How Do I Know What My Minimum Credit Card Payment Will Be

adminse

Apr 04, 2025 · 8 min read

Table of Contents

Decoding Your Minimum Credit Card Payment: A Comprehensive Guide

What if understanding your minimum credit card payment is the key to avoiding crippling debt? Mastering this seemingly simple calculation can be the cornerstone of responsible credit card management and long-term financial health.

Editor’s Note: This article on understanding minimum credit card payments was published today and provides up-to-date information on navigating this crucial aspect of credit card management. We'll break down the factors influencing your minimum payment, how to calculate it, and what to consider before only paying the minimum.

Why Understanding Your Minimum Credit Card Payment Matters:

Understanding your minimum credit card payment isn't just about avoiding late fees; it's a fundamental step towards responsible credit management. Ignoring this seemingly small number can lead to a snowball effect of accumulating interest, significantly increasing your overall debt and harming your credit score. Paying only the minimum often traps individuals in a cycle of debt that can take years to escape. This knowledge empowers you to make informed financial decisions, plan your budget effectively, and build a strong financial future.

Overview: What This Article Covers:

This comprehensive guide will delve into the intricacies of minimum credit card payments. We'll explore how the minimum payment is calculated, the factors that influence it, the potential consequences of only paying the minimum, and strategies for responsible credit card usage. We'll also examine the impact of various payment methods and address frequently asked questions.

The Research and Effort Behind the Insights:

This article draws upon extensive research, including analysis of credit card agreements from various financial institutions, regulatory guidelines, and insights from financial experts. We've synthesized this information to provide readers with clear, actionable advice based on reliable data and credible sources.

Key Takeaways:

- Definition and Core Concepts: A clear definition of minimum credit card payment and the underlying principles governing its calculation.

- Factors Influencing Minimum Payment: A detailed breakdown of the variables determining your minimum payment amount.

- Calculating Your Minimum Payment: Practical methods for estimating and verifying your minimum payment.

- Consequences of Only Paying the Minimum: A thorough examination of the long-term financial implications of this strategy.

- Strategies for Responsible Credit Card Use: Actionable tips for effective credit card management.

- The Role of Interest and APR: Understanding the impact of interest accrual on your debt.

Smooth Transition to the Core Discussion:

Now that we've established the importance of understanding your minimum credit card payment, let's explore the key aspects in detail. We will begin by dissecting the factors that contribute to this crucial figure.

Exploring the Key Aspects of Minimum Credit Card Payments:

1. Definition and Core Concepts:

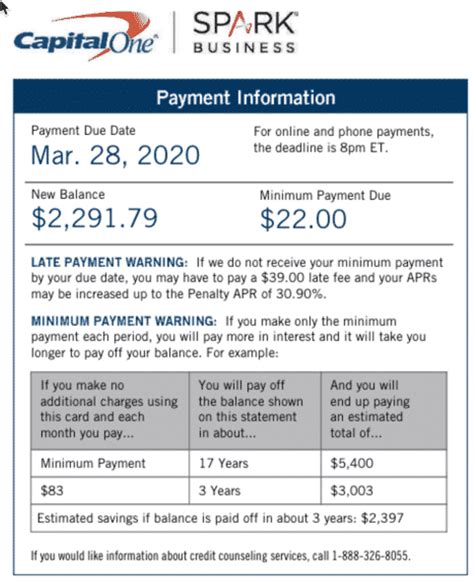

The minimum credit card payment is the smallest amount you can pay on your credit card statement each month without incurring a late fee. It's usually a percentage of your outstanding balance (often 1-3%), but it can also include a minimum dollar amount, ensuring that you pay at least a specified sum, regardless of your balance. This minimum payment is clearly stated on your monthly credit card statement. It's crucial to understand that this payment only covers a portion of your outstanding debt; the remaining balance continues to accrue interest.

2. Factors Influencing Minimum Payment:

Several factors influence the calculation of your minimum payment. These include:

- Outstanding Balance: The larger your outstanding balance, the higher your minimum payment will typically be (as a percentage).

- Credit Card Agreement: Each credit card issuer has its own terms and conditions outlining how minimum payments are calculated. These can vary significantly.

- Interest Accrued: While not directly factored into the minimum payment calculation, the interest accrued on your outstanding balance adds to your overall debt and impacts your future minimum payments.

- Fees and Charges: Late fees, annual fees, and other charges added to your account will typically increase your minimum payment.

- Promotional Periods: Some credit cards may offer introductory periods with lower interest rates or waived fees. These periods can temporarily influence your minimum payment.

3. Calculating Your Minimum Payment:

There's no single formula for calculating a minimum payment because it varies by issuer. However, you can usually find this information:

- On Your Credit Card Statement: The most reliable source is your monthly statement, which clearly shows the minimum amount due.

- Your Credit Card Agreement: Your credit card agreement (often available online) will outline the calculation method used by your issuer. This might specify a percentage of the balance or a fixed minimum dollar amount, whichever is greater.

- Contacting Your Issuer: If you have difficulty locating the information, contacting your credit card company's customer service is the most direct way to get the precise minimum payment amount.

4. Consequences of Only Paying the Minimum:

Paying only the minimum payment each month has significant long-term financial consequences:

- Accumulation of Interest: The vast majority of your payment goes toward interest, leaving only a small portion applied to your principal balance. This means it will take much longer to pay off your debt.

- Increased Total Debt: The accumulating interest significantly increases your total debt over time.

- Negative Impact on Credit Score: While consistently paying at least the minimum payment prevents late payment marks, carrying a high balance relative to your credit limit negatively impacts your credit utilization ratio, a key component of your credit score.

- Prolonged Debt Cycle: Paying only the minimum can trap you in a cycle of debt for years, preventing you from achieving other financial goals.

5. Strategies for Responsible Credit Card Use:

Avoid the pitfalls of minimum payments by adopting these strategies:

- Pay More Than the Minimum: Aim to pay as much as possible above the minimum payment each month to reduce your principal balance quicker and minimize interest charges.

- Budget Effectively: Create a budget that allows you to allocate sufficient funds for credit card payments.

- Track Your Spending: Monitor your spending regularly to avoid exceeding your credit limit and accumulating high balances.

- Consider Debt Consolidation: If you're struggling with multiple high-interest debts, debt consolidation can help streamline your payments and potentially lower your interest rate.

- Explore Balance Transfer Options: Some credit cards offer balance transfer options with introductory 0% APR periods. This can be a temporary solution to help you pay down your balance more efficiently.

Exploring the Connection Between Interest Rates and Minimum Payments:

The relationship between interest rates (APR) and minimum payments is crucial. A higher APR means a greater portion of your minimum payment goes towards interest, leaving less for the principal. This exacerbates the problem of paying only the minimum and significantly extends the repayment period.

Key Factors to Consider:

- Roles and Real-World Examples: Consider a scenario where an individual with a $5,000 balance and a 20% APR pays only the minimum. Even with consistent minimum payments, the interest accrual will substantially increase the total repayment amount and the overall time required to pay off the debt.

- Risks and Mitigations: The primary risk is prolonged debt and financial stress. Mitigation involves budgeting, prioritizing debt repayment, and exploring debt management options.

- Impact and Implications: The long-term impact is diminished financial flexibility, reduced credit score, and potential financial hardship.

Conclusion: Reinforcing the Connection:

The interplay between interest rates and minimum payments highlights the critical need to pay more than the minimum whenever possible. By understanding this connection, consumers can make informed decisions that lead to quicker debt repayment and improved financial well-being.

Further Analysis: Examining Interest Rates in Greater Detail:

Annual Percentage Rate (APR) is the annual interest rate charged on your outstanding credit card balance. It's a crucial factor in calculating interest charges and influences the effectiveness of your minimum payments. Understanding your APR is essential for making informed financial decisions. High APRs drastically increase the cost of borrowing and prolong the time it takes to repay your balance. Comparing APRs across different credit cards is vital when choosing a card.

FAQ Section: Answering Common Questions About Minimum Credit Card Payments:

-

Q: What happens if I miss a minimum payment? A: You'll likely incur a late payment fee, and this late payment will negatively impact your credit score. Repeated missed payments can lead to account suspension or closure.

-

Q: Can my minimum payment change each month? A: Yes, your minimum payment can fluctuate depending on your outstanding balance, fees, and interest charges.

-

Q: Is it always best to pay more than the minimum? A: Yes, paying more than the minimum accelerates debt repayment, reduces overall interest paid, and improves your credit score.

-

Q: How can I find my APR? A: Your APR is usually stated prominently on your credit card statement and in your credit card agreement.

-

Q: What if I can't afford to pay even the minimum? A: Contact your credit card issuer immediately to discuss potential options, such as hardship programs or payment plans.

Practical Tips: Maximizing the Benefits of Understanding Your Minimum Payment:

- Understand the Basics: Learn how your minimum payment is calculated and the factors influencing it.

- Check Your Statement Regularly: Review your statement meticulously to understand your balance, minimum payment, and interest charges.

- Budget for Credit Card Payments: Include credit card payments in your monthly budget, prioritizing payments above the minimum.

- Set Up Automatic Payments: Automate your payments to avoid late fees and ensure timely repayment.

- Seek Professional Advice: If you're struggling with credit card debt, consult a financial advisor for personalized guidance.

Final Conclusion: Wrapping Up with Lasting Insights:

Understanding your minimum credit card payment is more than just a technicality; it's a fundamental aspect of responsible financial management. By grasping the factors involved, understanding the long-term consequences of only paying the minimum, and implementing proactive strategies, you can pave the way for improved financial health and a brighter financial future. Remember that consistently paying more than the minimum is crucial for escaping the debt trap and building a solid credit history.

Latest Posts

Latest Posts

-

How Much Minimum Payment For Credit Card

Apr 05, 2025

-

How Is The Minimum Monthly Payment On A Credit Card Calculated

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Responses

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Edpuzzle

Apr 05, 2025

-

Why Is It More Difficult To Get Out Of Debt When Only Paying The Minimum Payment Quizlet

Apr 05, 2025

Related Post

Thank you for visiting our website which covers about How Do I Know What My Minimum Credit Card Payment Will Be . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.