Early Withdrawal Penalty Definition Finance

adminse

Mar 31, 2025 · 8 min read

Table of Contents

Unlocking the Mysteries of Early Withdrawal Penalties: A Comprehensive Guide

What if the financial security you diligently built could be jeopardized by unexpected early withdrawals? Understanding early withdrawal penalties is crucial for navigating the complexities of finance and safeguarding your hard-earned savings.

Editor’s Note: This article on early withdrawal penalties provides a comprehensive overview of this important financial concept. Updated with the latest information, it serves as a valuable resource for anyone saving for retirement, investing in various financial products, or simply seeking a better understanding of their financial obligations.

Why Early Withdrawal Penalties Matter: Relevance, Practical Applications, and Industry Significance

Early withdrawal penalties are significant because they directly impact the return on your investments and can have substantial financial consequences. Understanding these penalties is critical for making informed decisions about saving, investing, and accessing your funds. The penalties vary significantly depending on the type of account, the financial institution, and the terms of the investment agreement. Ignoring these penalties can lead to substantial losses, undermining your long-term financial goals. These penalties are relevant across various financial products, including retirement accounts, certificates of deposit (CDs), and certain types of insurance policies.

Overview: What This Article Covers

This article offers a deep dive into early withdrawal penalties, covering their definition, the various circumstances that trigger them, the calculation methods, and strategies to mitigate or avoid them altogether. We will examine different types of accounts and investments affected by these penalties, providing practical examples and actionable insights to empower informed financial decisions.

The Research and Effort Behind the Insights

This comprehensive guide is the result of extensive research, integrating information from reputable financial institutions, regulatory bodies, and legal documents. We have meticulously analyzed various financial products and their associated terms and conditions to ensure accuracy and present a well-rounded understanding of early withdrawal penalties.

Key Takeaways:

- Definition and Core Concepts: A precise definition of early withdrawal penalties and their underlying principles.

- Types of Accounts Affected: A detailed overview of accounts and investments subject to early withdrawal penalties.

- Penalty Calculation Methods: Understanding the various methods used to calculate these penalties.

- Strategies for Mitigation: Practical steps to minimize or avoid incurring early withdrawal penalties.

- Legal and Regulatory Aspects: An overview of the legal and regulatory frameworks surrounding these penalties.

Smooth Transition to the Core Discussion:

With an understanding of the importance of early withdrawal penalties, let’s delve into the specific details, starting with a clear definition and exploring their impact across different financial instruments.

Exploring the Key Aspects of Early Withdrawal Penalties

Definition and Core Concepts:

An early withdrawal penalty is a financial charge levied by a financial institution when you withdraw funds from a specific account or investment before the agreed-upon term or maturity date. These penalties are designed to discourage premature withdrawals and encourage long-term commitment to savings and investment strategies. The rationale behind these penalties is that financial institutions often structure these products with the expectation of long-term investment. Early withdrawals disrupt these plans, potentially impacting their profitability and ability to meet their obligations to other clients.

Types of Accounts Affected:

Several types of financial accounts and investments are susceptible to early withdrawal penalties. These include:

-

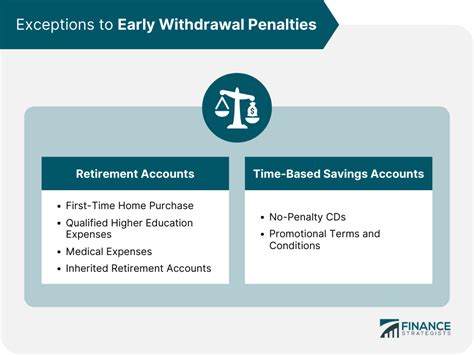

Retirement Accounts: These accounts, such as 401(k)s, 403(b)s, and IRAs (Traditional and Roth), often have penalties for withdrawals before the age of 59 1/2, unless specific exceptions apply. These penalties usually amount to a 10% tax on the withdrawn amount, in addition to any applicable income taxes. However, certain circumstances, such as severe financial hardship or first-time home buyer expenses, may allow for exceptions.

-

Certificates of Deposit (CDs): CDs are time deposits that offer a fixed interest rate over a specific term. Withdrawing funds before maturity typically results in an early withdrawal penalty, usually involving the forfeiture of a portion of the accrued interest or even a percentage of the principal. The penalty amount varies based on the length of the CD term and the specific bank or financial institution.

-

Annuities: Annuities are insurance products designed to provide regular income payments over time. Early withdrawals usually involve penalties that depend on the type of annuity and the timing of the withdrawal. These penalties can vary greatly, and understanding the specific terms of your annuity contract is crucial.

-

Savings Bonds: While generally considered low-risk investments, early withdrawal penalties may apply if you cash in savings bonds before they reach a certain maturity period. The penalty may vary depending on the type of savings bond and the length of time you hold it.

Penalty Calculation Methods:

The method for calculating early withdrawal penalties varies widely depending on the specific financial product and institution. Common methods include:

-

Fixed Percentage: A fixed percentage of the withdrawn amount is deducted as a penalty. For example, a 1% penalty on a $10,000 withdrawal would result in a $100 penalty.

-

Interest Forfeiture: The accrued interest earned up to the point of withdrawal is forfeited entirely. This can be especially significant for longer-term investments.

-

Tiered Penalties: Different penalty rates are applied based on the duration of the investment and the timing of the withdrawal. The longer the investment is held before withdrawal, the lower the penalty may be.

-

Combination of Methods: Some institutions may employ a combination of methods, such as a percentage of the principal plus interest forfeiture.

Strategies for Mitigation:

Avoiding early withdrawal penalties requires careful planning and understanding of your financial goals. Some strategies include:

-

Careful Account Selection: Choose accounts and investments that align with your timeline and financial needs. Avoid products with steep penalties if you anticipate needing access to funds prematurely.

-

Emergency Fund: Maintain a readily accessible emergency fund to cover unexpected expenses, reducing the need for early withdrawals from penalty-laden accounts.

-

Diversification: Spread your investments across different types of accounts to minimize risk. Having a mix of liquid and less liquid assets allows flexibility while still having long-term growth potential.

-

Financial Planning: Seek professional financial advice to develop a personalized financial plan that takes into account your short-term and long-term financial goals and risk tolerance.

Legal and Regulatory Aspects:

Early withdrawal penalties are generally governed by the terms and conditions of the specific financial product and the laws and regulations of the relevant jurisdiction. It's essential to thoroughly review the contract before investing to understand the implications of early withdrawals.

Exploring the Connection Between Tax Implications and Early Withdrawal Penalties

The relationship between tax implications and early withdrawal penalties is significant. While the penalties themselves are financial charges levied by the institution, they often have tax consequences as well. This is particularly true for retirement accounts where the early withdrawal penalty is often coupled with additional income taxes on the withdrawn amount. For example, withdrawing from a traditional IRA before age 59 1/2 typically results in both a 10% early withdrawal penalty and income tax on the withdrawn amount.

Key Factors to Consider:

-

Roles and Real-World Examples: The tax implications vary significantly depending on the type of account. Withdrawing from a Roth IRA typically avoids the early withdrawal penalty, but the earnings may be taxed if withdrawn before age 59 1/2.

-

Risks and Mitigations: Proper financial planning, including understanding tax implications, can help mitigate risks associated with early withdrawals. Tax professionals can advise on strategies to minimize tax burdens.

-

Impact and Implications: Failure to account for tax implications can significantly reduce the net amount received after an early withdrawal. This can severely impact your financial goals.

Conclusion: Reinforcing the Connection

The connection between tax implications and early withdrawal penalties highlights the importance of understanding the total cost of premature withdrawals. Ignoring these tax consequences can lead to unexpected financial losses.

Further Analysis: Examining Tax Laws and Regulations in Greater Detail

Federal tax laws and regulations heavily influence the tax consequences of early withdrawals from retirement accounts. The Internal Revenue Code (IRC) outlines the rules and exceptions regarding penalties and taxation. Understanding these regulations is essential for accurate planning.

FAQ Section: Answering Common Questions About Early Withdrawal Penalties

What is an early withdrawal penalty?

An early withdrawal penalty is a financial charge applied when you withdraw funds from a financial product before the agreed-upon term.

How are early withdrawal penalties calculated?

Methods vary. Common methods include a fixed percentage of the withdrawn amount, interest forfeiture, tiered penalties, or a combination.

What types of accounts are subject to early withdrawal penalties?

Retirement accounts (401(k)s, IRAs), CDs, annuities, and savings bonds are common examples.

Can early withdrawal penalties be avoided?

Careful planning, emergency funds, diversification, and professional financial advice can significantly reduce the likelihood of incurring penalties.

What are the tax implications of early withdrawals?

Tax implications often accompany early withdrawal penalties, especially with retirement accounts, leading to additional income tax on the withdrawn amount.

Practical Tips: Maximizing the Benefits of Avoiding Early Withdrawal Penalties

-

Understand the terms: Thoroughly review the terms and conditions of any financial product before investing.

-

Set realistic goals: Align your investment choices with your long-term financial objectives.

-

Emergency fund: Establish a readily available emergency fund to cover unexpected expenses.

-

Diversify: Spread your investments across different accounts to minimize risk and provide flexibility.

-

Seek professional advice: Consult a financial advisor to create a personalized financial plan.

Final Conclusion: Wrapping Up with Lasting Insights

Early withdrawal penalties represent a significant financial risk that can derail long-term goals. By understanding the intricacies of these penalties, diversifying investments, and planning prudently, individuals can protect their hard-earned savings and achieve financial security. Proactive financial planning, including seeking professional advice, is crucial in navigating this complex landscape and mitigating the impact of potential penalties. Remember, informed decision-making is the cornerstone of sound financial management.

Latest Posts

Latest Posts

-

Sacrifice Ratio In Economics Definition Example

Apr 29, 2025

-

What Have Pension Funds Invested In Ftx

Apr 29, 2025

-

How Are Mutual Funds Money Market Funds And Pension Funds Similar How Are They Different

Apr 29, 2025

-

How Much Have Pension Funds Affected The Price Of Tuition

Apr 29, 2025

-

How Much Have Teacher Pension Funds Affected The Price Of Tuition

Apr 29, 2025

Related Post

Thank you for visiting our website which covers about Early Withdrawal Penalty Definition Finance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.