How Do I Know What The Minimum Payment On My Credit Card Is

adminse

Apr 04, 2025 · 7 min read

Table of Contents

How Can I Easily Determine My Credit Card's Minimum Payment?

Understanding your minimum payment is crucial for responsible credit card management.

Editor’s Note: This article on determining your credit card minimum payment was published today, providing you with the most up-to-date information and strategies for managing your credit card debt effectively.

Why Understanding Your Minimum Payment Matters:

Knowing your credit card's minimum payment is not just about avoiding late fees; it's fundamental to responsible credit management. Understanding this amount allows you to:

- Avoid Late Fees: Failing to make at least the minimum payment by the due date incurs significant late fees, rapidly increasing your debt.

- Maintain a Good Credit Score: Consistently making at least the minimum payment demonstrates responsible credit behavior, positively impacting your credit score. A good credit score is essential for securing loans, mortgages, and even renting an apartment.

- Track Your Debt: Understanding the minimum payment helps you monitor your debt and create a realistic repayment plan. This awareness prevents the debt from spiraling out of control.

- Budget Effectively: Knowing your minimum payment allows you to incorporate it into your monthly budget, ensuring you have enough funds available to avoid missed payments.

- Avoid Default: Consistent failure to meet even minimum payments can lead to account default, severely damaging your credit and potentially leading to collection actions.

Overview: What This Article Covers

This comprehensive guide explores multiple ways to determine your credit card minimum payment. We'll cover checking your statement, using online account access, contacting your issuer, understanding the implications of only paying the minimum, and strategies for managing your debt effectively.

The Research and Effort Behind the Insights

This article draws upon research from reputable financial institutions, consumer protection agencies, and extensive analysis of credit card agreements. The information provided is designed to be accurate, reliable, and actionable.

Key Takeaways:

- Multiple Methods for Finding Minimum Payment: Learn various ways to access this crucial information.

- Understanding the Implications of Minimum Payments: Grasp the long-term financial consequences.

- Strategies for Effective Debt Management: Develop a plan to pay down your debt more efficiently.

- Resources for Further Assistance: Discover where to seek help if you're struggling with credit card debt.

Smooth Transition to the Core Discussion

Now that we've established the importance of knowing your minimum payment, let's delve into the practical methods for determining this amount.

Exploring the Key Aspects of Determining Your Minimum Payment

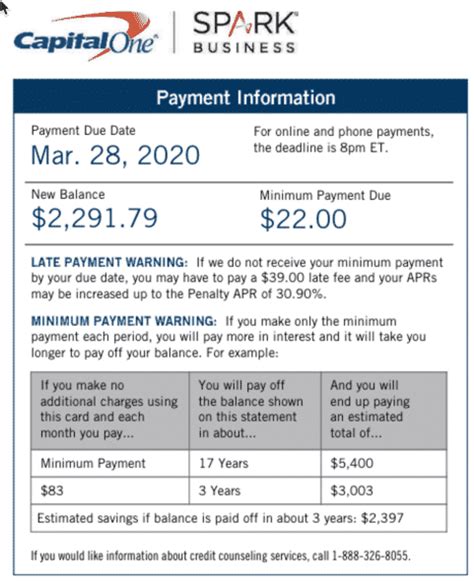

1. Checking Your Credit Card Statement:

The most straightforward method is to review your monthly credit card statement. The statement clearly outlines the minimum payment due, usually prominently displayed near the payment due date and total balance. Look for phrases like "Minimum Payment Due," "Minimum Amount Due," or a similar designation. The statement usually specifies the exact amount you must pay to avoid late fees.

2. Using Online Account Access:

Most credit card companies offer online account management portals. Logging into your account typically provides a comprehensive overview of your account, including your current balance, available credit, recent transactions, and crucially, the minimum payment due. This information is often readily accessible on the dashboard or summary page of your online account.

3. Utilizing Mobile Banking Apps:

Many credit card companies have mobile apps that mirror the functionality of their online portals. These apps provide convenient access to your account information, including the minimum payment due, allowing you to check it anytime, anywhere.

4. Contacting Your Credit Card Issuer:

If you're unable to locate the minimum payment on your statement or online, contact your credit card issuer directly. Customer service representatives can quickly provide this information. You can typically find their contact information on the back of your credit card or on your statement.

5. Checking Your Credit Card Agreement:

While not a regular method for finding your minimum payment for a given month, your credit card agreement will typically detail the calculation method for the minimum payment. While it won't give you the exact amount each month, it will shed light on how the minimum is calculated.

Exploring the Connection Between Interest Rates and Minimum Payments

The connection between your interest rate and minimum payment is indirect but significant. A higher interest rate generally means a larger portion of your minimum payment goes towards interest, leaving a smaller portion to reduce your principal balance. This slows down the debt repayment process, potentially leading to paying significantly more in interest over the life of the debt.

Key Factors to Consider:

- Roles and Real-World Examples: A high interest rate (e.g., 24%) will mean a greater proportion of your minimum payment is interest, leaving only a small amount to pay down the debt. Conversely, a low interest rate (e.g., 12%) will mean a larger proportion is applied to the principal.

- Risks and Mitigations: Relying solely on minimum payments with a high interest rate significantly increases the total interest paid and extends the repayment period. Mitigations include paying more than the minimum and exploring balance transfer options to lower interest rates.

- Impact and Implications: Paying only the minimum can lead to substantial long-term costs, potentially trapping you in a cycle of debt. Understanding this dynamic encourages more proactive debt management.

Conclusion: Reinforcing the Connection

The interest rate directly influences how effectively your minimum payment reduces your principal debt. A higher rate means slower repayment and higher overall costs, emphasizing the importance of paying more than the minimum whenever possible.

Further Analysis: Examining Interest Rate Calculations in Greater Detail

Credit card interest is typically calculated using the average daily balance method. This means the interest charged each month is based on the average balance carried throughout the billing cycle. Understanding this calculation helps you appreciate the impact of carrying a high balance.

FAQ Section: Answering Common Questions About Minimum Payments

Q: What happens if I only pay the minimum payment on my credit card each month?

A: While you'll avoid late fees, paying only the minimum significantly prolongs the repayment period and results in paying substantially more in interest over the life of the debt.

Q: Can the minimum payment amount change from month to month?

A: Yes, the minimum payment can fluctuate based on your balance, payment history, and the credit card's terms.

Q: What if I miss my minimum payment?

A: You'll incur late fees, negatively impacting your credit score. Repeated missed payments can lead to account default.

Q: Are there any penalties for consistently paying only the minimum?

A: While there aren't direct penalties, consistently paying only the minimum is financially detrimental due to accrued interest and prolonged debt repayment.

Practical Tips: Maximizing the Benefits of Understanding Your Minimum Payment

- Track Your Spending: Monitor your spending habits to control your balance and minimize the minimum payment.

- Pay More Than the Minimum: Whenever possible, pay more than the minimum to accelerate debt repayment and reduce overall interest costs.

- Create a Budget: Incorporate your minimum payment into your monthly budget to avoid missed payments.

- Explore Debt Management Options: If struggling with debt, consider options like balance transfers, debt consolidation, or credit counseling.

- Set Realistic Goals: Develop a realistic repayment plan, setting achievable goals to pay down your debt gradually.

Final Conclusion: Wrapping Up with Lasting Insights

Knowing your minimum credit card payment is crucial for responsible financial management. While it's a starting point, aiming to pay more than the minimum is key to efficiently managing credit card debt and building a strong financial future. Proactive planning and understanding the nuances of minimum payments empower you to take control of your finances and avoid the pitfalls of accumulating unnecessary debt. Remember, your credit card statement, online account access, and mobile app are your primary tools for quickly and efficiently determining your minimum payment each month.

Latest Posts

Latest Posts

-

What Is The Minimum Pay At Home Depot

Apr 05, 2025

-

What Is The Minimum Payment On Home Depot Credit Card

Apr 05, 2025

-

What Is The Minimum Wage For Home Depot

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Do I Know What The Minimum Payment On My Credit Card Is . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.