How Long To Pay Off Dental School Loans

adminse

Mar 31, 2025 · 8 min read

Table of Contents

How Long Does It Take to Pay Off Dental School Loans? A Comprehensive Guide

How long will it realistically take to pay off the mountain of debt incurred during dental school?

Successfully navigating dental school loan repayment requires a strategic, proactive approach and a deep understanding of available options.

Editor’s Note: This article on dental school loan repayment was published today and provides up-to-date information on repayment strategies, loan forgiveness programs, and financial planning advice for dentists.

Why Dental School Loan Repayment Matters:

Dental school is a significant financial undertaking. The cost of tuition, fees, living expenses, and other related costs can easily accumulate into hundreds of thousands of dollars in debt. The length of time it takes to repay these loans significantly impacts a dentist's financial well-being, career choices, and overall lifestyle. Understanding various repayment strategies, available resources, and financial planning techniques is crucial for successful debt management and achieving long-term financial security. The impact extends beyond the individual, affecting professional satisfaction and the ability to invest in practice growth or community involvement.

Overview: What This Article Covers:

This article provides a comprehensive guide to dental school loan repayment, addressing key factors influencing repayment timelines, outlining different repayment plans, exploring loan forgiveness programs, and offering practical financial planning strategies. Readers will gain a clear understanding of the challenges involved, the potential solutions, and steps to create a personalized debt repayment plan.

The Research and Effort Behind the Insights:

This article is based on extensive research, incorporating data from the American Dental Association (ADA), the Association of American Medical Colleges (AAMC), government sources on student loan programs, and financial planning experts specializing in high-debt professions. We've analyzed various repayment scenarios, considered different income levels and debt amounts, and explored the implications of various repayment strategies. The goal is to provide readers with accurate, evidence-based information to make informed decisions.

Key Takeaways:

- Understanding Your Debt: A detailed breakdown of your loan types, interest rates, and total debt amount.

- Repayment Plan Options: Exploring the advantages and disadvantages of various federal and private loan repayment plans.

- Income-Driven Repayment (IDR) Plans: How these plans can adjust monthly payments based on your income and family size.

- Loan Forgiveness Programs: Eligibility requirements and limitations of programs like Public Service Loan Forgiveness (PSLF).

- Financial Planning Strategies: Budgeting, debt consolidation, and investment strategies for accelerated debt repayment.

- Negotiating with Loan Servicers: Strategies for potentially reducing interest rates or modifying repayment terms.

Smooth Transition to the Core Discussion:

Now that we understand the significance of effective dental school loan repayment, let's delve into the factors affecting repayment timelines and explore strategies for optimizing the repayment process.

Exploring the Key Aspects of Dental School Loan Repayment:

1. Understanding Your Debt:

Before strategizing repayment, thoroughly understand your debt profile. This includes:

- Loan Types: Federal (Stafford, Grad PLUS) and private loans carry different interest rates, repayment options, and eligibility for forgiveness programs. Identify each loan type and its associated terms.

- Interest Rates: High interest rates significantly prolong repayment. Know the interest rate for each loan.

- Total Debt Amount: Calculate the total principal amount owed across all loans.

- Loan Servicers: Understand who services each loan, as this determines who to contact for repayment adjustments.

2. Repayment Plan Options:

Several repayment plans are available, each with its pros and cons:

- Standard Repayment Plan: Fixed monthly payments over a 10-year period. This plan pays off the loan quickly but results in higher monthly payments.

- Extended Repayment Plan: Fixed monthly payments over a longer period (up to 25 years for federal loans). This reduces monthly payments but increases total interest paid.

- Graduated Repayment Plan: Payments start low and gradually increase over time. This offers lower initial payments but higher payments later.

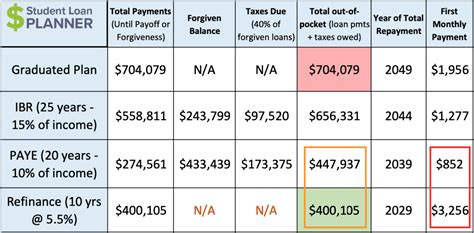

- Income-Driven Repayment (IDR) Plans: Monthly payments are calculated based on your discretionary income and family size. These plans include options like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE). IDR plans often result in loan forgiveness after 20 or 25 years, but the forgiven amount is considered taxable income.

3. Loan Forgiveness Programs:

Several programs may partially or fully forgive dental school loans, contingent on specific requirements:

- Public Service Loan Forgiveness (PSLF): Forgives remaining federal student loan debt after 120 qualifying monthly payments while employed full-time by a government or non-profit organization. Strict eligibility criteria apply.

- Teacher Loan Forgiveness: Forgives up to $17,500 of federal student loan debt for teachers who have completed five years of full-time teaching in low-income schools.

- State Loan Forgiveness Programs: Many states offer loan repayment assistance or forgiveness programs for dentists who practice in underserved areas. Eligibility varies by state.

4. Financial Planning Strategies:

Effective financial planning is crucial for accelerating loan repayment:

- Create a Realistic Budget: Track income and expenses meticulously to identify areas for savings.

- Prioritize High-Interest Debt: Focus on repaying loans with the highest interest rates first to minimize overall interest costs.

- Debt Consolidation: Consolidate multiple loans into a single loan with a lower interest rate, simplifying repayment.

- Consider Refinancing: Refinancing private loans may lower interest rates, shortening repayment.

- Automate Payments: Set up automatic payments to ensure consistent and timely repayments.

- Increase Income: Explore opportunities to increase income through additional work, consulting, or investing.

Exploring the Connection Between Income and Dental School Loan Repayment:

The relationship between a dentist's income and loan repayment is paramount. Higher income allows for larger monthly payments and faster repayment. However, even with a high income, careful financial planning is essential to avoid overspending and maintain a healthy financial balance.

Key Factors to Consider:

- Roles and Real-World Examples: A high-income specialist may repay loans significantly faster than a general dentist in a rural area with a lower income.

- Risks and Mitigations: High-income dentists face risks like lifestyle inflation, neglecting savings, and underestimating the long-term impact of high debt. Mitigations include budgeting, financial planning, and disciplined saving.

- Impact and Implications: Faster loan repayment frees up finances for investments, practice growth, and personal goals. Prolonged repayment can limit career choices, professional opportunities, and overall financial well-being.

Conclusion: Reinforcing the Connection:

The connection between income and dental school loan repayment highlights the importance of financial literacy and proactive planning. Understanding the earning potential of different dental specialties, practicing in diverse settings, and developing sound financial habits are crucial for effective debt management.

Further Analysis: Examining Income Potential in Dentistry

Dental specialties like orthodontics and oral surgery generally offer higher earning potential than general dentistry. This higher income can significantly impact loan repayment timelines. However, the increased earning potential often comes with a longer training period and potentially higher initial debt. Analyzing the income-to-debt ratio for various dental specialties provides a clearer picture of realistic repayment timelines.

FAQ Section: Answering Common Questions About Dental School Loan Repayment:

- Q: What is the average dental school loan debt? A: The average debt can vary significantly, but it's often in the range of $200,000 to $300,000 or more.

- Q: How long does it typically take to pay off dental school loans? A: This depends on several factors, including loan amount, interest rates, income, and chosen repayment plan. It can range from 10 years to 25 years or more.

- Q: What if I can't afford my monthly payments? A: Contact your loan servicer immediately to discuss options like forbearance, deferment, or an income-driven repayment plan.

- Q: Are there any resources to help with dental school loan repayment? A: Yes, the ADA, AAMC, and many state dental associations offer resources, workshops, and financial counseling.

- Q: Can I refinance my federal student loans? A: While you can't refinance federal student loans with private lenders, you can consolidate them into a Direct Consolidation Loan.

Practical Tips: Maximizing the Benefits of Effective Repayment Strategies:

- Step 1: Understand Your Loan Terms: Gather all loan documents and analyze the details of each loan.

- Step 2: Explore Repayment Plan Options: Carefully evaluate the pros and cons of each plan and choose one aligning with your financial situation.

- Step 3: Create a Detailed Budget: Track income, expenses, and debt repayment to visualize progress and identify areas for adjustment.

- Step 4: Prioritize High-Interest Debt: Focus on repaying loans with higher interest rates first to minimize the overall interest paid.

- Step 5: Explore Loan Forgiveness Programs: Determine eligibility for any applicable programs to potentially reduce or eliminate loan debt.

- Step 6: Regularly Review and Adjust: Financial situations change. Periodically review your repayment plan and make adjustments as needed.

Final Conclusion: Wrapping Up with Lasting Insights:

Successfully navigating dental school loan repayment requires a proactive, strategic approach. Understanding your debt, exploring repayment options, and implementing sound financial planning are crucial for minimizing the financial burden and ensuring long-term financial well-being. By combining financial literacy with personalized planning, dentists can achieve their financial goals while pursuing fulfilling careers. The journey may be challenging, but with careful planning and consistent effort, it's entirely possible to successfully manage dental school debt and achieve financial freedom.

Latest Posts

Latest Posts

-

What Are Mortgage Bonds

Apr 26, 2025

-

Narrow Basis Definition

Apr 26, 2025

-

Event Risk Definition

Apr 26, 2025

-

Buy Quote Definition

Apr 26, 2025

-

Closing Quote Definition

Apr 26, 2025

Related Post

Thank you for visiting our website which covers about How Long To Pay Off Dental School Loans . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.