay more than the minimum whenever possible. Setting a higher payment amount, even a small increase, can significantly reduce the overall cost and repayment time.

Impact and Implications:

The minimum payment calculation has far-reaching implications. Ignoring it can lead to delinquency, damaged credit scores, and potential legal action from lenders. Conversely, understanding and strategically managing minimum payments allows individuals to control their debt effectively and improve their financial well-being.

Conclusion: Reinforcing the Connection:

The relationship between interest rates, outstanding balances, and the chosen calculation method is crucial to comprehending your minimum payment. The higher the interest rate and the larger the outstanding balance, the more likely the minimum payment will mainly cover the interest accrued, making it difficult to reduce the principal.

Further Analysis: Examining Interest Calculation in Greater Detail:

Interest is typically calculated daily on the outstanding balance and compounded monthly. The daily interest rate is derived by dividing the annual interest rate by 365. The daily interest is then multiplied by the number of days in the billing cycle to get the total interest accrued. This interest is added to the outstanding balance, and the minimum payment is then calculated based on the updated balance and the lender’s chosen method.

FAQ Section: Answering Common Questions About Line of Credit Minimum Payments:

Q: What happens if I only pay the minimum payment? A: While you’ll avoid late fees, you will pay significantly more in interest over the life of the loan and it will take much longer to pay off the debt.

Q: Can I change my minimum payment amount? A: You cannot change the lender's calculated minimum payment, but you can always choose to pay more than the minimum.

Q: What if I miss a minimum payment? A: You’ll likely incur late payment fees, and your credit score will suffer. Your lender may also increase your interest rate.

Q: How can I calculate my minimum payment if the method isn't explicitly stated? A: Contact your lender directly; they are obligated to provide this information.

Practical Tips: Maximizing the Benefits of Understanding Your Minimum Payment:

- Review your credit agreement: Understand the exact method used to calculate your minimum payment.

- Track your payments: Monitor your balance regularly to see the impact of your payments.

- Pay more than the minimum: Even small increases can drastically shorten the repayment period.

- Consider a debt consolidation loan: If you have high-interest debt, this might be a better option.

- Budget effectively: Ensure you can afford your minimum payments each month, and aim for more.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding how your line of credit's minimum payment is calculated is fundamental to responsible debt management. By carefully reviewing your credit agreement, understanding the factors influencing the calculation, and making informed decisions about your payments, you can avoid the pitfalls of high interest charges and extended repayment periods. Take control of your finances by actively managing your line of credit and striving to pay more than the minimum whenever possible.

Latest Posts

Latest Posts

-

Minimum Mortgage Monthly Payment

Apr 05, 2025

-

Mortgage Minimum Amount

Apr 05, 2025

-

Minimum Payment On Mortgage

Apr 05, 2025

-

Home Loan Minimum Payment

Apr 05, 2025

-

Minimum Payment Chase

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How To Calculate Minimum Monthly Payment On A Line Of Credit . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.