How Do Institutions Calculate The Minimum Payment

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Decoding the Minimum Payment: How Institutions Calculate the Amount You Owe

What if understanding how minimum payments are calculated could save you thousands of dollars over your lifetime? This seemingly simple number holds significant financial implications, often leading to prolonged debt and increased interest costs.

Editor’s Note: This article on minimum payment calculations has been thoroughly researched and updated to reflect current industry practices. We aim to provide clarity and empower readers to make informed financial decisions.

Why Minimum Payment Calculations Matter: Relevance, Practical Applications, and Industry Significance

Understanding how institutions calculate minimum payments is crucial for responsible debt management. Failing to grasp this seemingly simple calculation can lead to significantly higher overall costs, extended repayment periods, and potential damage to one's credit score. The impact extends beyond individual consumers; businesses also need to understand these calculations for effective financial planning and risk assessment. From credit cards and personal loans to mortgages and student loans, the minimum payment calculation influences borrowing strategies and long-term financial health.

Overview: What This Article Covers

This article delves into the intricacies of minimum payment calculations across various debt types. We will explore different methodologies employed by financial institutions, the factors influencing these calculations, and the potential consequences of only paying the minimum. We will also discuss strategies for effective debt management and proactive financial planning.

The Research and Effort Behind the Insights

This article is based on extensive research, drawing upon publicly available information from financial institutions, regulatory bodies, and scholarly articles on consumer finance. We have analyzed various methodologies and case studies to provide a comprehensive and accurate portrayal of minimum payment calculations.

Key Takeaways:

- Definition and Core Concepts: Understanding the fundamental principles governing minimum payment calculations.

- Calculations Across Debt Types: Examining the specific methodologies used for credit cards, loans, and mortgages.

- Factors Influencing Minimum Payments: Exploring variables like interest rates, outstanding balance, and repayment terms.

- Consequences of Only Paying the Minimum: Highlighting the long-term financial implications of minimum payments.

- Strategies for Effective Debt Management: Providing practical advice for efficient debt repayment.

Smooth Transition to the Core Discussion

Now that we’ve established the importance of understanding minimum payment calculations, let's delve into the specifics, examining how different institutions arrive at that seemingly insignificant yet powerfully influential number.

Exploring the Key Aspects of Minimum Payment Calculations

1. Definition and Core Concepts:

A minimum payment is the smallest amount a borrower can pay on a debt within a given billing cycle without incurring late fees or penalties. It is typically a percentage of the outstanding balance, a fixed amount, or a combination of both. The primary purpose of the minimum payment is to maintain the account in good standing, preventing defaults and associated negative consequences. However, it's crucial to understand that solely paying the minimum often prolongs the repayment period and significantly increases the total interest paid.

2. Calculations Across Debt Types:

-

Credit Cards: Credit card minimum payment calculations vary slightly between issuers but generally involve a combination of factors. A common approach is to calculate a percentage of the outstanding balance (often 1-3%), with a minimum dollar amount (e.g., $25) as a floor. This ensures that even with small balances, a borrower pays at least a certain amount. The percentage method is designed to ensure sufficient payments are made, and this percentage is often directly stated within the account agreement.

-

Personal Loans: Minimum payments for personal loans are typically fixed monthly installments calculated based on the loan amount, interest rate, and loan term. These payments are amortized, meaning each payment covers a portion of the principal and the interest accrued. Amortization schedules clearly outline the payment schedule for the loan's duration. The calculation is based on standard loan amortization formulas, accessible online or through financial calculators.

-

Mortgages: Similar to personal loans, mortgage minimum payments are generally fixed monthly installments calculated using an amortization schedule. The calculations consider the loan amount, interest rate, loan term (typically 15 or 30 years), and property taxes and homeowners insurance (often included in the monthly payment as escrow). The complexity increases when dealing with adjustable-rate mortgages (ARMs) where interest rates can fluctuate, impacting the minimum payment over time. Mortgage calculations often utilize more complex formulas that account for these variations.

-

Student Loans: Student loan minimum payments vary depending on the type of loan (federal or private), repayment plan selected (standard, income-driven, etc.), and the loan amount. Federal student loans offer various repayment plans, each with its own minimum payment calculation. Income-driven plans, for example, adjust minimum payments based on the borrower's income and family size. Private student loans, on the other hand, usually have fixed minimum payments similar to personal loans.

3. Factors Influencing Minimum Payments:

Several factors influence the calculation of minimum payments:

- Interest Rate: Higher interest rates generally result in higher minimum payments because a larger portion of the payment goes towards interest.

- Outstanding Balance: A higher outstanding balance usually results in a higher minimum payment (especially when using percentage-based calculations).

- Repayment Term: Longer repayment terms generally lead to lower minimum payments, but significantly increase the total interest paid over the life of the loan.

- Fees and Charges: Late fees, annual fees, and other charges can affect the minimum payment calculation.

- Type of Debt: As discussed earlier, different debt types use different calculation methodologies.

4. Consequences of Only Paying the Minimum:

Consistently paying only the minimum payment on debts can have several significant negative consequences:

- Prolonged Debt: It takes significantly longer to pay off debt, increasing the total time spent in debt.

- Increased Interest Costs: The vast majority of interest accrues over the life of the debt, and extending the repayment period means substantially higher interest charges.

- Negative Impact on Credit Score: While making minimum payments prevents immediate delinquency, it can negatively influence credit utilization ratios, affecting one's credit score.

- Financial Stress: Prolonged debt can create ongoing financial stress, limiting the ability to save, invest, and achieve other financial goals.

Exploring the Connection Between Interest Rates and Minimum Payments

The relationship between interest rates and minimum payments is directly proportional. Higher interest rates lead to higher minimum payments (assuming a percentage-based calculation), as a larger portion of the payment covers the accrued interest. This relationship is critical because it demonstrates how seemingly small interest rate changes can significantly impact the minimum payment and the overall cost of borrowing.

Key Factors to Consider:

-

Roles and Real-World Examples: Consider a credit card with a $1000 balance and a 20% interest rate. The minimum payment might be $25, significantly more than if the interest rate was 10%. This illustrates the impact of even modest interest rate fluctuations.

-

Risks and Mitigations: The primary risk is incurring significant additional interest expenses and extending the repayment period. Mitigation involves aggressively paying more than the minimum to reduce the principal balance and decrease interest payments.

-

Impact and Implications: The long-term impact includes significantly higher overall costs and potential financial strain. Understanding this interplay empowers informed decisions on debt management strategies.

Conclusion: Reinforcing the Connection

The interplay between interest rates and minimum payments emphasizes the importance of understanding the mechanics of debt repayment. By paying down the principal aggressively, borrowers can mitigate the long-term costs of high-interest rates and shorten their repayment time.

Further Analysis: Examining Interest Rate Calculation in Greater Detail

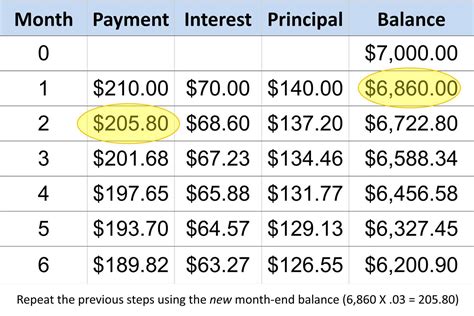

The calculation of interest on credit cards and loans is usually done using a daily periodic rate, a compound interest formula. This rate is determined by dividing the annual percentage rate (APR) by 365 (or 360 in some cases). The daily interest is then calculated on the outstanding balance, and this process repeats daily until the balance is paid. This compounding effect is what can make paying only the minimum so expensive.

FAQ Section: Answering Common Questions About Minimum Payments

-

What is a minimum payment? A minimum payment is the lowest amount you can pay on a debt each billing cycle without incurring late fees.

-

How are minimum payments calculated? The calculation varies depending on the debt type. Credit cards often use a percentage of the balance with a minimum dollar amount. Loans and mortgages generally have fixed monthly payments based on amortization schedules.

-

What happens if I only pay the minimum? You'll pay more in interest over time and take much longer to pay off the debt. This can negatively affect your credit score and financial health.

-

How can I pay off debt faster? Pay more than the minimum payment each month to reduce the principal balance and interest charges. Consider debt consolidation or balance transfer options.

Practical Tips: Maximizing the Benefits of Understanding Minimum Payments

- Understand your APR: Knowing your APR allows you to estimate the interest accrual accurately.

- Create a budget: A budget helps track expenses and allocate funds towards debt repayment.

- Prioritize high-interest debt: Focus on paying down debts with the highest interest rates first.

- Explore debt consolidation: Consolidating multiple debts into a single loan can simplify payments and potentially reduce interest rates.

Final Conclusion: Wrapping Up with Lasting Insights

Understanding how institutions calculate minimum payments is a crucial component of responsible financial management. While the minimum payment may seem insignificant, its implications on long-term financial health are profound. By understanding the mechanics behind these calculations and employing proactive debt management strategies, individuals can avoid the pitfalls of prolonged debt, excessive interest charges, and potential damage to their credit scores. Taking control of your debt repayment journey starts with understanding the numbers.

Latest Posts

Latest Posts

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Edpuzzle

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Quizlet

Apr 05, 2025

-

Minimum Payment Home Depot Card

Apr 05, 2025

-

Does Home Depot Do Monthly Payments

Apr 05, 2025

-

What Is A Minimum Monthly Payment

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Do Institutions Calculate The Minimum Payment . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.