How Does Credit Work In Mexico

adminse

Apr 04, 2025 · 9 min read

Table of Contents

Decoding Mexican Credit: A Comprehensive Guide

What if navigating the Mexican credit system was as easy as understanding a simple equation? This intricate yet vital financial landscape holds the key to economic empowerment for millions.

Editor’s Note: This article on how credit works in Mexico was published today, offering readers up-to-date insights into the country's evolving financial ecosystem. We've compiled information from reputable sources to provide a clear and comprehensive understanding of this important topic.

Why Mexican Credit Matters:

Understanding how credit functions in Mexico is crucial for both Mexican citizens and international businesses operating within the country. Access to credit fuels economic growth, enabling individuals to purchase homes, start businesses, and invest in education. For businesses, credit facilitates expansion, hiring, and overall operational efficiency. Moreover, a robust credit system is a cornerstone of a stable and thriving economy. The credit landscape in Mexico is dynamic, influenced by factors like government policies, technological advancements, and evolving consumer behavior. This understanding is vital for making informed financial decisions.

Overview: What This Article Covers:

This in-depth analysis will explore the multifaceted world of Mexican credit. We'll delve into the different types of credit available, the credit scoring systems used, the institutions involved, and the legal framework that governs it all. We will also address common challenges and offer practical advice for navigating the system effectively. Finally, we will explore the future of credit in Mexico and its potential impact on the economy.

The Research and Effort Behind the Insights:

This article is the culmination of extensive research, drawing upon reports from the Comisión Nacional Bancaria y de Valores (CNBV), the Mexican central bank (Banco de México), academic studies on the Mexican financial system, and analysis of industry trends. We have also consulted various consumer finance websites and consulted with financial experts to ensure accuracy and provide practical advice.

Key Takeaways:

- Definition and Core Concepts: A comprehensive overview of Mexican credit, its fundamental principles, and key terminology.

- Types of Credit: Exploration of various credit products available to consumers and businesses in Mexico, including credit cards, personal loans, mortgages, and business financing.

- Credit Scoring and Reporting: An in-depth look at the systems used to assess creditworthiness in Mexico and the implications for accessing credit.

- Institutions Involved: Understanding the role of banks, credit bureaus, and other financial institutions in the Mexican credit system.

- Legal Framework: An overview of the laws and regulations that govern credit in Mexico, safeguarding consumer rights and promoting fair lending practices.

- Challenges and Solutions: Addressing common hurdles faced by individuals and businesses seeking credit in Mexico, and providing practical solutions.

- Future Trends: Analyzing emerging trends in Mexican credit, including fintech innovations and their potential impact.

Smooth Transition to the Core Discussion:

Having established the importance of understanding Mexican credit, let's delve into its core components, beginning with the types of credit products available.

Exploring the Key Aspects of Mexican Credit:

1. Types of Credit Available in Mexico:

The Mexican credit market offers a diverse range of products catering to various needs:

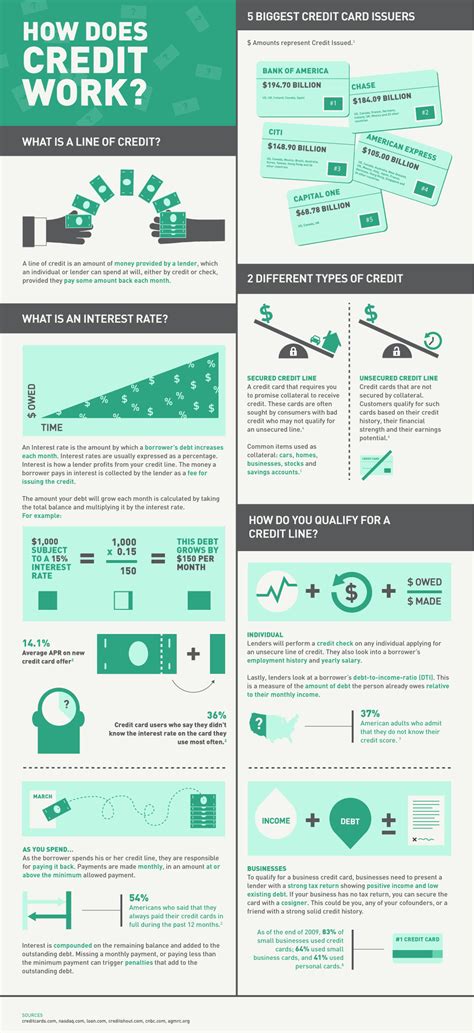

- Credit Cards: Widely used for everyday purchases, credit cards offer revolving credit with interest charges on outstanding balances. Different banks and financial institutions offer various features and reward programs. Credit limits are determined based on the applicant's credit history and income.

- Personal Loans: These unsecured loans are granted based on creditworthiness and are typically used for various purposes, such as debt consolidation, home improvements, or unexpected expenses. Repayment terms are fixed, with regular installments over a specified period.

- Mortgages (Hipotecas): Used to finance the purchase of real estate, mortgages are secured loans with the property serving as collateral. Mortgage rates and terms vary depending on the lender and the borrower's credit profile. The process can be lengthy, requiring extensive documentation and appraisal of the property.

- Auto Loans (Créditos Automotrices): Similar to mortgages, auto loans are secured loans used to purchase vehicles. The vehicle itself serves as collateral. Interest rates and repayment terms are typically fixed.

- Business Loans (Créditos Empresariales): Essential for small and medium-sized enterprises (SMEs), business loans can be used for working capital, expansion, equipment purchases, or other business-related expenses. Eligibility criteria are more stringent, requiring detailed financial statements and business plans. Access to these loans can significantly impact a business's growth trajectory.

- Microloans: Designed for individuals and micro-businesses with limited access to traditional banking services, microloans offer smaller amounts of credit with shorter repayment periods. These are often facilitated by microfinance institutions and NGOs.

2. Credit Scoring and Reporting in Mexico:

Creditworthiness in Mexico is assessed through credit bureaus (Sociedades de Información Crediticia – SICs). The two main SICs are:

- Buró de Crédito: The largest and most established credit bureau in Mexico.

- Círculo de Crédito: A newer player, but still a significant source of credit information.

These bureaus collect and maintain credit history data, including payment history, outstanding balances, and credit applications. They use this information to generate a credit score, which lenders use to assess the risk associated with extending credit to a borrower. A higher credit score typically indicates a lower risk, leading to better interest rates and easier access to credit. Maintaining a good credit score is paramount in Mexico, as it can significantly impact an individual's or business's financial opportunities.

3. Institutions Involved in the Mexican Credit System:

Several key players make up the Mexican credit system:

- Banks (Bancos): The primary lenders in Mexico, offering a wide range of credit products to individuals and businesses. They are regulated by the CNBV.

- Credit Unions (Uniones de Crédito): Cooperatively owned financial institutions that provide credit and other financial services to their members.

- Microfinance Institutions (Instituciones de Microfinanzas): Specialized institutions focusing on providing microloans to individuals and micro-businesses with limited access to traditional banking.

- Non-Bank Financial Institutions (NBFIs): These institutions offer various financial services, including credit, outside of the traditional banking system. Their activities are also regulated by the CNBV.

4. The Legal Framework Governing Credit in Mexico:

Mexican credit is governed by a comprehensive legal framework designed to protect consumers and promote responsible lending practices. Key laws include:

- Ley para la Transparencia y Ordenamiento de los Servicios Financieros (Law for the Transparency and Ordering of Financial Services): This law establishes regulations for financial institutions, promoting transparency and fair lending practices.

- Ley Federal de Protección al Consumidor (Federal Consumer Protection Law): This law protects consumers from unfair practices, including deceptive advertising and abusive lending terms.

- Código de Comercio (Commercial Code): This code provides the legal framework for commercial transactions, including credit agreements.

5. Challenges and Solutions:

Navigating the Mexican credit system can present challenges:

- Limited Access to Credit: Many individuals and SMEs lack access to credit due to limited credit history or stringent lending criteria. Solutions include the growth of microfinance institutions and alternative lending platforms.

- High Interest Rates: Interest rates on credit products can be high, especially for borrowers with poor credit scores. Solutions involve financial literacy programs and responsible borrowing habits.

- Bureaucracy and Lengthy Processes: Applying for credit can be a lengthy and bureaucratic process, requiring extensive documentation. Solutions involve streamlining processes and utilizing online platforms.

- Debt Management: Managing debt effectively can be challenging. Solutions include budgeting tools, debt consolidation options, and financial counseling services.

6. Future Trends in Mexican Credit:

Several trends are shaping the future of Mexican credit:

- Fintech Innovation: The rise of fintech companies is transforming access to credit, offering more convenient and efficient lending solutions.

- Digitalization: Increasingly, credit applications and management are conducted online, making the process faster and more accessible.

- Open Banking: The adoption of open banking principles will provide consumers with more control over their financial data and enhance competition among lenders.

- Government Initiatives: Government policies focused on financial inclusion and responsible lending will continue to influence the credit landscape.

Exploring the Connection Between Financial Literacy and Mexican Credit:

Financial literacy plays a pivotal role in shaping how individuals and businesses interact with the Mexican credit system. A lack of financial understanding can lead to irresponsible borrowing, high debt levels, and difficulty managing finances.

Key Factors to Consider:

- Roles and Real-World Examples: Financial literacy programs educate consumers about credit scores, interest rates, loan terms, and budgeting techniques, empowering them to make informed decisions. Many NGOs and government initiatives offer such programs.

- Risks and Mitigations: Without financial literacy, individuals are more vulnerable to predatory lending practices and high-interest debt traps. Financial education mitigates these risks.

- Impact and Implications: Improved financial literacy leads to better credit management, improved credit scores, and increased access to credit at favorable terms. This fosters economic empowerment and contributes to overall economic stability.

Conclusion: Reinforcing the Connection:

The interplay between financial literacy and Mexican credit is undeniable. By improving financial literacy, Mexico can enhance its credit system, leading to greater financial inclusion, economic growth, and improved living standards.

Further Analysis: Examining Fintech’s Impact in Greater Detail:

Fintech companies are disrupting the traditional Mexican credit landscape. They leverage technology to offer innovative solutions, often targeting underserved populations with limited access to traditional banking. These innovations include mobile lending platforms, peer-to-peer lending, and alternative credit scoring methods. This increased competition can lead to lower interest rates and broader access to credit.

FAQ Section: Answering Common Questions About Mexican Credit:

-

What is a credit score in Mexico, and how is it calculated? A credit score in Mexico reflects your creditworthiness based on payment history, outstanding balances, and credit utilization. The specific calculation methods vary slightly between Buró de Crédito and Círculo de Crédito.

-

How can I improve my credit score in Mexico? Pay your bills on time, maintain low credit utilization, and avoid applying for too much credit at once.

-

Where can I find reliable information about credit products in Mexico? Consult the websites of reputable banks, financial institutions, and the CNBV.

Practical Tips: Maximizing the Benefits of Mexican Credit:

- Build a positive credit history: Pay all your bills on time and in full.

- Monitor your credit report regularly: Check your credit report from Buró de Crédito and Círculo de Crédito for any errors or inaccuracies.

- Shop around for the best interest rates: Compare offers from different lenders before committing to a loan.

- Understand the loan terms carefully: Read the fine print before signing any credit agreement.

- Create a budget and manage your debt responsibly: Avoid accumulating excessive debt.

Final Conclusion: Wrapping Up with Lasting Insights:

The Mexican credit system, while complex, plays a crucial role in the country's economic development. By understanding its intricacies, navigating its challenges, and leveraging its opportunities, individuals and businesses can unlock significant economic potential. The ongoing evolution of the system, driven by technological advancements and government initiatives, promises a brighter future of financial inclusion and responsible credit access for all Mexicans.

Latest Posts

Latest Posts

-

What Is The Minimum Payment On Amazon Store Card

Apr 05, 2025

-

What Does Minimum Balance Mean On Credit Card

Apr 05, 2025

-

What Does Paying The Minimum Payment On A Credit Card Mean

Apr 05, 2025

-

What Does Minimum Credit Limit Mean On A Credit Card

Apr 05, 2025

-

What Does Making The Minimum Payment Mean On Your Credit Card

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Does Credit Work In Mexico . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.