Definition And Types Of Cost Accounting

adminse

Mar 28, 2025 · 7 min read

Table of Contents

Unveiling the World of Cost Accounting: Definitions, Types, and Applications

What if the future of profitable business operations hinges on a deep understanding of cost accounting? This critical discipline is the backbone of informed decision-making, empowering businesses to optimize resource allocation and maximize profitability.

Editor’s Note: This comprehensive article on cost accounting provides a detailed exploration of its definitions, various types, and practical applications. Updated with the latest insights, this resource serves as a valuable guide for business professionals, students, and anyone seeking to understand the financial underpinnings of successful businesses.

Why Cost Accounting Matters:

Cost accounting is far more than just number crunching; it's a strategic tool enabling businesses to understand the true cost of producing goods or services. This knowledge informs crucial decisions regarding pricing, production efficiency, resource allocation, and overall profitability. From small startups to multinational corporations, effective cost accounting is essential for long-term financial health and competitive advantage. It allows for the identification of areas for improvement, facilitating cost reduction strategies and improved operational efficiency. Furthermore, accurate cost data is vital for financial reporting, compliance, and strategic planning.

Overview: What This Article Covers:

This article provides a thorough overview of cost accounting, beginning with its fundamental definition and exploring its diverse types. We will delve into the various methods used for cost accumulation and allocation, examining their strengths and weaknesses. The practical applications of cost accounting in different industries will be showcased, followed by a detailed explanation of relevant key performance indicators (KPIs). Finally, we address common questions and offer practical tips for effective cost accounting implementation.

The Research and Effort Behind the Insights:

This article synthesizes information from leading accounting textbooks, peer-reviewed research papers, and industry best practices. Extensive research ensures the accuracy and reliability of the information presented, providing readers with a comprehensive and up-to-date understanding of cost accounting.

Key Takeaways:

- Definition and Core Concepts: A clear understanding of cost accounting principles and terminology.

- Types of Cost Accounting: A detailed examination of various cost accounting methods, including their applications and limitations.

- Costing Methods: In-depth analysis of different costing methods such as job order costing, process costing, and activity-based costing.

- Practical Applications: Real-world examples demonstrating the use of cost accounting in diverse industries.

- Key Performance Indicators (KPIs): Understanding the essential metrics used to track and evaluate cost performance.

Smooth Transition to the Core Discussion:

Having established the importance of cost accounting, let's now delve into the specifics, starting with a clear definition and exploration of its fundamental concepts.

Exploring the Key Aspects of Cost Accounting:

Definition and Core Concepts:

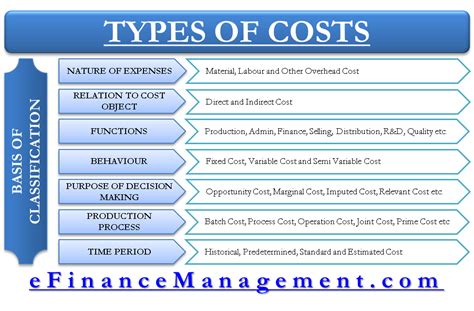

Cost accounting is a specialized branch of accounting that focuses on the systematic recording, classification, and analysis of business expenses. Its primary objective is to determine the cost of producing goods or services, providing essential information for pricing decisions, performance evaluation, and operational improvement. This differs from financial accounting, which focuses on external reporting to stakeholders. Cost accounting, however, is crucial for the data that informs financial accounting. Key concepts include:

- Direct Costs: Costs directly traceable to a specific product or service (e.g., raw materials, direct labor).

- Indirect Costs: Costs not easily traceable to a specific product (e.g., factory rent, utilities).

- Fixed Costs: Costs that remain constant regardless of production volume (e.g., rent, salaries).

- Variable Costs: Costs that change proportionally with production volume (e.g., raw materials, direct labor).

- Cost Allocation: The process of assigning indirect costs to specific products or services.

Types of Cost Accounting:

Several cost accounting methods cater to different business needs and structures. The most common types include:

-

Job Order Costing: This method tracks costs for individual projects or jobs. It's ideal for businesses producing unique or customized products, such as construction companies or custom furniture makers. Costs are accumulated for each job, making it easy to determine profitability on a per-job basis.

-

Process Costing: This method averages costs over a large volume of homogenous products. It's suitable for mass production environments where identical units are produced. The total cost of production is divided by the number of units to determine the cost per unit. Examples include food processing and chemical manufacturing.

-

Activity-Based Costing (ABC): ABC is a more sophisticated method that assigns costs based on activities that consume resources. It recognizes that indirect costs aren't always uniformly distributed across products. ABC is particularly useful in complex manufacturing environments with multiple products and processes. It helps identify cost drivers and pinpoint areas for improvement in efficiency.

Applications Across Industries:

Cost accounting finds wide application across various industries:

- Manufacturing: Determining the cost of goods sold, pricing strategies, and production efficiency improvements.

- Service Industries: Tracking the cost of providing services, optimizing resource allocation, and setting service prices.

- Retail: Analyzing inventory costs, pricing decisions, and managing supply chains.

- Healthcare: Determining the cost of patient care, managing resources, and evaluating the efficiency of healthcare services.

Challenges and Solutions:

Implementing effective cost accounting systems can present challenges:

- Data Accuracy: Maintaining accurate and timely cost data is crucial. Robust data collection and verification processes are essential.

- Cost Allocation: Accurately assigning indirect costs can be complex, requiring careful consideration of cost drivers and allocation methods.

- System Complexity: Implementing and maintaining complex cost accounting systems can be costly and time-consuming. Proper software and training are vital.

Impact on Innovation:

By providing detailed cost information, cost accounting drives innovation in various ways:

- Process Improvement: Identifying areas of inefficiency and cost reduction through analysis of cost data.

- New Product Development: Assessing the cost-effectiveness of new product ideas before launch.

- Pricing Strategies: Determining optimal pricing points based on accurate cost information.

Closing Insights: Summarizing the Core Discussion:

Cost accounting is not merely a compliance exercise; it's a strategic management tool that empowers businesses to make informed decisions, optimize resources, and enhance profitability. By understanding the various cost accounting methods and their applications, organizations can gain a competitive edge in today's dynamic business environment.

Exploring the Connection Between Technology and Cost Accounting:

Technology plays a significant role in modern cost accounting, transforming how businesses collect, analyze, and utilize cost data. The integration of Enterprise Resource Planning (ERP) systems, data analytics tools, and automation software significantly streamlines the cost accounting process. This section will delve into this vital connection.

Key Factors to Consider:

-

Roles and Real-World Examples: ERP systems automate data collection and provide real-time cost information. Data analytics tools enable advanced cost analysis and forecasting. Automation reduces manual data entry and minimizes errors.

-

Risks and Mitigations: The initial investment in technology can be substantial. Data security and integrity are paramount. Proper training and employee adoption are essential for successful implementation.

-

Impact and Implications: Technology enhances the accuracy, efficiency, and timeliness of cost accounting. It improves decision-making, fosters innovation, and contributes to improved profitability.

Conclusion: Reinforcing the Connection:

The synergy between technology and cost accounting is undeniable. Leveraging technological advancements enables businesses to optimize their cost accounting processes, gaining valuable insights that drive efficiency, innovation, and ultimately, success.

Further Analysis: Examining Technology in Greater Detail:

The adoption of cloud-based accounting software is transforming the landscape of cost accounting. These solutions offer scalability, accessibility, and enhanced collaboration capabilities. Advanced analytics tools offer predictive modeling and scenario planning, empowering businesses to proactively manage costs and optimize operations.

FAQ Section: Answering Common Questions About Cost Accounting:

-

What is the difference between cost accounting and financial accounting? Cost accounting focuses on internal decision-making, while financial accounting provides external reports to stakeholders.

-

How do I choose the right cost accounting method for my business? The optimal method depends on the nature of your business, product complexity, and production volume.

-

What are the key performance indicators (KPIs) used in cost accounting? KPIs include cost of goods sold (COGS), gross profit margin, contribution margin, and various efficiency ratios.

-

How can I improve the accuracy of my cost accounting data? Implement robust data collection procedures, regular data validation, and employee training.

Practical Tips: Maximizing the Benefits of Cost Accounting:

-

Understand Your Costs: Categorize your costs into direct and indirect, fixed and variable components.

-

Choose the Right Costing Method: Select a method that aligns with your business model and production process.

-

Implement a Robust Data Collection System: Use technology to automate data entry and minimize errors.

-

Regularly Analyze Your Cost Data: Identify areas for cost reduction and process improvement.

-

Utilize Cost Accounting for Pricing Decisions: Set prices that ensure profitability while remaining competitive.

Final Conclusion: Wrapping Up with Lasting Insights:

Cost accounting is an indispensable tool for businesses of all sizes. By understanding its principles, methods, and applications, organizations can unlock significant operational efficiencies, improve decision-making, and enhance their long-term profitability. The integration of technology further amplifies the power of cost accounting, transforming it into a dynamic engine for business growth and innovation. Investing in a robust cost accounting system is an investment in the future success of any business.

Latest Posts

Latest Posts

-

Information Circular Definition

Apr 24, 2025

-

What Is An Infomercial Definition How Theyre Made And Examples

Apr 24, 2025

-

Inflexible Expense Definition

Apr 24, 2025

-

Inflationary Risk Definition Ways To Counteract It

Apr 24, 2025

-

Inflation Protected Security Ips Definition

Apr 24, 2025

Related Post

Thank you for visiting our website which covers about Definition And Types Of Cost Accounting . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.